Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2016. The project is a required component of every master program.

Authors:

Ryan Jacildo and Ekaterina Rezepina

Master’s Program:

Macroeconomic Policy and Financial Markets

Paper Abstract:

Research concerning the linkage between global liquidity and domestic economic affairs is hardly new. Interestingly, however, it never gets old mainly because of its policy significance. The welfare impact of shocks to capital flows (may it be short or long-term) is by and large the bottom line of all the discussions. Inquiries about other pertinent issues such as global financial imbalance and asset price bubbles, international financial stability and global financial safety nets, and economic early warning systems are in one way or the other broadly tied with global liquidity. Indeed, the impact of shocks to global liquidity can be systemically disruptive. And because international financial landscape constantly changes (i.e. degree of linkages estimated in one period may not hold in the subsequent periods), regular spot checks are important. The aftershocks of the global financial crisis (GFC) in 2007/2008, for instance, re-emphasize the significance of understanding the consequences of fluxes in capital movement and the extent of these consequences in various settings and time periods.

Motivation:

The main motivation behind this study is to contribute to empirical literature on cross-border liquidity spillover effects on asset prices in light of broadening global economic integration. We decided to focus on the case of the Group of 7 (G7) economies (e.g. Canada, France, Germany, Italy, Japan, United Kingdom, and United States) and follow closely the earlier work of Darius and Radde (2010) – henceforth D&R. For the same set of economies, D&R looked at the relationship of global liquidity and asset prices before and after the “Great Moderation” period. In an attempt to provide an account of what happened after 2007, this study examines the behavior of the same variables until end of 2015 and checks whether there are significant changes to the magnitude of the pass though effects of global liquidity, particularly on the equity and property prices in recent years.

Conclusions:

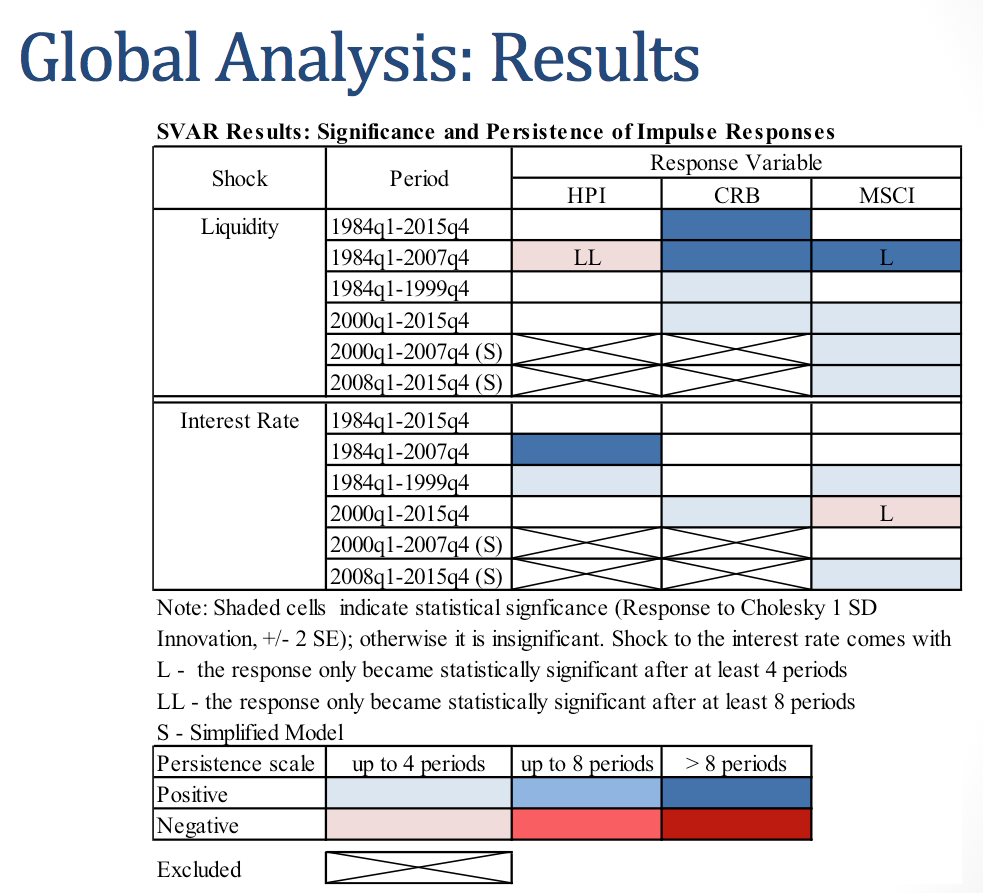

In light of the developments in the past decade that led central banks to flood the international financial system with liquidity, we deem it relevant to empirically re-examine the linkage between global liquidity and asset prices in large economies. To do the econometric analysis, we used available data from 1984q1 to 2015q4 and employed a VAR model following the specification suggested by D&R.

In the global analysis, we found that global liquidity has a positive significant impact on commodity prices using the sample from 1984q1 and 2015q4 but insignificant impact on equity prices. However, in our subsample analysis using the data from 1984q1 to 2007q4, our results showed that the impulse responses of both the CRB and the MSCI were positively significant and persistent while the impulse response function of house prices remained insignificant. Interestingly, D&R, which also used 1984q1 to 2007q4 as its Great Moderation subsample, found that the responses of commodity and equity prices to a liquidity shock were insignificant. In terms of the house prices, the results we obtained differed from those of D&R for periods from 1984q1 to 2007q4 in a sense that we found significantly negatively response to global liquidity albeit with a substantial lag of 16 quarters.

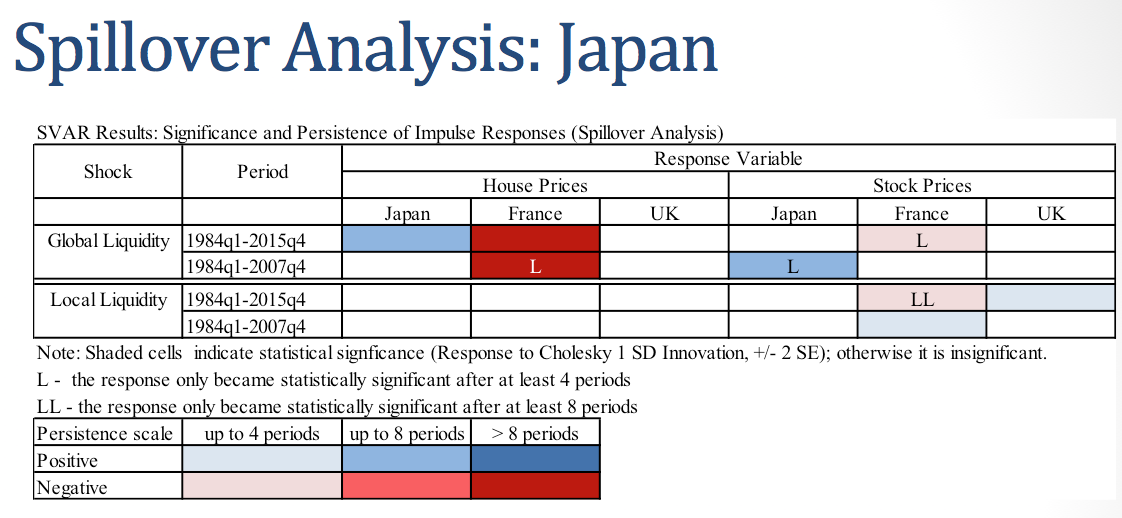

In our spillover analysis, we extended the model of D&R by adding the local stock prices to the model. For each economy, we ran the regression using data from 1984q1 to 2015q4 as well as from 1984q1 to 2007q4 (to serve as our pre-GFC subsample). The results of this exercise convey that the positive effect of a global liquidity shock on house prices in Japan obtained using data from 1984q1 to 2015q period disappears when only pre-GFC period is considered. In the full sample analysis both global and domestic liquidity did not affect stock prices in Japan, whereas the effect of global liquidity turned out to be positive for the pre-GFC period.

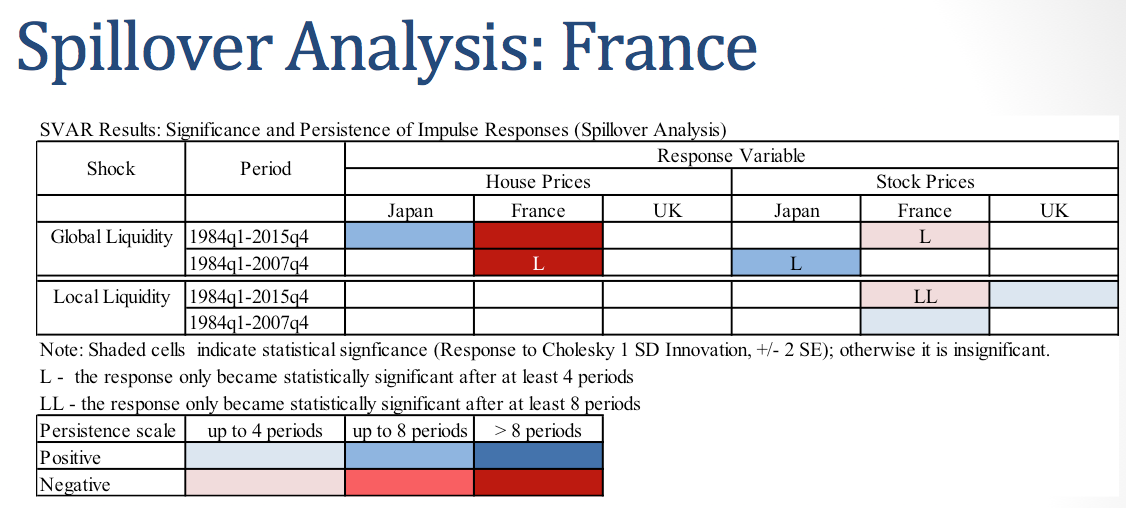

Notwithstanding the sample used (may it be full or pre-GFC), the effect of global liquidity on house prices in France stays significant and negative, while the negative impact of global liquidity on stock prices obtained using full sample disappears in pre-GFC subsample. In the case of the latter, the stock prices turned out to be significantly positively affected by local liquidity, while the inclusion of post crisis years made this response negatively significant with a substantial lag.

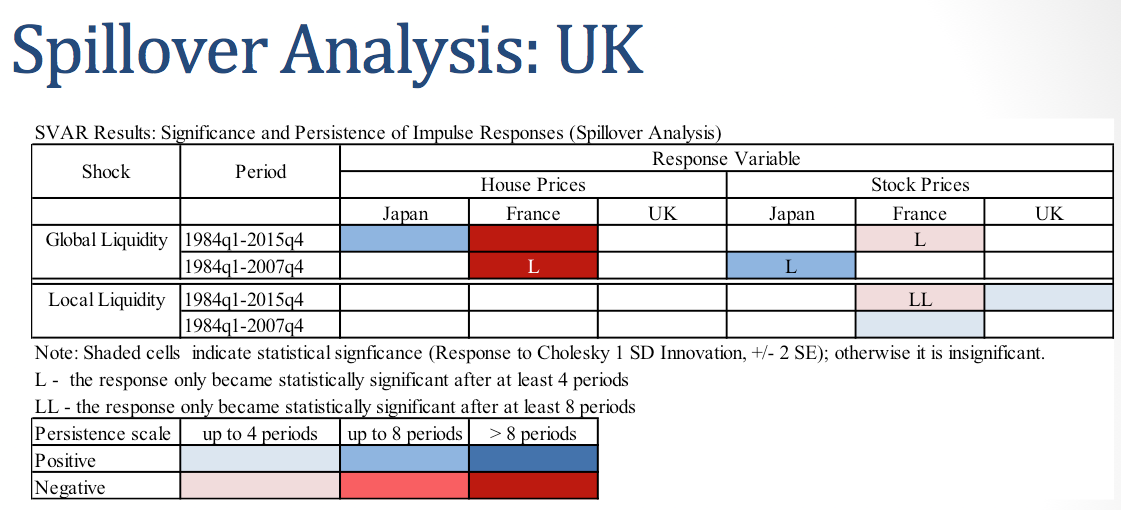

Lastly, the result of the pre-GFC subsample analysis involving the UK reveals that the effect of local liquidity shock on stock prices is not significant as opposed to full sample estimation when the effect was positive. Moreover, the variance decomposition dictates that global GDP growth rate explains the largest proportion of the volatility of stock prices in the UK.

Moving forward, one way to get a better understanding of the results would be to properly assess the country-level intertemporal idiosyncratic factors just like in the global analysis. Certainly, the nature and timing of these structural shifts can vary from one country to another. We likewise suggest trying different proxies for the global liquidity or run the model for the monthly data without house prices that are available only quarterly and the monthly proxy for GDP. Using monthly data would allow a closer analysis of dynamics in the post-GFC period. It would also be interesting to extend the scope of this exercise to emerging economies.