Tomas Williams (Economics ’12, GPEFM ’17) is Assistant Professor of International Finance at George Washington University in Washington, DC. His paper, “International Asset Allocations and Capital Flows: The Benchmark Effect” (with Claudio Raddatz, Central Bank of Chile and Sergio Schmukler, World Bank Research Group) is forthcoming at the Journal of International Economics.

International Asset Allocations and Capital Flows: The Benchmark Effect

As financial intermediaries such as open-end funds with benchmark tracking grow in importance around the world, the issue of which countries belong to relevant international benchmark indexes (such as the MSCI Emerging Markets) has generated significant attention in the financial world (Financial Times, 2015). The reason is that the inclusion/exclusion of countries from widely followed benchmarks has implications for the allocation of capital across countries. As institutional investors become more passive, they follow benchmark indexes more closely. These benchmark indexes change over time, as index providers reclassify countries, implying that investment funds have to re-allocate their portfolio among the countries they target. The capital flows generated by these portfolio re-allocations are important since worldwide open-end funds that follow a few well-known stock and bond market indexes manage around 37 trillion U.S. dollars in assets (ICI, 2016). These changes in benchmark indexes can produce unexpected effects in international capital flows, linked to how financial markets work, not necessarily to economic fundamentals.

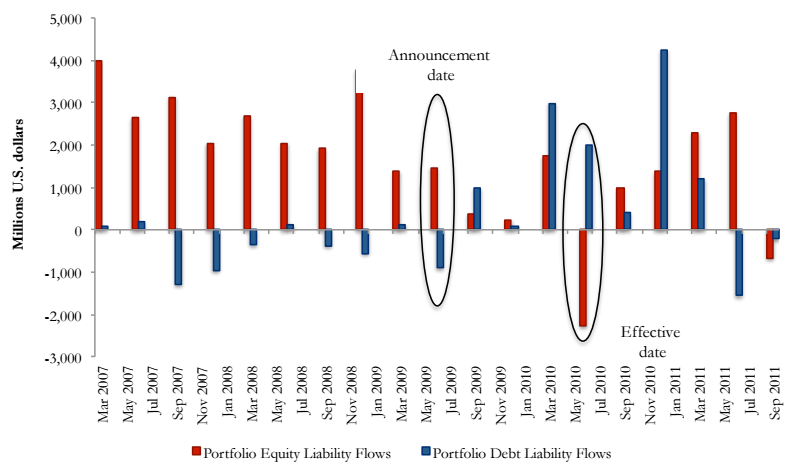

One clear example of these counterintuitive reallocations happened when MCSI announced in 2009 that it would upgrade Israel from emerging to developed market status, moving it from the MSCI Emerging Markets (EM) Index to the World Index. When the upgrade became effective in May 2010, Israel faced equity capital outflows of around 2 billion dollars despite its better status (Figure 1 below, click image to enlarge). The reason is that Israel became a smaller fish in a bigger pond. Israel’s weight in the MSCI EM Index decreased from 3.17 to 0, while it increased from 0 to 0.37 in the MSCI World Index. Israeli stocks in the MSCI index fell almost 4 percent in the week of the announcement and significantly underperformed the stocks not included in the index. The week prior to the effective date (when index funds rebalanced their portfolio) there was a 4.2 percent drop in the MSCI Israel Index, versus a 1.5 fall in the Israeli stocks outside the index.

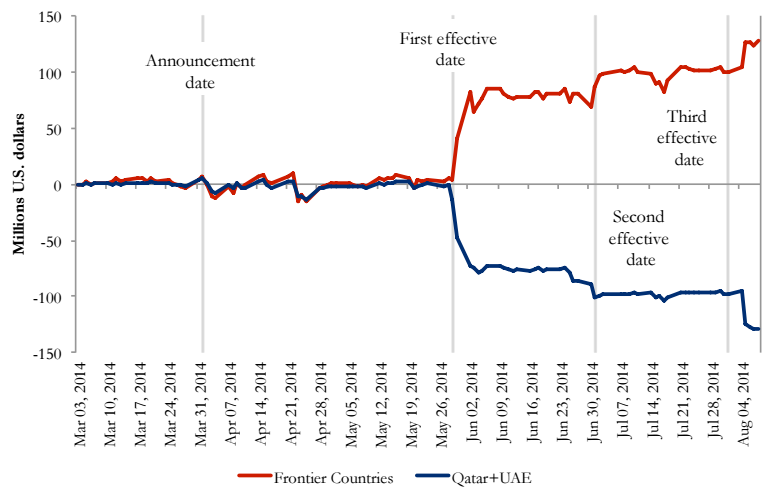

The effects of index reclassifications go beyond the countries and asset classes being specifically targeted. Spillovers could occur to other countries that share a certain benchmark with countries affected by reclassifications. A clear example of this is the upgrade in June 2013 of Qatar and United Arab Emirates (UAE) from the MSCI Frontier Markets (FM) Index to the MSCI EM Index. Together, these two countries were around 40 percent of the MSCI FM Index before the reclassification. When this reclassification took place, funds tracking closely the MSCI FM Index had to sell securities from these two countries and use the money to invest in the rest of the countries in the MSCI FM Index. This resulted in significant capital inflows and stock market price increases in countries such as Nigeria, Kuwait, and Pakistan (Figure 2, click image to enlarge).

These movements in financial markets have led to speculations and market movements related to potential new reclassifications. One recent and prominent example is that of China. For the past two years, MSCI delayed numerous times the introduction of China A-shares as a part of the MSCI Emerging Markets. Finally, in June 2017, they confirmed the inclusion of only a fraction of these stocks, creating capital inflows into the Chinese stock markets, and increases in stock prices (Financial Times, 2017). Chinese sovereign bonds may see similar capital inflows if J.P. Morgan, Citibank and Barclays decide to add China into their flagship bond indexes (CNBC, 2017).

In a recent study (Raddatz et al., 2017), we systematically document these benchmark effects, showing the various channels through which prominent international equity and bond market indexes affect asset allocations, capital flows, and asset prices across countries. Benchmarks have statistically and economically significant effects on the allocations and capital flows of mutual funds across countries. For example, a 1 percent increase in a country’s benchmark weight results on average in a 0.7 percent increase in the weight of that country for the typical mutual fund that follows that benchmark. These benchmark effects on the mutual fund portfolios are relevant even after controlling for time-varying industry allocations and country-specific or fundamental factors. Exogenous events that modify benchmark indexes affect benchmark weights. Furthermore, asset prices move both during the announcement and effective dates of the benchmark changes in response to the capital movements.

Academics, financial institutions, and policy makers have already started paying attention to the potential effects of benchmarks on capital flows and asset prices, as well as on herding, momentum, and risk taking (BIS, 2014; Arslanalp and Tsuda, 2015; IMF, 2015, Shek et al., 2015; Vayanos and Woolley, 2016). More work in this area would be welcomed as passive investing continues expanding.

References

Arslanalp, S., Tsuda, T., 2015. Emerging Market Portfolio Flows: The Role of Benchmark-Driven Investors. IMF Working Paper 15/263, December.

BIS, 2014. International Banking and Financial Market Developments. BIS Quarterly Review.

CNBC, 2017. Chinese Stocks got their Global Stamp of Approval, and now Bonds may be next.

Financial Times, 2015. Emerging Market Investors Dominated by Indices. August 4.

Financial Times, 2017. China Stocks Set for $500bn Inflows after MSCI Move. June 21.

ICI, 2016. Investment Company Institute: Annual Factbook.

IMF, 2015. Global Financial Stability Report.

MSCI, 2016. Potential Impact on the MSCI Indexes in the Event of the United Kingdom’s Exit from the European Union (“Brexit”). June.

Raddatz, C., Schmukler, S., Williams, T., 2017. International Asset Allocations and Capital Flows: The Benchmark Effect. Working Papers 2017-XX, The George Washington University, Institute for International Economic Policy.

Shek, J., Shim, I., Shin H.S., 2015. Investor Redemptions and Fund Manager Sales of Emerging Market Bonds: How Are They Related? BIS Working Paper 509.

Vayanos, D., Woolley, P., 2016. Curse of the Benchmarks. LSE Discussion Paper 747.

Wall Street Journal, 2014. Colombia Wins Investors’ Favor – And That’s the Problem. August 13.

About Tomas Williams

From his website:

I am an Assistant Professor of International Finance at George Washington University in Washington, D.C. My main fields of research are International Finance, Financial Economics and Empirical Banking. I have a special interest on financial intermediaries and how they affect international capital flows and economic activity. More specifically, I have been working on how the use of well-known benchmark indexes by financial intermediaries affects both financial markets and real economic activity.

More personally, I grew up in Buenos Aires, and studied economics at Universidad del CEMA. Afterwards, I moved to Barcelona and completed the Master’s Degree in Economics and Finance (Economics Program) at Barcelona GSE. Later on, I received my Ph.D. in Economics and Finance from Universitat Pompeu Fabra. I also spent one year as a visiting doctoral student in the Financial Markets Group (FMG) at the London School of Economics and Political Science.

Connect with Tomas on Twitter