We have a forthcoming article “Sectoral Risk Weights and Macroprudential Policy” in the Journal of Banking & Finance with our co-author Konstantin Vasilev (Essex).

Paper abstract

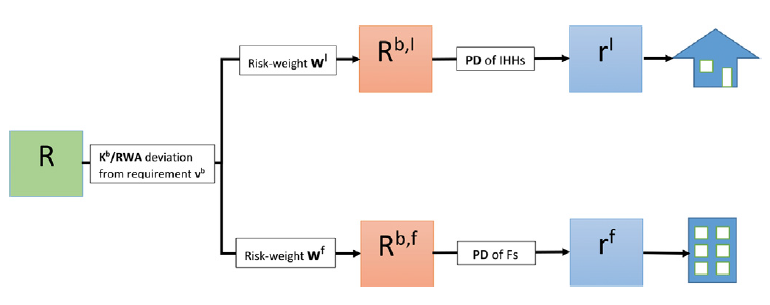

This paper analyses bank capital requirements in a general equilibrium model by evaluating the implications of different designs of such requirements regarding their impact on the tendency of banks to amplify the business cycle.

We compare the Basel-established Internal Ratings-Based (IRB) approach to risk-weighting assets with an alternative macroprudential approach which sets risk-weights in response to sectoral measures of leverage. The different methods are compared in a crisis scenario, where the crisis originates from the housing market that affects the banking sector and is then transmitted to the wider economy.

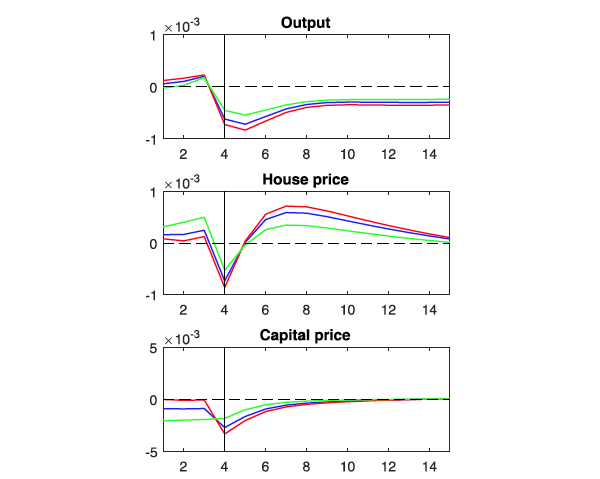

We investigate both boom and bust phases of the crisis by simulating an unrealized news shock that leads to a gradual build-up and rapid crash in the economy. Our results suggest that the IRB approach creates procyclicality in regulatory capital requirements and thereby works to amplify both boom and bust phases of the financial cycle. On the other hand, our proposed macroprudential approach to setting risk-weights leads to counter-cyclicality in regulatory capital requirements and thereby attenuates the financial cycle.

Conclusions in brief

- We show that IRB risk-weights can induce procyclicality of capital requirements and amplify both boom and bust phases of the business cycle. This is particularly concerning because procyclical risk weights could undermine other macroprudential tools, as these other tools are themselves based on risk-based measures of capital requirements e.g. Counter Cyclical Capital Buffers.

- Our alternative approach of macroprudential risk weights could induce countercyclicality of capital requirements, which may offer benefits in terms of smoothening financial cycles. Targeting macroprudential intervention on bank risk-weights is likely to be more effective when it is sector-specific. This will alter banks’ incentives in a sensitive way – thereby tending to attenuate sectoral asset booms.

- The results complement the ongoing debate about the potential merits of a Sectoral Counter Cyclical Capital Buffer, which is ongoing internationally.

About the authors

Alexander Hodbod ’12 is Adviser to representatives on the ECB Supervisory Board. He is an alum of the Barcelona GSE Master’s in International Trade, Finance and Development.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

If you are an alum and would like to share your work on the Barcelona GSE Voice, please reach out!