Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2015. The project is a required component of every master program.

Authors:

Mette Albèr, Ming Yu Wong, Urša Krenk & Stan deRuijter

Master’s Program:

Economics

Paper Abstract:

This paper examines the factors associated with gender disparities in attitudes towards intimate-partner violence against women (IPVAW) at the regional and household level using data from the 2010 Demo-graphic and Health Survey (DHS) in Rwanda. An OLS regression model was used at the regional level, while multivariate logistic regression models were fitted at the household level. The results show that women’s education level and women’s TV-viewing frequency are significant and consistent predictors of gender disparities at the household level, with sizeable marginal effects. More generally, many factors beyond national- and regional-level characteristics account for variation in IPVAW acceptance across genders, suggesting that more granular and sophisticated modes of analysis can help to determine the true nature of relationships between individual and household level factors and attitudes towards IPVAW.

Barcelona GSE alum Miguel Ángel Santos (ITFD ’11 and Economics ’12) is Senior Research Fellow at the Center for International Development at Harvard University. He recently won an award for a paper he has written with Harvard Professor Carmen Reinhart. In this post, he shares some background on the paper and some results.

I approached Carmen Reinhart last year, while I was a Mason Fellow at the Kennedy School. She said she would be very interested in writing something about Venezuela. It turns out that Venezuela is such an anachronic, chaotic economy, that it allows us to study some economic phenomena in a way no other place does.

My idea was writing about foreign debt sustainability and default probabilities, etc. Carmen suggested otherwise. After all, lots of people have been working on foreign debt sustainability, and it would not be interesting adding to that pile of work.

Instead, she suggested looking into domestic debt default via financial repression, and associating that to leakages in the capital account that in turn weakened the foreign asset position. It goes against some market analysts’ assessment that Venezuela can go wild internally, wild being able to serve its external debt without any trouble. So we used two modified formulas for estimating financial repression for the previous 30 years, differentiating free market years from years of exchange controls.

Our results

We proved that financial repression it is not only significantly higher in periods of exchange controls, but also that the sheer size in Venezuela was astounding, equivalent to more developed countries with much larger internal debt-to-GDP ratios. That is to say, with a smaller stock of domestic debt, the Venezuelan regime needs a lot more repression to collect that. So they actually engineer it, creating mechanisms to produce it: right now inflation is running at a rate five times higher than yields on domestic bonds or bank deposits.

We moved on to show that capital flight, conceived in broader sense, including the over-invoice of imports, was higher in periods of exchange controls. Since financial repression is rampant in periods of controls, people will run risks just to jump out of domestic currency and get into dollars (capital flight). They do that by two means: buying dollar-denominated bonds that the government has been selling in exchange for domestic currency, and over-invoicing imports. We measured the latter by a very innovative process, contrasting Central Bank reported imports with the sum of imports reported at Venezuelan customs. The difference is not only significantly higher across years of controls, but over those years it is 3-4 standard deviations away from the distribution of this error worldwide.

I presented the paper two weeks ago in San Juan, Puerto Rico, within the Business Association of Latin American Studies (BALAS), where it was granted the Sion Raveed Award, given to the best paper of the conference.

Comments welcome from the Barcelona GSE community

CID has published the paper on their working paper series. All comments from the BGSE Alumni and scholars community are welcome at this point. It is a modest paper, dealing with a small, crazy economy. And yet I think it makes a significant contribution.

Lecture summary by masters students Hugo Kaminski ’15 and Yi-Ting Kuo ’15.

During the 31st Barcelona GSE Lecture, Professor Jonathan Levin, Holbrook Working Professor of Price Theory at Stanford University, discussed the advantages and challenges of using Internet commerce data for empirical research in economics.

Seller Experience – Let real online sellers run experiments for us

Economic research has long relied on public governmental institutions and organisations to collect empirical data, which are reliable but expensive. Data on the Internet could potentially be an alternative source as it can reduce the cost of varying parameters. However, it is also challenging to isolate specific effects as customization of products and services raises concerns about selection and endogeneity.

Prof. Levin and his collaborators found that the millions of listings on eBay could potentially serve as millions of small experiments with different seller choices. In collaboration with eBay, US data allowed them to run fixed effect regressions exploiting within-experiment variation in prices, fees, displays, and other parameters.

Auction and Demand – Never start with an intermediate price

The buyers market is very competitive. If an auction starts at a low price, the item will be highly sellable and the market will drive it to around 80% of its value. Starting at a high price will make the item harder to sell, but increases the probability of ending with a higher price. The resulting estimated demand curve was convex, which implies that for a seller to start an auction with either a low or high price is more profitable than an intermediate price.

As second example, Prof . Levin argued that the Internet market could be used to test behavioural hypotheses about consumers. By looking at the multiple auction listings with different (flat rate) shipping fees, their analysis suggests that people prefer free shipping so much that they are willing to pay a higher price for the goods with free shipping even if there is an equal good with lower total price including shipping costs.

By analysing Internet commerce data from 2003 to 2012, they observed the sellers’ learning curve and concluded that the demand for online auction has declined. One interpretation of this development could be that consumers grew accustomed to increasingly instant purchase options and tend to spend more time on other online activities thus losing the attention for online auction.

Sales tax – a problem across US states

In the United States there exists a sales tax of 8.875% on average among states for within state sales. It does not come as a surprise that the payment of this tax is viewed as a negative additional charge which online often appears just towards the end of the purchasing process. To analyse the impact of the ‘tax surprise’ Prof. Levin estimates the tax sensitivity by comparing purchase rates.

Prof. Levin’s research finds that both consumers and sellers are aware of this perceived “extra charge” and the fact that the tax does not apply on out-of-state sales. Their analysis finds two consumer trends: first there exists a preference for goods bought in geographic proximity; second, the rising item-level substitution which means the consumer chooses to buy the item from an out-of-state seller to avoid the tax. These two trends seem to form a paradox.

Professor Nezih Guner (right) with our speaker

On the seller side, Prof. Levin illustrates the case of Amazon and the location of their distribution centres. Amazon takes advantage of California’s geographic shape by locating its distribution centres just outside state lines while keeping delivery times short. This results in being able to cater to consumers in California without paying the sales tax.

Since online shopping is a growing trend, taxation legislation changes have potentially great impact. Based on the data used, a 1% increase in current sales tax decreases online sales by 1.5-2.0% but increase online home-state sales by 3-4%; alternatively switching to national tax collection of internet purchases would decrease online sales by 12%.

Professor Levin’s presentation concluded that new large-scale data offers an opportunity to assess microeconomic theories of behaviour and market operation. The presentation was followed by a Questions & Answers session on data quality, auction information asymmetry and lessons learned from use of auctions. For Yi-Ting Kuo and Hugo Kaminski it has been an insightful experience to listen to Professor Levin’s talk presented with support from Banco Sabadell.

If you are interested to know more about the lecture, you may view it here:

The following job market paper summary was contributed by Keke Sun (IDEA). Keke is a job market candidate at UAB. Her research interests include Industrial Organization, Venture Capital Markets and Innovation.

Two-sided markets are economic platforms that connect two interdependent groups of users together and enable certain interactions between these two groups of users. The main characteristic of two-sided markets is the indirect network externalities, meaning that one group user’s benefits of joining one platform depends on the number of users of the other group on the same platform. My job market paper studies the impact of pure bundling and the level of consumer information on two-sided platform competition.

The Story

This paper is motivated by the casual observations from the smartphone operating system industry. The operating system (OS) platform connects consumer and application developers, the major competitors are Android by Google and iOS by Apple. Apple also has its amazing in-house handset, iPhone, it bundles the handset with the OS platform.

The Main Results

The leverage theory has established that, in standard one-sided market, if a firm can commit to pure bundling, when consumers have homogeneous valuation of the bundling product, pure bundling reduces equilibrium profits for all firms. Therefore, bundling is usually adopted to deter entry or lead to foreclosure (see Whinston (1990) and Carlton and Waldman (2002) ). However, in a two-sided market, if a platform could commit to aggressive pricing on one side and gain a larger market share. Hence, it becomes more valuable to the users on the other side. I show that, in the presence of asymmetric network externalities, when consumers have homogeneous valuation of the bundling handset, bundling may emerge as a profitable strategy when platforms engage in “divide-and-conquer” strategy: subsidizing the low externality side (consumers) for participation and making profits on the high-externality side (developers). That is, when the benefits of attracting one extra consumer are very strong, committing to aggressive pricing can be profitable without inducing the exit of the rival.

This paper also studies the impact of the level of consumer information on platform competition and the emergence of the bundling decision. Most literature on two-sided markets assumes that all agents have full information about prices and others’ preferences; therefore, can perfectly predict others’ participation decision (see Rochet and Tirole (2003), Caillaud and Jullien (2003), and Armstrong (2006) etc.). Following Hagiu and Halaburda (2014), I use the setting of a hybrid scenario in which some consumers are informed about developer subscription prices and hold responsive expectations about developer participation, while the remaining consumers are uninformed and hold passive expectations. This setting should be a good fit of a situation where information may be less than perfect for some users on different sides of the platform. For instance, some consumers don’t know how much Apple or Google charges the developers for listing applications. Information intensifies price competition with or without bundling. Bundling is more effective in stimulating consumer demand the larger proportion of informed consumers, but bundling is less likely to emerge as the fraction of informed consumers increases.

Strategy and Policy Implications

From a strategy perspective, this paper shows that both platforms have incentives to affect consumers’ knowledge regarding developer subscription prices. Without bundling, both platforms have incentives to withhold the information because consumer information intensifies price competition on both sides. However, when bundling does occur, the two platforms may have different attitudes towards consumer information. The bundling platform prefers a high level of consumer information because bundling is more effective to stimulate consumer demand. The competing platform wishes to withhold the information as it gets worse off as the level of consumer information increases. This paper also shows that when the network externalities are strong, it is more profitable for the platforms to be more aggressive.

From a public policy perspective, this paper provides recommendations concern bundling and information disclosure. Due to the existence of (positive) network externalities, consumer surplus increases with the number of developers on the same platform. Bundling does not only affect consumer subscription prices, but also affects the perceived quality of platforms as it affects developer participation. It has shown that pure bundling improves consumer welfare mainly because it offers a lower subscription price and more application variety to the majority of consumers. For the same reason, even when bundling implements second-degree price discrimination, bundling still improves consumer welfare. Also, information disclosure unambiguously improves consumer surplus by lowering subscription prices on both sides of the platform and improving developer participation. Thus, information disclosure should be encouraged or mandated for consumer’s sake.

“…One of my research projects is on the Panic of 1907. In many ways, it resembles our recent economic crisis. For me, the most startling resemblance is the absolute fear that the monetary authority had about any contraction in the credit market.”

Excerpt from the blog post Nothing New Under the Sun Brian C. Albrecht ’14 (Master in Economics)

PhD student at University of Minnesota

Barcelona GSE grad Alvaro Leandro looks at the EU’s Stability and Growth Pact through the lens of the draft budget plans of France and Italy.

The following post by Alvaro Leandro (ITFD’13 and Economics ’14) has been previously published by Bruegel.

Mr. Leandro is Research Assistant at Bruegel in Brussels, Belgium.

The EU’s fiscal framework, the Stability and Growth Pact (SGP), is a complicated system of fiscal rules. Rather than trying to assess the virtues and failures of the SGP, this blogpost aims at understanding its complex rules through the lens of the draft budget plans of France and Italy. France is in the corrective arm of the SGP, while Italy is now in the preventive arm, which allows the examination of various SGP requirements, such as the

structural balance pillar,

expenditure balance pillar,

and the debt criterion

which apply to countries in the preventive arm (like Italy), and the

headline budget deficit criterion,

the structural balance criterion,

and the cumulative structural balance criterion

which apply to countries in the corrective arm (like France). We also discuss the rules regarding financial sanctions.

On 28 November 2014, the European Commission released its opinions on the euro area Member States’ Draft Budgetary Plans for 2015. The purpose of these opinions is to assess each country’s compliance with the SGP, and to recommend appropriate action if there are risks of non-compliance.

Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”

One of the surprises was that, in the case of Italy and France (as well as Belgium), the Commission decided to postpone its recommendations until March 2015, “in the light of the finalisation of the budget laws and the expected specification of the structural reform programmes announced by the authorities“. Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”, according to the Commission.

The Framework

The Stability and Growth Pact is composed of a preventive and a corrective arm. The corrective arm is called the Excessive Deficit Procedure (EDP), which is triggered for countries with a general government deficit larger than 3 percent of GDP or with debt larger than 60 percent of GDP not being reduced at a satisfactory pace. France is currently under the corrective arm and Italy was as well until 2013. Italy is therefore now subject to the rules of the preventive arm.

Source: Country Stability and Convergence Programmes for MTOs, AMECO for forecast of 2014 and 2015 Structural Balances

Notes: Data labels are for the MTOs. According to the Treaty on Stability, Coordination and Governance (TSCG), signed by all euro area members in March 2012, all signatory Member States must have an MTO higher than -0.5% of GDP (or -1% for countries with a debt/GDP ratio lower than 60%). The “fiscal” part of the TSCG is often called the ‘Fiscal Compact’.

The fundamental variables used to assess compliance with the preventive arm of the SGP are the country-specific medium-term budgetary objectives (MTOs), which are defined as structural balances (a measure of the government budget balance adjusted for the economic cycle and one-off revenue and expenditure items; this blog post by Zsolt Darvas explains the estimation methodology and why it has some drawbacks). MTOs are chosen by each Member State following strict guidelines set out by the Commission, in order to ensure sustainability in its public finances (a higher MTO is required from countries with a high debt ratio or with a rapidly-ageing population faced with increasing age related expenditure for example, while the ‘Fiscal Compact’ limits the MTO for euro area member states, see the notes to Figure 1). A few examples of MTOs can be found in Figure 1: France, Italy and Spain have an MTO of 0 percent of GDP, while Germany’s MTO is -0.5 percent. This means that in the case of Germany, for example, a structural deficit of 0.5 percent of GDP is deemed enough to ensure the sustainability of its public finances.

The Fiscal Compact is not binding for non-euro area Member States, which therefore have more freedom in setting their MTOs. For example, Hungary has an MTO of -1.7 percent, the Polish and Swedish MTO is -1 percent, while it is zero for the United Kingdom.

To comply with the preventive arm of the SGP, all Member States must be at their MTOs or be on a path to reach them, with an annual improvement of their structural balance of 0.5 percent of GDP towards the MTO as a benchmark.

A higher effort might be required for countries with high debt/GDP ratios and pronounced risks to overall debt sustainability. A higher effort is also required in good economic times, and a lower effort in economic downturns. A Member State could also be allowed to deviate from the adjustments if it experiences “an unusual event outside its control with a major impact on the financial position of the general government”.

Therefore compliance with the preventive arm is not defined by the Member State’s structural balance, but by its path towards the MTO.

Italy

Structural balance pillar: Table 1 shows the recommended path for Italy. On the 28th of November 2014 the Commission decided that “severe economic conditions” (namely a real GDP contraction and a large negative output gap: see Table 3) justified that Italy is not required to adjust its structural balance towards the MTO by the 0.5 percent of GDP benchmark in 2014. This is why the required change in the structural balance for 2014 is 0. Italy had originally planned a large correction of its structural budget for 2014 in its 2013 Stability Program, of 0.7 percentage points. In its Draft Budget Plan for 2014 Italy revised this adjustment to 0.3. Finally it invoked Article 5 of Regulation 1175/2011 in its 2014 Stability Program which allows a deviation from the required adjustment “in the case of an unusual event outside the control of the Member State concerned which has a major impact on the financial position of the general government”. The required adjustment is also 0 in 2013 for the same reason: negative real output growth makes Italy eligible to the escape clause. In 2015 real GDP is forecast by the Commission to increase by 0.6 (see Table 3), which means that Italy can no longer apply for the escape clause regarding economic downturns.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of Italy (28 November 2014), European Commission Autumn Forecast (November 2014), Italy’s Stability Programme April 2014, Italy’s Stability Programme April 2013, Vade Mecum on the Stability and Growth Pact (May 2013)

Note: ΔSB denotes the percentage point change in the structural balance. MLSA: minimum linear structural adjustment. DBP: draft budget plan

(1): Deviation of the growth rate of public expenditure net of discretionary revenue measures and revenue increases mandated by law from the applicable reference rate in terms of the effect on the structural balance. A negative sign implies that expenditure growth exceeds the applicable reference rate.

Expenditure balance pillar: Member States in the preventive arm of the SGP also have to comply with the expenditure benchmark pillar, which complements the structural balance pillar. It requires countries that are not at their MTO to contain the growth rate of expenditure net of discretionary revenue measures to a country-specific rate below that of its medium-term potential GDP growth. This medium-term potential GDP growth is calculated as a 10-year average (of the 5 preceding years, the current year and forecasts for the next 4 years), and in the case of Italy it is 0 percent in 2014 and 2015. Had Italy been at its MTO it would have had to contain net expenditure growth to 0 percent. However, not being at its MTO, it is required to contain net expenditure growth to a reference rate below medium-term potential GDP growth: -1.1 percent in 2015 (which is calculated so that it is consistent with a tightening of the budget balance of 0.5 percent of GDP when GDP grows at its potential rate). The applicable reference rate in 2014 is 0 because of the “severe economic conditions”. In 2013 the applicable reference rate was 0.3, which is different to that in 2014 and 2015 because it is revised every three years. The commission allows one-year and two-year average deviations of a maximum of 0.5 pp of GDP in terms of their impact on the structural balance. In 2015 the deviation in terms of its effect on the structural balance is forecast to be of 0.7 pp. of GDP, which is a deviation larger than the allowed 0.5 pp.

Debt Criterion: Countries which have recently left the EDP are subject to a 3-year transition period aimed at ensuring that the debt level is being reduced at an acceptable pace. Italy is in such a transition period, since it left the EDP in 2013. It is thus subject to required medium-term linear structural adjustments (MLSAs) aimed at ensuring that it will comply with the debt criterion. These MLSAs are formulated in terms of adjustments to the structural balance. Since Italy is in the preventive arm and therefore also subject to required adjustments towards the MTO, the largest one is applicable. The 2.5 pp. MLSA in 2015 (larger than the 0.5 pp. required change under the preventive arm) is at serious risk of not being met according to Commission forecasts. This violation of the debt criterion could lead to a reopening of the Excessive Deficit Procedure.

Commission’s view: In its opinion on Italy’s Draft Budget Plan released at the end of November 2014, the Commission points to risks of non-compliance with the requirements of the SGP, and “invites the authorities to take the necessary measures […] to ensure that the 2015 budget will be compliant with the Stability and Growth Pact”. It then says that “The Commission is also of the opinion that Italy has made some progress with regard to the structural part of the fiscal recommendations issued by the Council in the context of the 2014 European Semester and invites the authorities to make further progress. In this context, policies fostering growth prospects, keeping current primary expenditure under strict control while increasing the overall efficiency of public spending, as well as the planned privatisations, would contribute to bring the debt-to-GDP ratio on a declining path consistent with the debt rule over the coming years.”

France

Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit.

Headline budget deficit criterion: Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit. France has now been under the EDP for 5 consecutive years, and is subject to requirements set out in the latest Council recommendation to end the excessive deficit situation (June 2013). The recommendation released in 2009 originally planned a correction of the deficit (below 3 percent) by 2012, which was then postponed to 2013 in view of the actions taken and the “unexpected adverse economic events with major unfavourable consequences for government finances”. In June 2013, the Council again postponed the correction of the deficit to 2015 for the same reasons: France fell slightly short of the required 1 percent average annual fiscal effort for the period 2010-2013 (the actual average annual fiscal effort was 0.9 percent), but this was again against a backdrop of “unexpected adverse economic events”.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of France (November 28, 2014), Council recommendation to end the excessive deficit situation (June 2013), European Commission Autumn Forecast (November 2014)

Note: ΔSB denotes the percentage point change in the structural balance

The latest Council recommendation (June 2013) sets out a path for France’s headline government balance, which you can see in Table 2. By 2015, the headline balance should be reduced to -2.8 percent of GDP. The forecast headline balance of -4.5 percent falls significantly short of this requirement.

Structural balance criteria: Additionally the adjusted change in the structural balance from 2014 to 2015 is forecast to be of 0.0 pp., and its cumulative change from 2012 to 2015 is forecast to be 1.6 pp., falling short of the requirements of 0.8 pp. and 2.9 pp. respectively (1). The structural budget also deviates from the requirements for 2014.

Commission’s view: Thus France is “at a risk of non-compliance” with the SGP, and, contrary to Italy, the Commission “is also of the opinion that France has made limited progress with regard to the structural part of the fiscal recommendations issued by the Council […] and thus invites the authorities to accelerate implementation”. In his letter to the President of the European Commission, France reiterated its determination to go ahead with reforms, most notably in the labour market. It remains to be seen whether progress by March 2015 will be assessed to be sufficient by the Commission.

Table 3: France and Italy: main macroeconomic indicators in 2014 and 2015

Sanctions

Non-compliance with the SGP can lead to sanctions. In the preventive arm, a Council recommendation which is not respected can lead to an interest-bearing deposit of 0.2 percent of GDP. A euro-area country in the corrective arm of the SGP may be required to make a non-interest bearing deposit until the deficit has been corrected, after which it can also be sanctioned with a fine worth up to 0.5 percent of GDP (with a fixed component of 0.2 percent of GDP and a variable component (2)). France and Italy are both at a risk of non-compliance with the requirements of the SGP. Failure to meet the required efforts in terms of fiscal consolidation and structural reforms by March 2015 could bring them closer to possible sanctions, unless the flexibility of the SGP is stretched further. Recent growth and inflationary figures suggest continued weak economic activity, and if economic data of 2014 qualified for “severe economic conditions”, 2015 may qualify too, especially if growth and inflation will disappoint relative to the November 2014 ECFIN forecasts. And in the preventive arm, structural reforms which have a verifiable positive impact on the long-term sustainability of public finances (such as by raising potential growth) could be considered when assessing the adjustment path to the medium-term objective.

Notes:

(1) The adjusted changes in the structural balance correct for the negative impact of the changeover to ESA 2010 as well as for changes in potential growth and revenue windfalls/shortfalls.

(2) This variable component is equal to “a tenth of the absolute value of the difference between the balance as a percentage of GDP in the preceding year and either the reference value for government balance, or, if non-compliance with budgetary discipline includes the debt criterion, the government balance as a percentage of GDP that should have been achieved in the same year according to the notice issued”

Post by Nadim Elayan, current student in the Barcelona GSE’s Master Program in International Trade, Finance and Development. Follow him on Twitter @Nadim1306.

It is unethical that 20-year-old guys with no studies whatsoever earn 20 million euros a year by just kicking a ball during one hour and a half once a week whereas doctors who have studied almost an entire decade and save human lives every day earn 500 times less.

A fair society should compensate with higher wages people who save human lives than people that entertain us during the weekends.

How can we stand by watching soccer players earning millions a year while there are people starving in the same country?

Most of us will have probably heard these sentences or similar ones regarding the large wages that soccer players earn and even that this situation is immoral or a bad incentive for kids to have a good education. But is this true? Do soccer players actually earn more than doctors?

Before analyzing the Spanish soccer labor market or discussing the ethical implications of this situation we need first to say that this is not true. The fact that we can name some players with shockingly salaries it does not mean that on average soccer players earn more than doctors, or even more than the average salary of a specific country. In order to compare professions we need a non-biased sample. We cannot look at the best soccer player in the whole history, Lionel Messi, and compare his salary with a regular doctor in Barcelona and then conclude that soccer players earn 500 times more than doctors. This situation would be the same as looking at Yao Ming, a Chinese basketball player with a height of 7.6 feet (2.29 meters) and a weight of 310 pounds (141 kg) and wrongly concluding that Chinese people are 2 feet taller (0.6 meters) and they weigh 130 pounds (59 kg) more than the average European citizen. Thus Lionel Messi is not the best representative of soccer players’ earnings terms as Yao Ming is not the best representative of the Chinese citizen in physical terms.

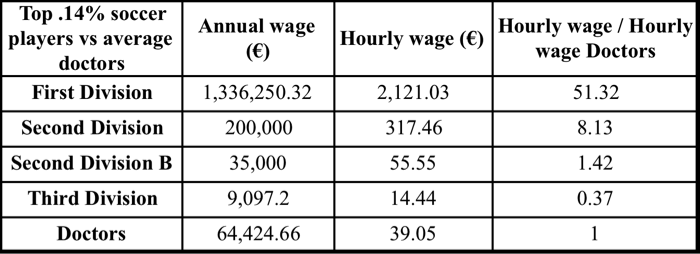

In Spain there are more than 700,000 professional and amateur soccer players according to the Real Federación Española de Fútbol and most of them work without a salary or earning below the minimum wage and that is why most of them need another job. There are about 500 players earning on average a wage of 1,336,250.32€ a year, the ones playing in the First Division and also about 500 players earning a wage below 200,000€ on average, the ones playing in the Second Division[1]. So in total we can count that within Spain there are only around 1000 players earning a salary way above the salary an average doctor earns, which in Spain is 64,424.66€[2] on average.

We would have also to take into account that the soccer professional life is barely higher than 10 years while the doctor’s one would be around 35 to 40 years. All this without considering the high risk of injury a soccer player faces every day that would leave him without any salary at all the rest of his life. But of course on the other hand soccer players work no more than 15 hours a week on average and therefore the wage for this .14% gets even larger if calculated per hour. So in order to compensate for the differences in professional lives we should observe that soccer players would earn at least 3.5 to 4 times more than doctors.

Table 1. Source: OCDE and El Pais.

We can see that these 1,000 players, .14% out of the total, earn way more than doctors on average but the next group of professional players who earn the most are the ones playing in 2nd B Division. There are 2,000 players in this Division earning on average 35,000€, what is actually less than doctors, but the hourly wage would still be above, 55.55€ per hour. If we go further away focusing in the ones playing in 3rd Division their hourly wage is 14.44€ already below the doctors one.

Summing up .14% out of total soccer players earn a salary way above the doctors’ average that more than compensates their shorter professional life. The next .28% still earns a higher hourly wage than doctors’ average but not enough to compensate their shorter professional life. So the rest 99.58% of the soccer players do not earn more than the average salary of a doctor. Actually most of them do not earn anything and some of them earn a little bit if they are in the starting line-up or for each victory.

Once showed that the average soccer player does not earn more than the average doctor, not even more than the minimum wage, we will analyze the soccer labor market and try to explain why this 0.14% earn so much money.

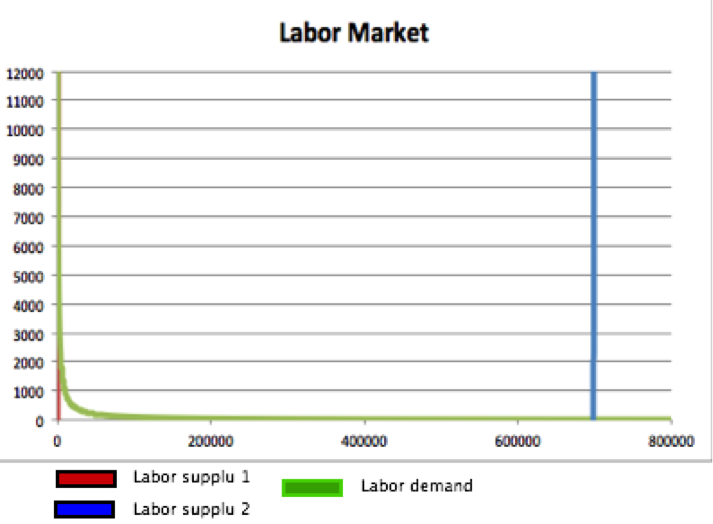

Analyzing the soccer labor market

First we will focus on the soccer labor demand. It is extremely high for very low values of labor hired, so for the first soccer players in the First Division and even for the Second Division. It is easy to show this by noticing that European societies are willing to fill 50 to 90 thousand people stadiums more than 30 times a year at prices between 20€ and 200€ per person each game. Therefore demand is huge. But for higher levels of labor hired, so 2nd Division B, 3rd Division and following Divisions the labor demand is very low and close to 0. Usually these games are free attendance or paying a type of mandatory lottery participation.

Now we can talk about the labor supply. In this case we can separate it into 2 subgroups. For simplicity we just divide the market in 2 subgroups, the first is composed by the 1000 soccer players playing in First or Second Division and the rest of the players. Even when considering perfect inelastic labor supplies we see very high wages for the first subgroup due to the high labor demand and also due to the very scarce labor supply of this type. Whereas for the second subgroup the wages are extremely low, almost 0, because of the low labor demand and the extremely high labor supply.

Ethical implications

People think constantly about soccer, they fill large stadiums paying really high prices and spend almost 100€ a year to buy the newest shirt of their team. Furthermore between 20 and 60 percent of total TV spectators watch Champions League games in prime time and even watch TV programs and listen radio programs that only talk about soccer… In conclusion people spend a large fraction of their income and time on soccer. Is it unethical that a large fraction of this cake is sent to workers via wages?

If we think that this 0.14% of total soccer players earn too much we should then say where we send this money generated by them. Would it be more ethical to let billionaire soccer teams owners to keep a larger fraction instead? In a non-profit Solow Economy, total output goes to capital and labor, therefore , high output will translate into high wages (for one club L=25, so very low). For example in F.C. Barcelona the season 2014-2015 has spent 509 million € in total and 288.9 million € of them only in players’ wages. So 56.76% of total expenditure goes to their soccer players[3].

Secondly if we speak about fairness we should want a society that creates only inequality from people who had the same life opportunities but they succeeded and managed to highlight in their respective fields and dislike inequalities coming from differences in opportunities. Since playing soccer is not expensive, all kids can play it everywhere and the best clubs, knowing this, have scouters all over the world. This makes this labor market pretty competitive, almost every kid at age 12 has at least tried once to get in F.C. Barcelona or Real Madrid through many tests these clubs organize everywhere. Thus, the kids who finally succeed must have been better than almost every kid of their age in the planet. All this combined make the differences in wages created be explained by differences in talent and effort no matter the race, family’s economic status or better education opportunities. In fact, most of the best soccer players like Pelé, Maradona, Ronaldinho, Cristiano Ronaldo, Samuel Eto’o, so also the ones earning high wages, come from very poor families.

Lastly the fact that there are people starving in a country has nothing to do with the fact that there are soccer players earning large wages because this is determined by a very large labor demand and a very scarce labor supply for this very specific First and Second Division players. The labor demand is determined by the society’s taste so we should blame this taste if we think that the amount of money generated by soccer is disproportionately huge and instead we should allocate this exact amount of time and income to fight hunger and other problems we find more relevant.

[1] Every team posts their wage budget annually. These values are obtained by dividing the total wage budget over the total players in that division.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.

{kind=link}