Publication in Journal of Banking and Finance by Alex Hodbod (ITFD ’12) and Steffi Huber (Economics ’10, GPEFM ’17)

We have a forthcoming article “Sectoral Risk Weights and Macroprudential Policy” in the Journal of Banking & Finance with our co-author Konstantin Vasilev (Essex).

The authors!

Paper abstract

This paper analyses bank capital requirements in a general equilibrium model by evaluating the implications of different designs of such requirements regarding their impact on the tendency of banks to amplify the business cycle.

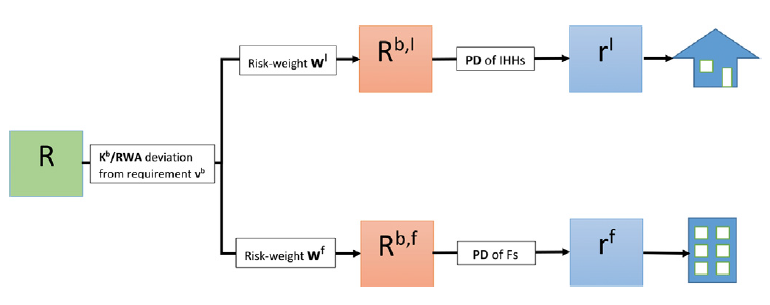

Interest rate spreads structure. This figure gives an overview of the different interest rate spreads within the model and the factors that affect them. The asset-specific interest rate spreads determine the borrowing costs of households and firms and hence the quantities of specific loan types in the economy.

We compare the Basel-established Internal Ratings-Based (IRB) approach to risk-weighting assets with an alternative macroprudential approach which sets risk-weights in response to sectoral measures of leverage. The different methods are compared in a crisis scenario, where the crisis originates from the housing market that affects the banking sector and is then transmitted to the wider economy.

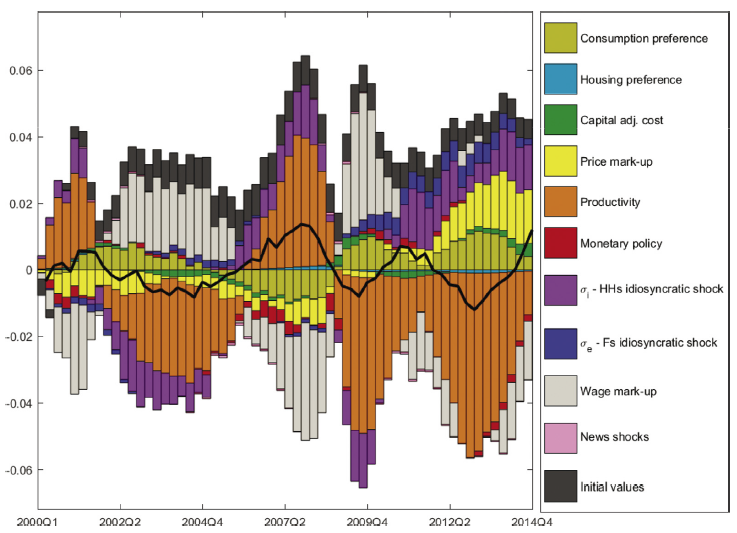

Variance decomposition – real consumption during the Great Recession. This variance decomposition shows that the model identifies the productivity shock and the shock to mortgage lending risk to be the main drivers of the crash in real consumption during the Great Recession. In our model, the main channel through which the shock to mortgage risk has a procyclical effect on consumption is through lending and house prices.

We investigate both boom and bust phases of the crisis by simulating an unrealized news shock that leads to a gradual build-up and rapid crash in the economy. Our results suggest that the IRB approach creates procyclicality in regulatory capital requirements and thereby works to amplify both boom and bust phases of the financial cycle. On the other hand, our proposed macroprudential approach to setting risk-weights leads to counter-cyclicality in regulatory capital requirements and thereby attenuates the financial cycle.

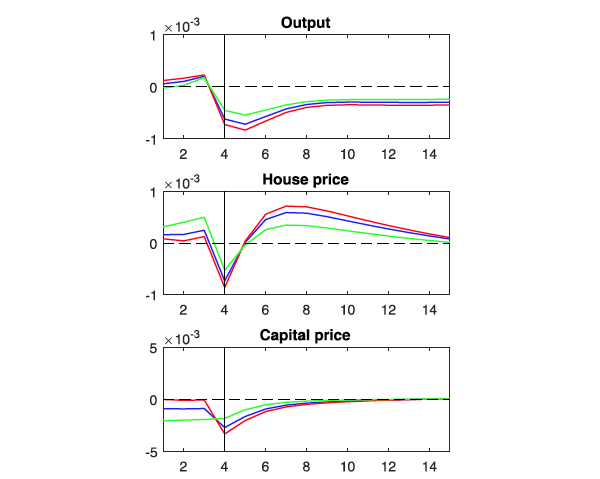

Impulse Response Function – Unrealised news shock. Here, we model both the build-up and crash phases of the crisis and use this to examine how different policy approaches perform in handling the boom phase of the cycle. In periods 1-4 agents start with expectations that a housing boom will occur, but at period 4 a shock arrives as this boom does not materialise. At the top of the chart one sees that the policy setup based on the IRB approach (red) generates the biggest macroeconomic consequences from this shock; it is the most procyclical. The macroprudential approach to risk-weighting (in green) is the least procyclical. An unweighted “leverage ratio” approach (blue) is less procyclical than the IRB approach, but more so than our macroprudential approach.

Conclusions in brief

We show that IRB risk-weights can induce procyclicality of capital requirements and amplify both boom and bust phases of the business cycle. This is particularly concerning because procyclical risk weights could undermine other macroprudential tools, as these other tools are themselves based on risk-based measures of capital requirements e.g. Counter Cyclical Capital Buffers.

Our alternative approach of macroprudential

risk weights could induce countercyclicality of capital requirements, which may

offer benefits in terms of smoothening financial cycles. Targeting

macroprudential intervention on bank risk-weights is likely to be more

effective when it is sector-specific. This will alter banks’ incentives in a

sensitive way – thereby tending to attenuate sectoral asset booms.

The results complement the ongoing debate about the potential merits of a Sectoral Counter Cyclical Capital Buffer, which is ongoing internationally.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

International Trade, Finance, and Development master project by Zhuldyz Ashikbayeva, Marei Fürstenberg, Timo Kapelari, Albert Pierres, Stephan Thies ’19

Source: NY Times

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

This thesis studies the impacts of flooding on income and expenditures of rural households in northeast Thailand. It explores and compares shock coping strategies and identifies household level differences in flood resilience. Drawing on unique household panel data collected between 2007 and 2016, we exploit random spatio-temporal variation in flood intensities on the village level to identify the causal impacts of flooding on households. Two objective measures for flood intensities are derived from satellite data and employed in the analysis. Both proposed measures rely on the percentage area inundated in the surrounding of a village, but the second measure is standardized and expressed in comparison to the median village level flood exposure. We find that household incomes are negatively affected by floods. However, our results suggest that rather than absolute levels of flooding, deviations from median flood exposure are driving negative effects on households. This indicates a certain degree of adaptation to floods. Household expenditures for health and especially food rise in the aftermath of flooding. Lastly, we find that above primary school education helps to completely offset potential negative effects of flooding.

Conclusion

This paper adds to the existing body of literature by employing a satellite based measure to investigate the long-run effects of recurrent floods on household level outcomes. We first set out to identify the causal impacts of flooding on income and expenditures of rural households in Thailand. Next, we explored and compared shock coping strategies and identified potential differences in flood resilience based on household characteristics. For this purpose, we leveraged a detailed household panel data set provided by the Thailand Vietnam Socio Economic Panel. To quantify the severity of flood events, we calculated flood indices based on flood maps collected by the Geo-Informatics and Space Technology Development Agency (GISTDA) measuring the deviation from median levels of flooding in a 5km radius around a respective village. The figure below illustrates the construction of the index for a set of exemplary villages that lie in the Nang Rong district of Buri Ram in northeast Thailand.

(a) 2010 flooding in Buri Ram and surrounding provinces. Red lines mark the location of the Nong Rong district.

(b) Detailed overview of flood index construction. Red dot shows the exact location of each village with the 5 km area around each village marked by the red circle.

Our results suggest a negative relationship between floods and per household member income, for both total income and income from farming. Per household member expenditure, however, does not seem to be affected by flood events at all. The only exemptions are food and health expenditures, which increase after flood events that are among the top 10 percent of the most severe floods. The former is likely to be driven by the fact that many households in northeastern Thailand live at subsistence level, and therefore consume their farming produce. A lack of production in a given year may lead these households to substitute this loss by buying produce from markets. Rising health expenditures may be explained by injuries caused or diseases obtained during a heavy flood.

Investigating potential risk mitigation strategies revealed that households with better educated household heads suffer less during flood events. However, this result does not necessarily point to a causal relationship, as better educated households might settle in locations of the village which are less likely to be flooded. While our data does not allow to control for such settlement choices on the micro-spatial level, our findings still provide valuable insights for future policy-relevant research on the effects of education on disaster resilience in rural Thailand. Moreover, our data suggests that only very few households are insured against potential disasters. Future research will help to investigate flood impacts and risk mitigation channels in more detail.

Fall 2019 roundup of CaixaBank Research by Barcelona GSE alumni

It’s time once again to check in with Barcelona GSE Alumni who are now Economists and Senior Economists at CaixaBank Research in Barcelona. As part of their duties, they regularly publish working papers and reports on a range of topics. Below are some of their latest contributions.

(If you’re a Barcelona GSE alum and you’re also writing about Economics, Finance, or Data Science, let us know where we can find your stuff!)

Communication is one of the most powerful monetary policy tools. For this reason, CaixaBank Research has developed an index to measure the sentiment of the ECB’s statements.Our ECB sentiment index shows a strong correlation with euro area economic activity indicators and foresees changes in the reference interest rate. The index notes a significant deterioration in ECB sentiment between late 2017 and Q3 2019 and shows how geopolitical uncertainty has affected the ECB’s view of the economic outlook.

In this article, we analyse the extent to which it will be more difficult for Spanish companies to establish relations for international expansion with the United Kingdom following Brexit. We use the CaixaBank Index for Business Internationalisation (CIBI), which classifies foreign countries according to the potential for internationalisation they offer for Spanish companies, and we analyse the impact of the four Brexit scenarios put forward by the Bank of England.

Digital technologies permeate the debate on the future of the economy. Monetary policy and its main vehicle, money, are no exception. More and more products are sold over the internet and cash is used less and less. This new digital economy creates new demands on the financial sector and digital money emerges as a new means of payment that appeals to consumers. How does all this affect monetary policy? What can central banks do (and what are they doing) about it?

Mario Draghi ends his eight-year mandate at the ECB on October 31, leaving the central bank at the cutting edge of monetary policy. Under Draghi’s leadership, the ECB has offered significant support to the recovery of the euro area. However, the latest measures have raised doubts over the margin for action and effectiveness of monetary policy. Christine Lagarde, with a less technical profile but a vision of continuity in monetary policy, will take over in a sombre economic environment in which signs of fragmentation between ECB members have appeared.

ITFD master project by Sofia Alvarez, Michael Barczay, Guadalupe Galambos, Ina Sandler, and Rasmus Herløw Schmidt ’19

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Whereas monetary policy in the euro area is conducted by one single authority, the European Central Bank (ECB), the real effects of these decisions provoke different reactions among the set of targeted countries. One common explanation for this finding is structural heterogeneity across the members of the eurozone. The paper assesses how commercial bank interconnectedness – as a specific source of structural heterogeneity – affects the propagation of common monetary policy shocks across the euro countries between 2003 and 2018. While recent research has found that bank interconnectedness can counteract the contraction in loans resulting from a monetary policy tightening in the US, evidence on the effects in the euro area is scarce. The paper tests this hypothesis empirically by constructing a panel data set for the original euro area countries, creating a measure for country-specific bank interconnectedness, and by identifying an exogenous monetary policy shocks based on high-frequency data. Employing local projections we find evidence that – in accordance with the theoretical model we discuss – a contractionary monetary policy surprise leads to a reduction in the supply of corporate and household loans in countries with a low degree of interconnectedness. Conversely, when the banking sector is highly interconnected, the impact of monetary policy is reduced or even counteracted. This implies that a common monetary policy shock can have heterogeneous effects among countries of the euro area, depending on the degree of interconnectedness of their banking industries. These results are robust to the inclusion of a wide set of controls and alternative shock specifications.

Conclusions and Key Results

Standard theory, assuming that the balance sheet transmission channel is at play, suggests that an increase in the interest rate reduces the value of pledgeable assets held by firms and households. This reduction in the borrowers’ creditworthiness consequently induces banks to constrain their amount of lending. A higher degree of interconnectedness of the banking sector, however, makes banks less sensitive to changes in the value of the collateral posted by borrowers since loan portfolios can be traded among banks with different risk exposures. Thus, when banks are highly interconnected, the reduction of the loans supply after contractionary monetary policy is expected to be smaller and the effects of monetary policy are likely to be less pronounced.

The paper tests this hypothesis for the eurozone using local projections and a panel dataset of 12 euro-area countries in the period between 2003 and 2018. The eurozone constitutes an excellent subject to study: It exhibits significant variation of bank interconnectedness – both across time and countries – which makes the hypothesis of bank interconnectedness as a determinant of heterogeneous reactions to monetary policy particularly relevant.

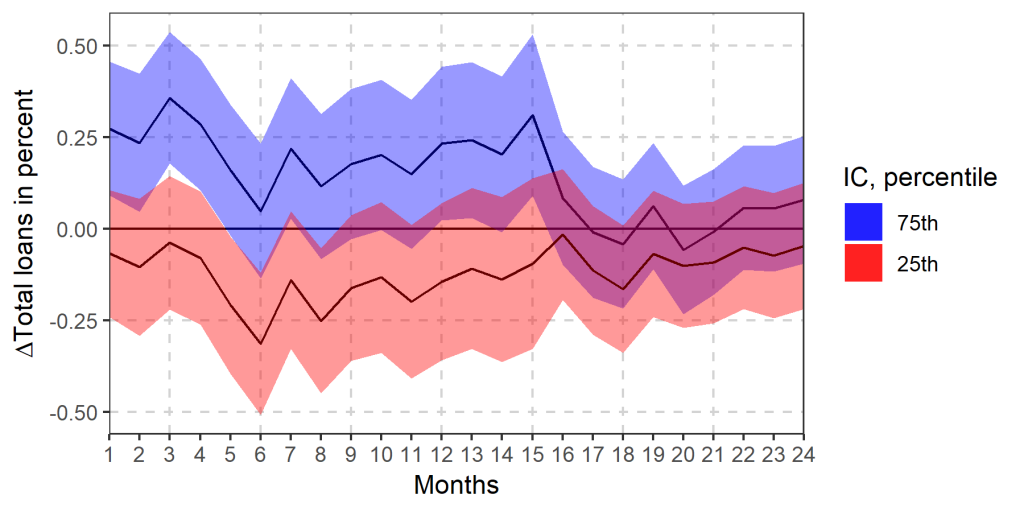

The key findings of the paper are that interconnectedness is in fact an important driver of heterogeneity in the transmission of monetary policy in the eurozone. More precisely, the analysis shows that when bank interconnectedness is low, contractionary monetary policy leads to a reduction in lending. In countries with highly interconnected banking sectors, however, the paper documents that the impact of monetary policy on loans may be offset. Even more so, our findings suggest that the effect of monetary policy may even be reversed at certain points in time after a monetary policy shock (see Figure 1). More generally, these effects seem to persist for approximately 15 months and hold for both household and corporate loans. A potential conjecture for the observed increase in loans, when bank interconnectedness is high, could be that contractionary shocks induce lending from highly interconnected core countries to countries with low bank interconnectedness in the European periphery.

Additionally, higher interest rates may induce banks to increase the loan supply due to higher potential returns in a context of efficient risk-sharing. The analysis also suggests that cross-country variation of bank interconnectedness, in particular, plays an important role in explaining heterogeneous responses to monetary policy. Muting the cross-country variation, by contrast, delivers effects that are still in line with the theory but which turn out to be statistically insignificant. In other words, accounting for cross-country heterogeneity is essential. Moreover, employing alternative specifications, the results are found to be robust to using alternative shock measures, including additional controls, and excluding outliers.

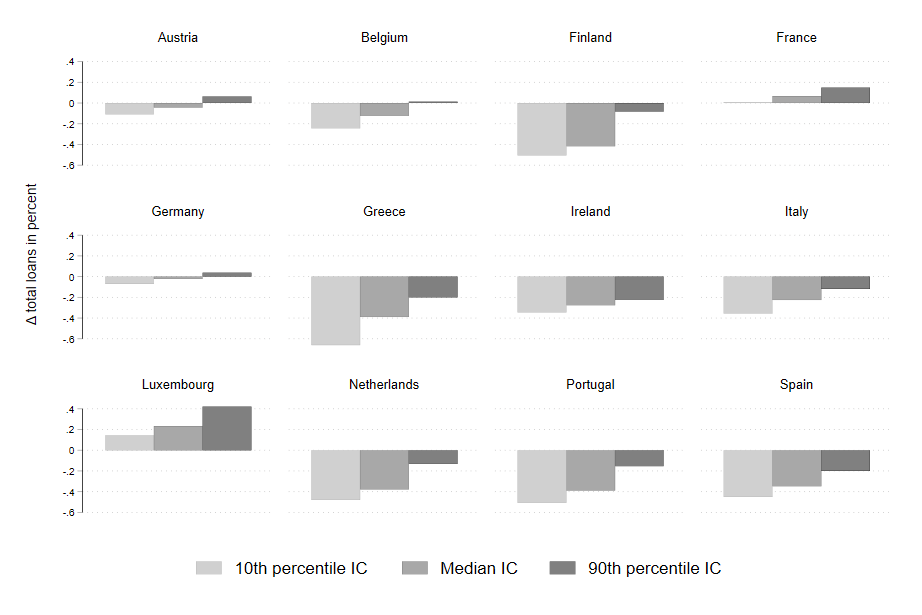

Figure 1: Impulse response of total loans to a one basis point increase in the monetary policy shock variable (Red: Low bank interconnectedness, blue: high bank interconnectedness)

Using our estimates to predict the country specific responses to a monetary policy shock, we show that countries are expected to react very heterogeneously. While Greece, for instance, is predicted to experience a contraction of loans after an interest rate hike at its 10th, 50th, and 75th percentile of bank interconnectedness, the effect of monetary policy is almost completely offset in Germany or Austria (see Figure 2).

Figure 2: Implied heterogeneous responses after 6 months to a common monetary policy shock of 1 basis point by each country’s degrees of interconnectedness

In sum, the analysis contributes to the understanding of how monetary policy is transmitted across countries in the euro area. The paper shows how heterogeneous responses can be explained by the variation in countries’ individual levels of bank interconnectedness. Furthermore, it provides a potential explanation for why recent research has found rather modest responses of the loan supply to monetary policy. Such observations appear inevitable given that many countries display levels of interconnectedness at which the reaction of loans to monetary policy is predicted to be only small or even nonexistent. Only by incorporating interbank lending into the analysis, sizable effects of monetary policy become apparent again.

IDB publication co-authored by Miguel Angel Santos (ITFD ’11, Economics ’12)

After a lengthy review process we are proud to announce that our book “City Design, Planning, Policy Innovations: The Case of Hermosillo” is published and available for download from the Inter-American Development Bank. Cutting edge research on cities featuring my work with Douglas Barrios, my colleague at the Center for International Development’s Growth Lab at the Harvard Kennedy School. Thanks to Andreina Seijas and Diego Arcia for the superb coordination and editing work.

About the book

This publication summarizes the outcomes and lessons learned from the Fall 2017 course titled “Emergent Urbanism: Planning and Design Visions for the City of Hermosillo, Mexico” (ADV-9146). Taught by professors Diane Davis and Felipe Vera, this course asked a group of 12 students to design a set of projects that could lay the groundwork for a sustainable future for the city of Hermosillo—an emerging city located in northwest Mexico and the capital of the state of Sonora. Part of a larger initiative funded by the Inter-American Development Bank and the North-American Development Bank in partnership with Harvard University, ideas developed for this class were the product of collaboration between faculty and students at the Graduate School of Design, the Kennedy School’s Center for International Development and the T.H. Chan School of Public Health.

Master’s students Analía García ’19 (ITFD) and Lorena Franco ’19 (Economics) organized the seminar to highlight research by female PhD students and professors

This May, BGSE Master’s students Analía García ’19 (ITFD) and Lorena Franco ’19 (Economics) organized the Women in Economics two-day seminar, which meant to highlight female PhD students and faculty members’ research.

Three students and four Barcelona GSE Affiliated Professors presented their work, which varied from family economics to political economics and experimental economics. More information of the speakers and their topics below.

Organizers Analía García ’19 and Lorena Franco ’19

These efforts, nonetheless, started over two months ago when both students, who are from Latin America and the Caribbean, organized an open forum on International Women’s Day. Having prior work experience and noting the clear lack of female representation in economics and academia, they wanted to expand the conversations on the topic and discuss what we could do to potentially “make it better” within their parameters. The Women in Economics seminar was born from the conversations during the first and second open forums, and thanks to the ideas of Marta Morazzoni and Claudia Meza, both PhD students at GPEFM (UPF and Barcelona GSE).

Putting this together was a challenge given this had not been done at BGSE before, but the organizers hope this was insightful for all those who attended.

More female and racial diversity in economics and academia, please!

The speakers and the titles of the work were the following (listed alphabetically):

PhD Students

Marta Morazzoni“Family Dynamics in Macroeconomics: when the representative household does not represent us anymore”

Marta Santamaría“The Gains from Reshaping Infrastructure: Evidence from the Division of Germany”

Alina Velias“When to Tie Odysseus to the Mast: Costly Commitment Under Biased Expactations”

Professors

Enriqueta Aragonés“Stability of a Multi-level Government: A Catalonia in Spain”

Rosa Ferrer“Consumers’ Costly Responses to Product-Harm Crises” and “Gender Gaps in Performance: Evidence from Young Lawyers”

Ada Ferrer-i-Carbonell“Relative Deprivation in Tanzania”

Rosemarie Nagel“Regularities in the Lab, Brain, and Field: A Cognitive Reasoning Model”

Antonia Esser ’11 (International Trade, Finance, and Development)

I started to work on remittances around three years ago when

I joined my current organization, the Centre for Financial Regulation and

Inclusion (or Cenfri in short) as a

researcher. We are an independent, not-for-profit think-and-do-tank based in

Cape Town, South Africa, trying to answer complex questions around the role of

the financial sector in improving individuals’ welfare in emerging economies.

Remittances is one of our key focus areas and we have received donor funding

from Financial Sector Deepening Africa (FSDA)

to understand why the cost of sending funds into Africa is still the highest in

the world.

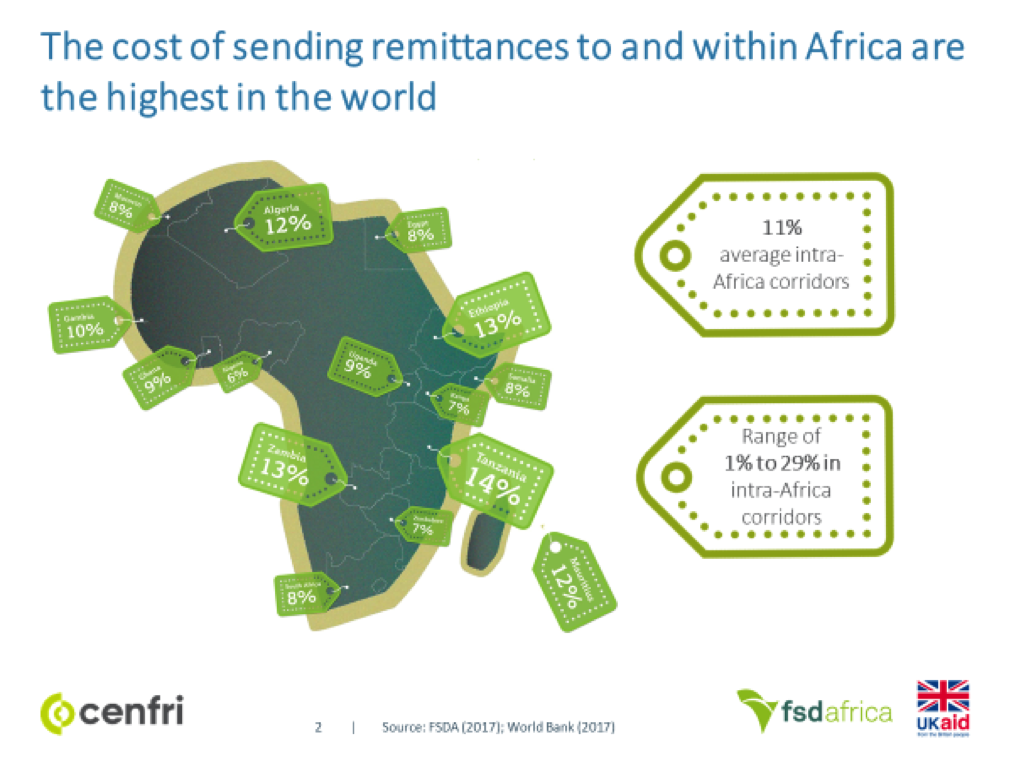

According to the World Bank, the average cost of sending remittances globally stood at just under 7% of the total value of the transfer in the first quarter of this year; in sub-Saharan Africa (SSA), consumers had to pay on average 9.25% – by far the most expensive region in the world. The SDGs want to bring down the cost to between three and five percent. Most disturbingly, intra-Africa transfers can cost way more than 15% in some corridors, even when the countries are neighbours (e.g. Nigeria and Cameroon where a transfer can cost 15%). The following graphic shows the average prices some time in 2017 between the UK and selected African countries.

The cost of sending remittances to and within Africa are the highest in the world. Sources: FSDA (2017) and The World Bank (2017)

When one considers that around 80% of African migrants stay

within Africa, this is an incredibly high burden in terms of cost that reduces

the positive impact of these essential flows for recipients. Many migrants are

therefore forced to use informal mechanisms that are often cheaper, more

trusted and more convenient. Yet informal mechanisms can be fronts for illicit

financial flows, including money laundering and the financing of terrorism.

They also indirectly influence competition as they mask the true size of a

remittance corridor, deterring providers from entering the market.

Formal remittance flows are now higher than the value of

official development assistance (ODA) and foreign direct investment (FDI). They

have shown to have significant positive impact as they flow directly in the

hands of those that rely on these funds as a primary source of income, and they

tend to be more stable than ODA or FDI.

Based on all this evidence, FSDA asked us to understand the cost

drivers and why it is still so expensive to send money to and within the

continent despite all the innovations in the FinTech space with apps from

players such as WorldRemit. We embarked

on a journey to collect evidence through stakeholder interviews (with private

sector players such as money transfer organisations, banks, FinTechs, and post

offices, as well as regulators, policy makers and experts), mystery shopping, speaking

to consumers, and ploughing through existing literature. We travelled to

important remittance markets such as Nigeria, Ethiopia, Côte d’Ivoire and

Uganda last year to understand the situation on the ground.

What I’ve learned since then is that remittances are an

incredibly complicated business. It consists of providers in the first mile

(where cash sending happens), the middle mile (where the processing of payments

happens) and the last mile (where the recipient collects the money). The value

chain is therefore very long and brings with it not only partnership complications

but also technical issues. Cross-border money transfers are heavily regulated

due to money laundering fears and severe risk exposure, but especially in

Africa capital outflows of any kind are also heavily controlled in many markets

still. To get a money transfer license can sometimes take a decade, we heard

from some providers.

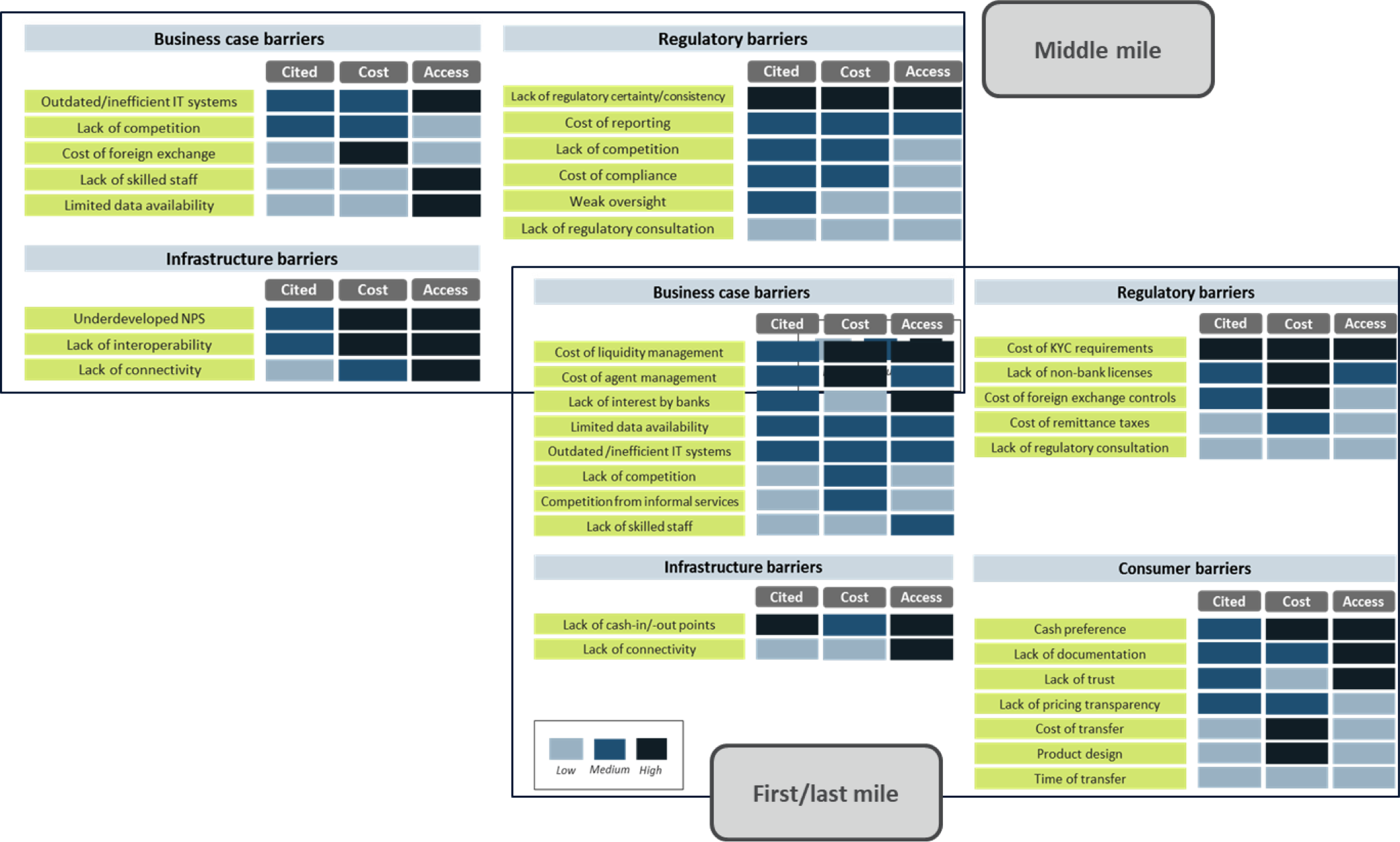

Overall, there were many interesting insights but at the end of the day we narrowed the reasons for the high costs down to four categories: business case barriers, regulatory barriers, infrastructure barriers and consumer-facing barriers. We then evaluated the number of citations and their impact on cost and access for the consumer to show how severe the barrier is for both providers and consumers:

From these insights we produced a range of reports, that you

can access here,

if you are interested, with the aim to disseminate them at key events and bring

them into relevant discussions with the various stakeholders.

One avenue we are pursuing is to reduce the regulatory

burden for providers to stimulate competition, especially in intra-Africa

corridors. Many cross-border corridors are still dominated by one or two

companies such as Western Union or MoneyGram that can set their prices freely.

They are helped by the regulation as the licensing requirements in some cases

can be incredibly high. For example, you may need to show capital of USD 20

million, be operational in at least seven countries for at least ten years. Of

course, none of the newer players that can offer cheaper remittances through

using apps, for example, can meet all

these requirements.

We were therefore on the hunt to influence regulators to revise some of the regulations. And a lot of regulation touches cross-border remittances: payment system act, banking act, foreign exchange act, agent banking regulation, e-money regulation, telecommunications regulation, cross-border transfer regulation etc – the list goes on and on. Every country seems to have their own set of rules and regulations that need to be made interoperable or at least harmonise to reduce the regulatory burdens in a value chain that can cross many jurisdictions. Definitely not an easy task! Many African countries are still heavily dependent on natural resources, such as Nigeria on oil for example. Their exchange rate with the dollar is fixed by the central bank. Yet, the Nigerian Naira is overvalued, leading to a parallel shadow market where one can get better rates for dollars on the streets of Lagos, impacting the use of formal remittance channels. But of course, the regulator is very concerned with financial stability and the impact a devaluation could have on foreign exchange reserves, inflation etc. Attracting more formal remittances does not sway the regulator enough to change the exchange rate policies. All of these realities need to be taken into consideration when approaching the regulators to try and achieve change based on research, and of course protocols play a huge role.

As part of this effort to reach regulators and based on the

research we had done, I was recently invited to attend the inaugural meeting of

experts, organized by the African Institute for Remittances (AIR), which is a programme established by

the African Union. We were called from all over the continent based on our

research and professional experience to build a cohort that would give

technical assistance to willing African regulators. Last month we met in

Mombasa, Kenya, and learned more about the planned interventions. On the one

hand, we want to achieve better remittance data quality in the individual

countries as the data can be questionable, but on the other hand we want to

assist with writing the right kind of regulation that fosters innovation,

reduces cost without reducing the access for consumers, and incentivise the

uptake of formal remittance mechanisms.

Looking foreward to three days of learning, sharing experiences and plotting the way forward with colleagues from all over Africa with @_AfricanUnion and African Institute for Remittances #remittancepic.twitter.com/kERFXsVpVC

I learned which data point to allocate to which balance of

payment code at the central bank to make sure there is consistency across

countries. I also learned how we will go about understand the regulatory

background, as of course there is a difference between de jure and de facto

regulation, i.e. we need to understand how regulation is interpreted from a

stakeholder point of view.

So far it has been an exciting journey to see how we can

take our insights into regulatory change. Some countries have already shown

interest in being assessed and assisted and we will receive a list of our

country missions as the expert cohort soon. Judging from our past work with

regulators, this process can take many months, years if not decades but the

potential impact of such fundamental changes is immense, especially for the

individual person on the ground. System-level impact takes patience and

perseverance.

ITFD taught me to be precise and on-point with my research to effect change – policy makers do not want to read 300 pages no matter how well-researched the material is. Insights need to be relatable and digestible, yet you also need to be able to raise funding for important interventions even if they seem cumbersome. We are lucky that FSDA has such a mandate and I look forward to continuing this journey with them and the African Union. Hopefully I will be able to report a significant drop in remittance prices due to regulatory change soon..ish.

It’s our second roundup of articles by Barcelona GSE Alumni who are now working as research assistants and economists at CaixaBank Research in Barcelona (see Vol. 1).

This roundup includes posts and videos from the second half of 2018 and early 2019, listed in reverse chronological order. Click each author’s name to view all of his or her articles from CaixaBank Research in English, Catalan, and Spanish.

Ricard Murillo ’17 (International Trade, Finance, and Development)

The importance of education for people’s well-being throughout all stages of their lives is beyond any doubt. At the economic level, individuals with higher levels of education tend to enjoy higher employment rates and income levels. What is more, all the indicators suggest that in the years to come, the role of education will be even more important. The challenges posed by technological change and globalisation have a profound effect on the educational model.

Faced with the major transformation of the productive system brought about by technological change and globalisation, as well as the challenges posed by an ageing population, it is important to take action to strengthen social cohesion – an indispensable element if we are to carry out reforms that foster an inclusive and sustained form of growth.

The US and the euro area are at different stages of their financial cycles: while the Fed’s monetary policy is close to becoming neutral or even restrictive, the ECB remains in clearly accommodative territory. However, to some extent, both are facing a common risk: the decoupling between their monetary policy and the financial conditions. The two institutions will try to manage their tools carefully, in order to facilitate a gradual adjustment of the financial conditions in the US and, in the case of the euro area, to keep them in accommodative territory.

Gerard Arqué ’09 (Macroeconomic Policy and Financial Markets)

Thanks to the implementation of the measures introduced following the financial crisis, today the financial sector is more robust than before. This will help to minimise the impact to the economy and financial stability in periods of upheaval, since countries with better-capitalised banking systems tend to experience shorter recessions and less contraction in the supply of credit. However, the outstanding tasks we have mentioned should be properly addressed sooner rather than later.

Central banks are facing the challenge of removing the extraordinary measures imposed during the financial crisis of 2007-2008 and the subsequent economic recession. In normal times, central banks would simply raise interest rates up to the desired level. However, monetary policy is currently in a rather unconventional cycle.

Master project by Samuel Jones, Annanya Mahajan, Maria Oliva, Debora Reyna, Marta Vila

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

We capitalise on the 2006 implementation of a minimum wage for the hospitality sector to make well-evidenced inferences about the impact of the upcoming National Minimum Wage (NMW) Legislation on low-wage workers. Our paper focuses on the two largest low-wage sectors currently without minimum wage regulation, which are manufacturing and construction. Two regression specifications and sensitivity analysis are used to provide insights into the implication for wages, hours worked, employment, formality and poverty rates. In light of our results and a comprehensive review of the literature, we conclude that the NMW will be largely beneficial for low-wage labourers. Our critical recommendation for policymakers is the need for complementary policies to ensure compliance and facilitate the transition of vulnerable groups (particularly black women) into the formal sector.

Conclusions and key results:

From our first specification, our analysis suggests that wages and hours worked will increase in manufacturing and construction sectors as a result of the minimum wage, mostly driven by increases for black and female workers. Although the policy is likely to increase the formality rate among male workers, we predict formality will fall among females as employers try to circumvent the legislation. Therefore it is crucial that adequate complementary policies are implemented to ensure the benefits are captured by all population groups. Our second specification exploits the variation in the median wage across provinces. In doing so, we find no significant effect on wages, which signals regional impacts of the minimum wage are fairly homogeneous. Therefore, compared to other countries adopting a similar policy, the implementation of safety-nets combating the adverse effects of the minimum wage will be relatively more straightforward. By conducting sensitivity analysis around compliance rates and poverty lines already stipulated in the literature, we predict between 100,000 and 300,000 manufacturing and construction workers will be lifted out of wage poverty as a result of the minimum wage. We combine our empirical partial equilibrium analysis with theoretical general equilibrium forces to provide statements on the anticipated lower bound of wage changes.

Miguel Angel Santos was interviewed on CNN’s Global Portfolio where he shared his analysis of the economic crisis in Venezuela.

Master’s alum Miguel Angel Santos was interviewed on CNN’s Global Portfolio where he shared his analysis of the economic crisis in Venezuela. From his post on LinkedIn:

“The collapse of Venezuela has a magnitude never before seen: it is the only country in the top ten of falls in GDP in five years in history (ninth, 45%), of falls in imports (third, 75%), and is also projected as one of the most intense hyperinflations in history, comparable only to Germany and Zimbabwe. There is no country on those three lists which has suffered collapses in imports, production, and hyperinflation at this level of intensity. It’s unprecedented.”

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.