Alum Lucila Mederos ’11 with Barcelona GSE founder Andreu Mas-Colell in Chicago last week

Last week, I had the pleasure of attending the ceremony where Prof. Andreu Mas-Colell was named Doctor Honoris Causa by the University of Chicago. As an alum of the Barcelona GSE, I felt honored to watch the founder of our school receive this recognition and to represent the alumni community here in Chicago.

After the ceremony I got to join Prof. Mas-Colell, his family, the President Emeritus of the University of Chicago and Chairman of the Barcelona GSE Scientific Council Hugo Sonnenschein, and the other recipients for lunch, where I took this photo. Professor Mas-Colell seemed very grateful to receive the Honoris Causa distinction and to have the GSE represented at the event.

Lucila Mederos ’11 (Master Program in International Trade, Finance, and Development) is Project Manager for Euromonitor International’s LATAM Custom Research Team in Chicago, IL (USA). Follow her on Twitter @lucilamederos

By Iacopo Tonini ’15, current student in the International Trade, Finance and Development program. Follow him on Twitter @iacopotoni

On April 8th Professor Ruben Durante (Sciences Po) visited the Institute of Political Economy and Governance (IPEG) to present his latest research paper, “Attack when the world is not watching? International Media and the Israeli-Palestinian conflict” (coauthored with Ekaterina Zhuravskaya, Paris School of Economics). The title clearly suggests that the article relates to the Israeli-Palestinian conflict, however the research aims at demonstrating a more general result. Indeed, the objective is establishing a causal relationship between unpopular policy choices and news with a “highly relevant” media content.

“I have noticed that my older daughter steals her brother’s toys when we (the parents) are not home”, the Italian professor stated cheerfully while explaining where he had initially gotten the idea for the research. The process seems to make sense. In the case of an influential conflict such as the Israeli-Palestinian one, it could well be the case that the factions involved wait for the world to look away before coordinating and ultimately launching a brutal offensive – or interrupting a ceasefire after a period of peace.

Beyond the intuitive example extrapolated from the professor’s family life, more concrete cases are the following. On the very same day in which the Italian National team qualified for the World Cup final (July 13, 1994), the Berlusconi government passed and approved an emergency decree – recently renamed the “save-the-thieves” decree– that allowed several politicians accused of corruption to avoid imprisonment, and keep working unscathed. Another example is the start of the Russian military operations to invade Georgia. The Russian army received the order to attack during the opening ceremony for the 2008 Beijing Summer Olympics. Finally, during the 2014 FIFA World Cup, while at the stadium Mineirão in Belo Horizonte the German national team was inflicting a historical débâcle to the Seleçao, Israel launched the operation “Protective Edge” against Gaza.

News item about an unpopular policy appears below news about the World Cup qualifier in this Italian newspaper.

“Governments are accountable to the extent that the public is informed about their actions. Mass media ensure accountability by informing citizens about government actions (Besley and Prat, 2006; Snyder and Stromberg, 2010),” answered the professor to one of the questions asked by a scholar. “Yet, how effectively mass media inform the public depends, among other things, on the presence of other newsworthy events that may crowd out the news coverage of governments’ actions (Eisensee and Stromberg, 2007).” The assumption on which the study is built – and that the Israeli-Palestinian case seems to demonstrate – is that politicians might exploit the presence of other “newsworthy events” to put forward unpopular actions so that they coincide with major events that distract the audience.

However, could this perhaps be the overly-pessimistic vision of the researcher? The data shows otherwise. In particular, Professor Durante shows in his work that when the Israeli-Palestinian conflict is given coverage in the media, there is a 12% increase in the Google searches related to the topic.

Let us focus on the case studied in the paper: the Israeli-Palestinian conflict.

Since the 70s, the Israeli government has put a great effort in projecting a positive image of Israel and its army abroad. This policy is denominated Hasbara, which in Hebrew means “explanation”, and entails the production of informative material on issues regarding Israel and the Middle East. Furthermore, Hasbara includes collaborations between international and local journalists, and social-media usage to influence public opinion. Nothing similar is in place in Palestine.

In his article the Professor writes: “Most likely, in an armed conflict nothing has a worse impact on the international public opinion than civilian casualties.” The factions involved seem to be perfectly aware of the primary role mass media have in informing, and thus influencing, public opinion. Evidence of this is found, for instance, in the words of the Prime Minister Netanyahu who, when interviewed by the CNN about the numerous civilian victims, commented: “[Hamas] wants to pile up as many civilian dead as they can…they use telegenically dead Palestinians for their cause.”

By combining daily data on attacks on both sides of the conflict with data on the content of evening news for top U.S. TV networks, the authors show that: “Israeli attacks are more likely to be carried out when the U.S. news are expected to be dominated by important (non-Israel-related, such as an election or the Super Bowl) events on the following day.” Specifically, the empirical findings indicate that the strategic timing of the Israeli army is less relevant in a period of intense fighting as opposed to attacks in a period of relative peace. Moreover, the attacks are strategically planned only in the case when there is the possibility of civilian casualties. Thus, the facts documented in the paper confirm that the aim of Israel is that of “minimizing negative international publicity” – and in the case of graphic or emotional contents regarding civilian victims, would result in a strong, negative impact on the American public opinion.

In contrast, the researchers find “no evidence that attacks by Palestinian militant groups are timed to U.S. news pressure.” This might be reflecting the marked gap that exists between the two arrays: unlike Israel, Palestine does not have a structured or well-organized army, nor does it have the same level of resources that would allow it to plan such attacks strategically. Nevertheless, it should be noted that this does not exclude the possibility of Palestine’s lack of interest towards shaping American public opinion.

Beyond the interesting findings of the research on the role international media plays in the Israeli-Palestinian conflict, this study also reminds us of the powerful responsibility it holds. In particular, mass media is a watchdog powerful enough to influence the actions of governments by simply carrying out their mission of informing citizens. This becomes even more important when considering the exponential interconnectedness of people throughout the globe via technological progresses.

References

Besley, Timothy and Andrea Prat, “Handcuffs for the Grabbing Hand? Media Capture and Political Accountability,” American Economic Review, 2006, 96 (3), 720–736.

Eisensee, Thomas and David Stromberg, “News Droughts, News Floods, and U.S. Disaster Relief,” The Quarterly Journal of Economics, 05 2007, 122 (2), 693–728.

Snyder, James M. and David Stromberg, “Press Coverage and Political Accountability,” Journal of Political Economy, 04 2010, 118 (2), 355-408.

Barcelona GSE alum Miguel Ángel Santos (ITFD ’11 and Economics ’12) is Senior Research Fellow at the Center for International Development at Harvard University. He recently won an award for a paper he has written with Harvard Professor Carmen Reinhart. In this post, he shares some background on the paper and some results.

I approached Carmen Reinhart last year, while I was a Mason Fellow at the Kennedy School. She said she would be very interested in writing something about Venezuela. It turns out that Venezuela is such an anachronic, chaotic economy, that it allows us to study some economic phenomena in a way no other place does.

My idea was writing about foreign debt sustainability and default probabilities, etc. Carmen suggested otherwise. After all, lots of people have been working on foreign debt sustainability, and it would not be interesting adding to that pile of work.

Instead, she suggested looking into domestic debt default via financial repression, and associating that to leakages in the capital account that in turn weakened the foreign asset position. It goes against some market analysts’ assessment that Venezuela can go wild internally, wild being able to serve its external debt without any trouble. So we used two modified formulas for estimating financial repression for the previous 30 years, differentiating free market years from years of exchange controls.

Our results

We proved that financial repression it is not only significantly higher in periods of exchange controls, but also that the sheer size in Venezuela was astounding, equivalent to more developed countries with much larger internal debt-to-GDP ratios. That is to say, with a smaller stock of domestic debt, the Venezuelan regime needs a lot more repression to collect that. So they actually engineer it, creating mechanisms to produce it: right now inflation is running at a rate five times higher than yields on domestic bonds or bank deposits.

We moved on to show that capital flight, conceived in broader sense, including the over-invoice of imports, was higher in periods of exchange controls. Since financial repression is rampant in periods of controls, people will run risks just to jump out of domestic currency and get into dollars (capital flight). They do that by two means: buying dollar-denominated bonds that the government has been selling in exchange for domestic currency, and over-invoicing imports. We measured the latter by a very innovative process, contrasting Central Bank reported imports with the sum of imports reported at Venezuelan customs. The difference is not only significantly higher across years of controls, but over those years it is 3-4 standard deviations away from the distribution of this error worldwide.

I presented the paper two weeks ago in San Juan, Puerto Rico, within the Business Association of Latin American Studies (BALAS), where it was granted the Sion Raveed Award, given to the best paper of the conference.

Comments welcome from the Barcelona GSE community

CID has published the paper on their working paper series. All comments from the BGSE Alumni and scholars community are welcome at this point. It is a modest paper, dealing with a small, crazy economy. And yet I think it makes a significant contribution.

Jana Bobosikova ’10 is a graduate of the Barcelona GSE master program in International Trade, Finance and Development.

I was sitting in the Conference Room 1 at the United Nations in New York in summer 2013 amidst the Nexus Global Youth Summit attendees, listening to the opening address from Roland Rich, Executive Head of the United Nations Democracy Fund. The message I was hearing was clear and bold: we are here to take action. Not “we” as in policy makers and government funded multilateral agencies” but rather “we” as in Nexus, the global movement of Doers from the circles of the largest philanthropists, hardest working and most daring social entrepreneurs, investors, international advocates and NGOs.

Part of me was elated: so many influencers, all on the same page, with substantial financial and human commitment to contributing to making the world a better place!

Another part of me, the one I cultivated through the study of economic analysis at the ITFD program at Barcelona GSE, was a bit nervous about so much “good doing”.

I felt too aligned with the work of my former professor Xavier Sala-i-Martin and William Easterly that suggest that much of external help to date has had none or negative effect on socio-economic growth to simply embrace the possibility that Nexus Youth Summit was different and effective.

I sent a mental greeting to Prof. Antonio Ciccone and his often restated quest for the “one-handed economist” – creating one best solution with all relevant sets of variables – conclusions with no caveats “on the other hand.” Had I found them? What were the Nexus development solutions that gathered at the UN?

Let’s see:

We have been conditioned to include savings as a basic variable for economic growth models. At Nexus, Aron Ping D’Souza felt so compelled by the meeting of Sir Richard Cohen at an earlier Nexus Europe Youth Summit that he started an impact investing annulation fund, using the best practice from classic and impact investing to target over AUS$1.7 trillion pension funds to a creating a 2.0 return for the economy.

We learned about girls’ education challenges in developing countries. One of Nexus’ members, Nikki Agrawal, invested in researching and launching menstruation-absorbing underwear to address one of the most significant school attendance problems for girls.

We studied about how to create policies that incentivize investing into R&D for a healthier global population. At Nexus, it was a great honor to be joined by Jake Glaser, the son of Elizabeth Glaser who pioneered and prompted research and development in pediatric AIDs in early 1990s. It was the one case of AIDS transmission via blood transfusion during Elizabeth Glaser’s giving birth and her subsequent fight to save her children that has kickstarted the largest research and movement on eliminating pediatric AIDS – a vision that is now becoming a reality.

I could probably keep going and catalogue the amazing encounters and inspiring efforts of the hundreds (!) of international innovators, family offices that fund some of the largest projects as well as startup social entrepreneurs – that make up Nexus.

And maybe I should, so that the passion and commitment of the Nexus movement and the research and rigorous analysis from the realms of development economists could start catalyzing into aligned efforts to improve international trade, finance and socio-economic development.

Barcelona GSE grad Alvaro Leandro looks at the EU’s Stability and Growth Pact through the lens of the draft budget plans of France and Italy.

The following post by Alvaro Leandro (ITFD’13 and Economics ’14) has been previously published by Bruegel.

Mr. Leandro is Research Assistant at Bruegel in Brussels, Belgium.

The EU’s fiscal framework, the Stability and Growth Pact (SGP), is a complicated system of fiscal rules. Rather than trying to assess the virtues and failures of the SGP, this blogpost aims at understanding its complex rules through the lens of the draft budget plans of France and Italy. France is in the corrective arm of the SGP, while Italy is now in the preventive arm, which allows the examination of various SGP requirements, such as the

structural balance pillar,

expenditure balance pillar,

and the debt criterion

which apply to countries in the preventive arm (like Italy), and the

headline budget deficit criterion,

the structural balance criterion,

and the cumulative structural balance criterion

which apply to countries in the corrective arm (like France). We also discuss the rules regarding financial sanctions.

On 28 November 2014, the European Commission released its opinions on the euro area Member States’ Draft Budgetary Plans for 2015. The purpose of these opinions is to assess each country’s compliance with the SGP, and to recommend appropriate action if there are risks of non-compliance.

Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”

One of the surprises was that, in the case of Italy and France (as well as Belgium), the Commission decided to postpone its recommendations until March 2015, “in the light of the finalisation of the budget laws and the expected specification of the structural reform programmes announced by the authorities“. Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”, according to the Commission.

The Framework

The Stability and Growth Pact is composed of a preventive and a corrective arm. The corrective arm is called the Excessive Deficit Procedure (EDP), which is triggered for countries with a general government deficit larger than 3 percent of GDP or with debt larger than 60 percent of GDP not being reduced at a satisfactory pace. France is currently under the corrective arm and Italy was as well until 2013. Italy is therefore now subject to the rules of the preventive arm.

Source: Country Stability and Convergence Programmes for MTOs, AMECO for forecast of 2014 and 2015 Structural Balances

Notes: Data labels are for the MTOs. According to the Treaty on Stability, Coordination and Governance (TSCG), signed by all euro area members in March 2012, all signatory Member States must have an MTO higher than -0.5% of GDP (or -1% for countries with a debt/GDP ratio lower than 60%). The “fiscal” part of the TSCG is often called the ‘Fiscal Compact’.

The fundamental variables used to assess compliance with the preventive arm of the SGP are the country-specific medium-term budgetary objectives (MTOs), which are defined as structural balances (a measure of the government budget balance adjusted for the economic cycle and one-off revenue and expenditure items; this blog post by Zsolt Darvas explains the estimation methodology and why it has some drawbacks). MTOs are chosen by each Member State following strict guidelines set out by the Commission, in order to ensure sustainability in its public finances (a higher MTO is required from countries with a high debt ratio or with a rapidly-ageing population faced with increasing age related expenditure for example, while the ‘Fiscal Compact’ limits the MTO for euro area member states, see the notes to Figure 1). A few examples of MTOs can be found in Figure 1: France, Italy and Spain have an MTO of 0 percent of GDP, while Germany’s MTO is -0.5 percent. This means that in the case of Germany, for example, a structural deficit of 0.5 percent of GDP is deemed enough to ensure the sustainability of its public finances.

The Fiscal Compact is not binding for non-euro area Member States, which therefore have more freedom in setting their MTOs. For example, Hungary has an MTO of -1.7 percent, the Polish and Swedish MTO is -1 percent, while it is zero for the United Kingdom.

To comply with the preventive arm of the SGP, all Member States must be at their MTOs or be on a path to reach them, with an annual improvement of their structural balance of 0.5 percent of GDP towards the MTO as a benchmark.

A higher effort might be required for countries with high debt/GDP ratios and pronounced risks to overall debt sustainability. A higher effort is also required in good economic times, and a lower effort in economic downturns. A Member State could also be allowed to deviate from the adjustments if it experiences “an unusual event outside its control with a major impact on the financial position of the general government”.

Therefore compliance with the preventive arm is not defined by the Member State’s structural balance, but by its path towards the MTO.

Italy

Structural balance pillar: Table 1 shows the recommended path for Italy. On the 28th of November 2014 the Commission decided that “severe economic conditions” (namely a real GDP contraction and a large negative output gap: see Table 3) justified that Italy is not required to adjust its structural balance towards the MTO by the 0.5 percent of GDP benchmark in 2014. This is why the required change in the structural balance for 2014 is 0. Italy had originally planned a large correction of its structural budget for 2014 in its 2013 Stability Program, of 0.7 percentage points. In its Draft Budget Plan for 2014 Italy revised this adjustment to 0.3. Finally it invoked Article 5 of Regulation 1175/2011 in its 2014 Stability Program which allows a deviation from the required adjustment “in the case of an unusual event outside the control of the Member State concerned which has a major impact on the financial position of the general government”. The required adjustment is also 0 in 2013 for the same reason: negative real output growth makes Italy eligible to the escape clause. In 2015 real GDP is forecast by the Commission to increase by 0.6 (see Table 3), which means that Italy can no longer apply for the escape clause regarding economic downturns.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of Italy (28 November 2014), European Commission Autumn Forecast (November 2014), Italy’s Stability Programme April 2014, Italy’s Stability Programme April 2013, Vade Mecum on the Stability and Growth Pact (May 2013)

Note: ΔSB denotes the percentage point change in the structural balance. MLSA: minimum linear structural adjustment. DBP: draft budget plan

(1): Deviation of the growth rate of public expenditure net of discretionary revenue measures and revenue increases mandated by law from the applicable reference rate in terms of the effect on the structural balance. A negative sign implies that expenditure growth exceeds the applicable reference rate.

Expenditure balance pillar: Member States in the preventive arm of the SGP also have to comply with the expenditure benchmark pillar, which complements the structural balance pillar. It requires countries that are not at their MTO to contain the growth rate of expenditure net of discretionary revenue measures to a country-specific rate below that of its medium-term potential GDP growth. This medium-term potential GDP growth is calculated as a 10-year average (of the 5 preceding years, the current year and forecasts for the next 4 years), and in the case of Italy it is 0 percent in 2014 and 2015. Had Italy been at its MTO it would have had to contain net expenditure growth to 0 percent. However, not being at its MTO, it is required to contain net expenditure growth to a reference rate below medium-term potential GDP growth: -1.1 percent in 2015 (which is calculated so that it is consistent with a tightening of the budget balance of 0.5 percent of GDP when GDP grows at its potential rate). The applicable reference rate in 2014 is 0 because of the “severe economic conditions”. In 2013 the applicable reference rate was 0.3, which is different to that in 2014 and 2015 because it is revised every three years. The commission allows one-year and two-year average deviations of a maximum of 0.5 pp of GDP in terms of their impact on the structural balance. In 2015 the deviation in terms of its effect on the structural balance is forecast to be of 0.7 pp. of GDP, which is a deviation larger than the allowed 0.5 pp.

Debt Criterion: Countries which have recently left the EDP are subject to a 3-year transition period aimed at ensuring that the debt level is being reduced at an acceptable pace. Italy is in such a transition period, since it left the EDP in 2013. It is thus subject to required medium-term linear structural adjustments (MLSAs) aimed at ensuring that it will comply with the debt criterion. These MLSAs are formulated in terms of adjustments to the structural balance. Since Italy is in the preventive arm and therefore also subject to required adjustments towards the MTO, the largest one is applicable. The 2.5 pp. MLSA in 2015 (larger than the 0.5 pp. required change under the preventive arm) is at serious risk of not being met according to Commission forecasts. This violation of the debt criterion could lead to a reopening of the Excessive Deficit Procedure.

Commission’s view: In its opinion on Italy’s Draft Budget Plan released at the end of November 2014, the Commission points to risks of non-compliance with the requirements of the SGP, and “invites the authorities to take the necessary measures […] to ensure that the 2015 budget will be compliant with the Stability and Growth Pact”. It then says that “The Commission is also of the opinion that Italy has made some progress with regard to the structural part of the fiscal recommendations issued by the Council in the context of the 2014 European Semester and invites the authorities to make further progress. In this context, policies fostering growth prospects, keeping current primary expenditure under strict control while increasing the overall efficiency of public spending, as well as the planned privatisations, would contribute to bring the debt-to-GDP ratio on a declining path consistent with the debt rule over the coming years.”

France

Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit.

Headline budget deficit criterion: Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit. France has now been under the EDP for 5 consecutive years, and is subject to requirements set out in the latest Council recommendation to end the excessive deficit situation (June 2013). The recommendation released in 2009 originally planned a correction of the deficit (below 3 percent) by 2012, which was then postponed to 2013 in view of the actions taken and the “unexpected adverse economic events with major unfavourable consequences for government finances”. In June 2013, the Council again postponed the correction of the deficit to 2015 for the same reasons: France fell slightly short of the required 1 percent average annual fiscal effort for the period 2010-2013 (the actual average annual fiscal effort was 0.9 percent), but this was again against a backdrop of “unexpected adverse economic events”.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of France (November 28, 2014), Council recommendation to end the excessive deficit situation (June 2013), European Commission Autumn Forecast (November 2014)

Note: ΔSB denotes the percentage point change in the structural balance

The latest Council recommendation (June 2013) sets out a path for France’s headline government balance, which you can see in Table 2. By 2015, the headline balance should be reduced to -2.8 percent of GDP. The forecast headline balance of -4.5 percent falls significantly short of this requirement.

Structural balance criteria: Additionally the adjusted change in the structural balance from 2014 to 2015 is forecast to be of 0.0 pp., and its cumulative change from 2012 to 2015 is forecast to be 1.6 pp., falling short of the requirements of 0.8 pp. and 2.9 pp. respectively (1). The structural budget also deviates from the requirements for 2014.

Commission’s view: Thus France is “at a risk of non-compliance” with the SGP, and, contrary to Italy, the Commission “is also of the opinion that France has made limited progress with regard to the structural part of the fiscal recommendations issued by the Council […] and thus invites the authorities to accelerate implementation”. In his letter to the President of the European Commission, France reiterated its determination to go ahead with reforms, most notably in the labour market. It remains to be seen whether progress by March 2015 will be assessed to be sufficient by the Commission.

Table 3: France and Italy: main macroeconomic indicators in 2014 and 2015

Sanctions

Non-compliance with the SGP can lead to sanctions. In the preventive arm, a Council recommendation which is not respected can lead to an interest-bearing deposit of 0.2 percent of GDP. A euro-area country in the corrective arm of the SGP may be required to make a non-interest bearing deposit until the deficit has been corrected, after which it can also be sanctioned with a fine worth up to 0.5 percent of GDP (with a fixed component of 0.2 percent of GDP and a variable component (2)). France and Italy are both at a risk of non-compliance with the requirements of the SGP. Failure to meet the required efforts in terms of fiscal consolidation and structural reforms by March 2015 could bring them closer to possible sanctions, unless the flexibility of the SGP is stretched further. Recent growth and inflationary figures suggest continued weak economic activity, and if economic data of 2014 qualified for “severe economic conditions”, 2015 may qualify too, especially if growth and inflation will disappoint relative to the November 2014 ECFIN forecasts. And in the preventive arm, structural reforms which have a verifiable positive impact on the long-term sustainability of public finances (such as by raising potential growth) could be considered when assessing the adjustment path to the medium-term objective.

Notes:

(1) The adjusted changes in the structural balance correct for the negative impact of the changeover to ESA 2010 as well as for changes in potential growth and revenue windfalls/shortfalls.

(2) This variable component is equal to “a tenth of the absolute value of the difference between the balance as a percentage of GDP in the preceding year and either the reference value for government balance, or, if non-compliance with budgetary discipline includes the debt criterion, the government balance as a percentage of GDP that should have been achieved in the same year according to the notice issued”

Post by Nadim Elayan, current student in the Barcelona GSE’s Master Program in International Trade, Finance and Development. Follow him on Twitter @Nadim1306.

It is unethical that 20-year-old guys with no studies whatsoever earn 20 million euros a year by just kicking a ball during one hour and a half once a week whereas doctors who have studied almost an entire decade and save human lives every day earn 500 times less.

A fair society should compensate with higher wages people who save human lives than people that entertain us during the weekends.

How can we stand by watching soccer players earning millions a year while there are people starving in the same country?

Most of us will have probably heard these sentences or similar ones regarding the large wages that soccer players earn and even that this situation is immoral or a bad incentive for kids to have a good education. But is this true? Do soccer players actually earn more than doctors?

Before analyzing the Spanish soccer labor market or discussing the ethical implications of this situation we need first to say that this is not true. The fact that we can name some players with shockingly salaries it does not mean that on average soccer players earn more than doctors, or even more than the average salary of a specific country. In order to compare professions we need a non-biased sample. We cannot look at the best soccer player in the whole history, Lionel Messi, and compare his salary with a regular doctor in Barcelona and then conclude that soccer players earn 500 times more than doctors. This situation would be the same as looking at Yao Ming, a Chinese basketball player with a height of 7.6 feet (2.29 meters) and a weight of 310 pounds (141 kg) and wrongly concluding that Chinese people are 2 feet taller (0.6 meters) and they weigh 130 pounds (59 kg) more than the average European citizen. Thus Lionel Messi is not the best representative of soccer players’ earnings terms as Yao Ming is not the best representative of the Chinese citizen in physical terms.

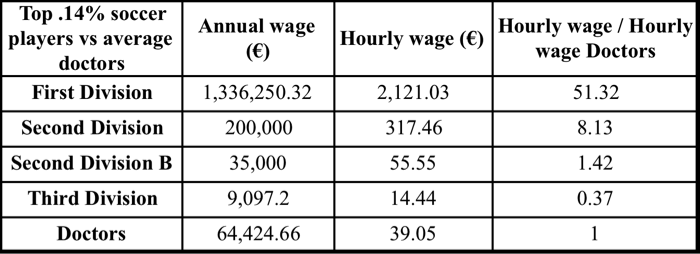

In Spain there are more than 700,000 professional and amateur soccer players according to the Real Federación Española de Fútbol and most of them work without a salary or earning below the minimum wage and that is why most of them need another job. There are about 500 players earning on average a wage of 1,336,250.32€ a year, the ones playing in the First Division and also about 500 players earning a wage below 200,000€ on average, the ones playing in the Second Division[1]. So in total we can count that within Spain there are only around 1000 players earning a salary way above the salary an average doctor earns, which in Spain is 64,424.66€[2] on average.

We would have also to take into account that the soccer professional life is barely higher than 10 years while the doctor’s one would be around 35 to 40 years. All this without considering the high risk of injury a soccer player faces every day that would leave him without any salary at all the rest of his life. But of course on the other hand soccer players work no more than 15 hours a week on average and therefore the wage for this .14% gets even larger if calculated per hour. So in order to compensate for the differences in professional lives we should observe that soccer players would earn at least 3.5 to 4 times more than doctors.

Table 1. Source: OCDE and El Pais.

We can see that these 1,000 players, .14% out of the total, earn way more than doctors on average but the next group of professional players who earn the most are the ones playing in 2nd B Division. There are 2,000 players in this Division earning on average 35,000€, what is actually less than doctors, but the hourly wage would still be above, 55.55€ per hour. If we go further away focusing in the ones playing in 3rd Division their hourly wage is 14.44€ already below the doctors one.

Summing up .14% out of total soccer players earn a salary way above the doctors’ average that more than compensates their shorter professional life. The next .28% still earns a higher hourly wage than doctors’ average but not enough to compensate their shorter professional life. So the rest 99.58% of the soccer players do not earn more than the average salary of a doctor. Actually most of them do not earn anything and some of them earn a little bit if they are in the starting line-up or for each victory.

Once showed that the average soccer player does not earn more than the average doctor, not even more than the minimum wage, we will analyze the soccer labor market and try to explain why this 0.14% earn so much money.

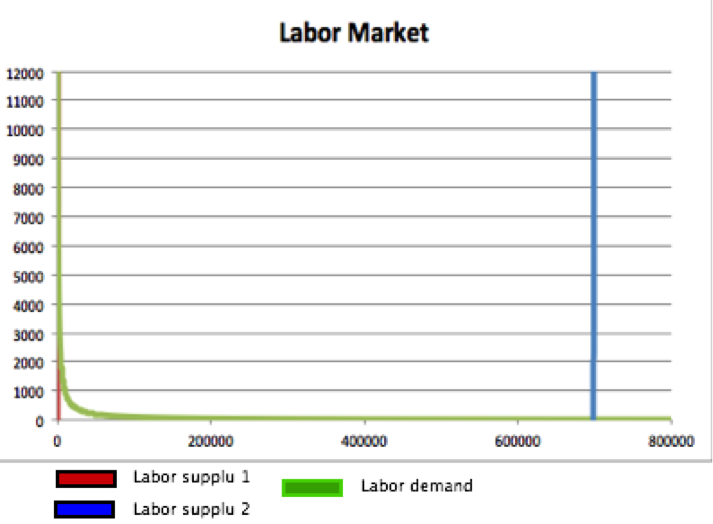

Analyzing the soccer labor market

First we will focus on the soccer labor demand. It is extremely high for very low values of labor hired, so for the first soccer players in the First Division and even for the Second Division. It is easy to show this by noticing that European societies are willing to fill 50 to 90 thousand people stadiums more than 30 times a year at prices between 20€ and 200€ per person each game. Therefore demand is huge. But for higher levels of labor hired, so 2nd Division B, 3rd Division and following Divisions the labor demand is very low and close to 0. Usually these games are free attendance or paying a type of mandatory lottery participation.

Now we can talk about the labor supply. In this case we can separate it into 2 subgroups. For simplicity we just divide the market in 2 subgroups, the first is composed by the 1000 soccer players playing in First or Second Division and the rest of the players. Even when considering perfect inelastic labor supplies we see very high wages for the first subgroup due to the high labor demand and also due to the very scarce labor supply of this type. Whereas for the second subgroup the wages are extremely low, almost 0, because of the low labor demand and the extremely high labor supply.

Ethical implications

People think constantly about soccer, they fill large stadiums paying really high prices and spend almost 100€ a year to buy the newest shirt of their team. Furthermore between 20 and 60 percent of total TV spectators watch Champions League games in prime time and even watch TV programs and listen radio programs that only talk about soccer… In conclusion people spend a large fraction of their income and time on soccer. Is it unethical that a large fraction of this cake is sent to workers via wages?

If we think that this 0.14% of total soccer players earn too much we should then say where we send this money generated by them. Would it be more ethical to let billionaire soccer teams owners to keep a larger fraction instead? In a non-profit Solow Economy, total output goes to capital and labor, therefore , high output will translate into high wages (for one club L=25, so very low). For example in F.C. Barcelona the season 2014-2015 has spent 509 million € in total and 288.9 million € of them only in players’ wages. So 56.76% of total expenditure goes to their soccer players[3].

Secondly if we speak about fairness we should want a society that creates only inequality from people who had the same life opportunities but they succeeded and managed to highlight in their respective fields and dislike inequalities coming from differences in opportunities. Since playing soccer is not expensive, all kids can play it everywhere and the best clubs, knowing this, have scouters all over the world. This makes this labor market pretty competitive, almost every kid at age 12 has at least tried once to get in F.C. Barcelona or Real Madrid through many tests these clubs organize everywhere. Thus, the kids who finally succeed must have been better than almost every kid of their age in the planet. All this combined make the differences in wages created be explained by differences in talent and effort no matter the race, family’s economic status or better education opportunities. In fact, most of the best soccer players like Pelé, Maradona, Ronaldinho, Cristiano Ronaldo, Samuel Eto’o, so also the ones earning high wages, come from very poor families.

Lastly the fact that there are people starving in a country has nothing to do with the fact that there are soccer players earning large wages because this is determined by a very large labor demand and a very scarce labor supply for this very specific First and Second Division players. The labor demand is determined by the society’s taste so we should blame this taste if we think that the amount of money generated by soccer is disproportionately huge and instead we should allocate this exact amount of time and income to fight hunger and other problems we find more relevant.

[1] Every team posts their wage budget annually. These values are obtained by dividing the total wage budget over the total players in that division.

Víctor Burguete ’11 (International Trade, Finance and Development) is an Economic Researcher and Public Policy Analyst at IESE’s Public-Private Sector Research Center (IESE-PPSRC) in Barcelona. In this post, he shares the process of preparing a policy brief on Spanish policy reforms and provides an overview of the brief’s findings.

Preparing a Policy Brief like this took me over a month. It is necessary to consider than working in a research institution implies getting involved in many projects and there is usually less time than what I would like to devote to one specific project. In my opinion, it is very important to work open-minded and to continuously consider the possible connections among different projects. In the case of this Policy Brief, most of the data (international economic policy recommendations) were collected during the past few months. In late September I proposed this topic and the IESE-PPSRC research center decided to inaugurate these series of papers. After reviewing the literature (Table 1), I analyzed the data and I started creating some graphs and building the story I wanted to tell. Of course, the final text was reviewed several times until it was finally published.

“Spain’s response to EC and OECD economic policy recommendations” analyses the overall reformist progress of the Spanish Government in an international perspective. According to the international assessment, Spain ranks as one of the top reformers in the Euro Area and the EU as a whole. A second insight one gets from our Policy Brief is that Spain’s delivery, in relative terms to other countries, accelerated between 2011 and 2013.

Of course, this is the general trend and the Policy Brief offers details on the progress in the 18 policy sub-areas we cover at the SpanishReforms project, including how the reform priorities prescribed to Spain by these institutions have changed over time. Substantial progress is recognized in addressing the financial system reform, mainly in the area of recapitalization and restructuring but also by adopting other financial measures. However, both the OECD and the EC point to active labour market policies and professional services as the main structural reforms lagging behind.

More information in www.spanishreforms.com, a new an academic, non‐governmental website that aims at being a useful reference for those interested in independent, rigorous and up‐to‐date information about the Spanish economy and its economic policy reforms.

Alex Hansson ’13 (International Trade, Finance and Development) is an Analyst at Tribus Capital Partners in Zurich, Switzerland. Previously he was External Asset Management Analyst at Credit Suisse.

A few weeks ago I found myself sitting in the James Joyce Wine Cellar in Zurich listening to a talk by the Chief Investment Officer of one of the world’s largest asset managers’ fixed income division. Surrounded by ageing wine bottles and Swiss bankers in grey suits, the CIO put down his glass of Chateau Neuf du Pape and proclaimed, “You know, I’ve been investing in fixed income all my career, but I feel obliged to tell you that fixed income as an asset class is dead.” That was the last sentence of the speech.

Now I don’t frequent too many of these events, but ending a presentation on that kind of a bombshell was not something that I’d ever experienced before. The Swiss bankers around me shifted nervously in their seats thinking something else was coming. But the CIO did not follow up the statement with any caveats. He was undoubtedly out to provoke and had we pushed him a little he would have most likely followed up his statement with the usual spiel that one should be careful with statements like ‘this time it is different.’ He would have probably added that fixed income in terms of developed markets sovereign and corporate bonds would at some point in the future again be an interesting investment.

Nonetheless, finding out fixed income was dead was pretty exciting. Moreover, the statement was in line with a trend I had been witnessing for the past couple months whereby capital was flowing into a new asset class – alternative fixed income.

But, before moving on to this, it is worth spending a few minutes on the death of fixed income, whether temporary or not. Classic portfolio management theory will tell you to put 60% of your assets in equities (e.g. at its most basic through a S&P 500 Index ETF) and 40% in bonds (e.g. at its most basic through a Bond Index) in order to achieve diversification and lower the portfolio’s volatility. Without getting too deep into the technicalities, the thinking goes that equities outperform bonds in the long run – hence the overweight. However, bonds are included because they lower the volatility and increase the diversification of the overall portfolio. They lower the volatility because they are less risky than equities. Moreover, bonds have historically moved inversely to equities and this diversification effect has served the purpose of smoothing out the return profile of a balanced portfolio in times of market turbulence. Seeing as, nearly all investors have regular liquidity needs for, for instance, a regular mortgage payment, a smoother albeit lower return profile in the long run is more attractive than high volatility with a higher return in the very long run.

So what has changed? Norman Villamin (CIO Coutts) was recently quoted as saying that bonds used to offer an asymmetric payoff relative to equities whereas now you are left with a “symmetric asset class.” Put another way, bonds still serve the purpose of protecting capital when equities are down but no longer give you any meaningful upside. In other words by having 40% bonds you lower volatility but you no longer achieve diversification. Explaining exactly why, at least from a developed markets perspective, is not straightforward. Some analysts have highlighted that rates have been kept low to encourage lending given the slower than expected recovery in the US and Europe. Other analysts have pointed to lower inflation and central banks not feeling the pressure to increase rates. In any case, with very low returns you also have very low volatility. With low volatility even if this effect moves inversely to equities it will not be ‘strong enough’ to provide the desired counterbalancing effect. Think of two grown men on a seesaw where one gets replaced by a child, no matter how much the child jumps up and down on the plank, they will not significantly propel the man into the air. Whatever the reasons for this phenomenon, most seem to agree that a low rate environment will be the norm for some time to come.

Many investors realize that if rates remain low it will become more difficult to find bonds yielding attractive returns without taking on excessive risk. In terms of fixed income this generally means looking towards emerging market debt or distressed corporate bonds. To be clear some investors have successfully gone down this route, such as, Michael Hasenstab (CIO Franklin Templeton) who has became famous for his bullish speeches on Ukrainian debt. Nonetheless this dynamic has led to many investors leaving fixed income in favor of equities. That trend is clearly reflected by the fact that the largest fund by assets under management has over the last year shifted from the PIMCO Total Return fund (a fixed income product) to the Vanguard Total Stock Market Index (an equity product). The leaving of Mr. Gross from PIMCO no doubt also contributed to this shift.

With the recent prolonged bull market most investors have shut their eyes to the increased volatility and enjoyed the attractive returns they have seen from their portfolios. However, some sophisticated investors have elected not to move their fixed income exposure to equities. Some have chosen to put assets into well-known alternatives like private equity or real estate. But these asset classes do not offer the same advantages that fixed income did.

As outlined above fixed income was liked because, first, it was relatively low risk. Second, it paid a steady regular coupon, which was liked not just by private investors but especially pension and insurance funds, which have regular liquidity needs. Third, it paid a handsome return of anywhere from 5.00% to 8.00% (historically seen). To put that into perspective, a ten year German Government Bond pays you less than 1.00% currently. A private equity or real estate investment conversely can mean having to lock up capital for ten years, with no regular coupon payment, and with no guarantee for handsome reward.

Given this, many of these sophisticated investors have turned to a different asset class that has emerged largely as a product of new lending opportunities. It is often referred to as Alternative Fixed Income. These opportunities have to a large extent emerged as a product of new banking regulations. Simply put, banks have been forced to move away from certain types of lending and new non-bank credit providers have stepped in to fill this void offering new investment opportunities. Indeed, according to Alliance Bernstein, since 1980 the nonfinancial corporate and mortgage credit outstanding has grown by ca. USD 18.9tn whereof USD 15.0tn can be attributed to non-banks.

This trend of lending by non-banks has been accelerated largely as a product of post-crisis regulation. In Europe, the most important regulation framework for this trend has been Basel III. This framework stipulated that banks now have much higher capital requirements as well as having to take on higher operational costs for certain types of lending. This has been most pronounced for investments with longer investments horizons, which therefore cannot match bank-liability structures subject to daily liquidity requirements.

There are literally hundreds of structures that have emerged to take advantage of this systemic shift. The biggest opportunities for alternative credit providers have been in corporate loans, commercial real estate loans, residential real estate loans, and infrastructure loans. Many new organizations have been set up and are raising capital from investors in order to lend to corporations and real estate developers in the same way banks used to. The lenders pay a coupon on the loan, the new firms take a cut, and the investor gets a regular coupon payment at a tolerable risk and a much higher return than they would have in traditional fixed income.

This systemic shift has created opportunities along the entire supply chain of lending. It stretches from the most logical to the most niche areas you can think of, and no doubt this is just the beginning. Below I will give two examples of the most common constellations.

Most commonly you see new organizations made up of former bankers. They leave or are made redundant by their employer. They take with them an intimate knowledge of that bank’s loan book as well as the skillset to analyze other banks’ loan books. They then raise capital in a fund structure (funded by our sophisticated investors above) and begin buying loans from banks that can no longer be kept on their balance sheets. This can take many different forms. The easiest is a pure purchase at a discount where the new organization takes over the loan. Typically this happens via a Collateralized Loan Obligation (CLO) which is a securitized asset backed by a pool of debt. Another variety is a situation where banks have debt on their balance sheet which is highly attractive from a return perspective but which they cannot keep on their balance sheet. They therefore use something called Regulatory Capital Relief Trades (CRTs) in order to temporarily transfer risky assets off their balance sheets to one of these new organizations which in turn charge interest on the assets while on their balance sheets. Finally you have situations where the bank will give an organization access to their pipeline of loan opportunities. This setup is rarer and requires a very close relationship between the bank and the new organization. Essentially, these new organization can sift through bank’s pipeline of lending opportunities and chose to take on any loans they find attractive. In return the bank receives a share of the profits.

The other more common constellation of new organizations is direct loans that banks used to be able to do. Indeed, many of these organizations are whole teams that used to do the same thing at their former employers. A great example is Renshaw Bay. Renshaw Bay was setup by the former co-CEO of J.P. Morgan’s Investment Bank – Bill Winters. The firm runs a real estate strategy that is “focused on direct, whole loan origination of commercial real estate loans… and seeks to take advantage of the lack of financing available to real estate borrowers”. They also run a structural finance strategy, which looks to “capitalize on opportunities driven by regulatory change and the retreat of capital.” There are now new organizations (or old organizations which have seen a significant uptick in demand) that are doing the same thing in corporate loans, real estate loans, infrastructure loans, or even leverage loans to private equity firms.

It is still relatively early days and no one yet completely understands the full implications of this systemic shift. Perhaps the setup is better, seeing as you have more specialized niche players, often with much of their internal capital at risk, and unhindered by bureaucracy associated with banks running these new organizations. Or perhaps this setup is riskier, since at the same time you also have small, inexperienced, and at times highly leveraged organizations with less oversight then banks used to have. Added to this increasing numbers of pension funds and insurance companies are investing in these structures. Undoubtedly there will be some financial cowboys who have cut corners in order to have first mover advantage. At the same time you will undoubtedly have a lot of smart people who will make themselves and their investors a lot of money. Clearly, it is going to be very interesting to monitor these developments to see whether this shift turns out to be a good one or a bad one.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.