This paper studies the spillover of a macroprudential regulation in Spain to the Mexican financial system via Mexican subsidiaries of Spanish banks. The spillover caused a drop in the supply of household credit in Mexico. Municipalities with a higher exposure to Spanish subsidiaries experienced a larger contraction in household credit. These localized contractions caused a drop in macroeconomic activity in the local non-tradable sector. Estimates of the elasticity of loan demand by the non-tradable sector to changes in household credit supply range from 1.2–1.8. These results emphasize cross-border effects of regulations in the presence of global banks.

Key takeaways

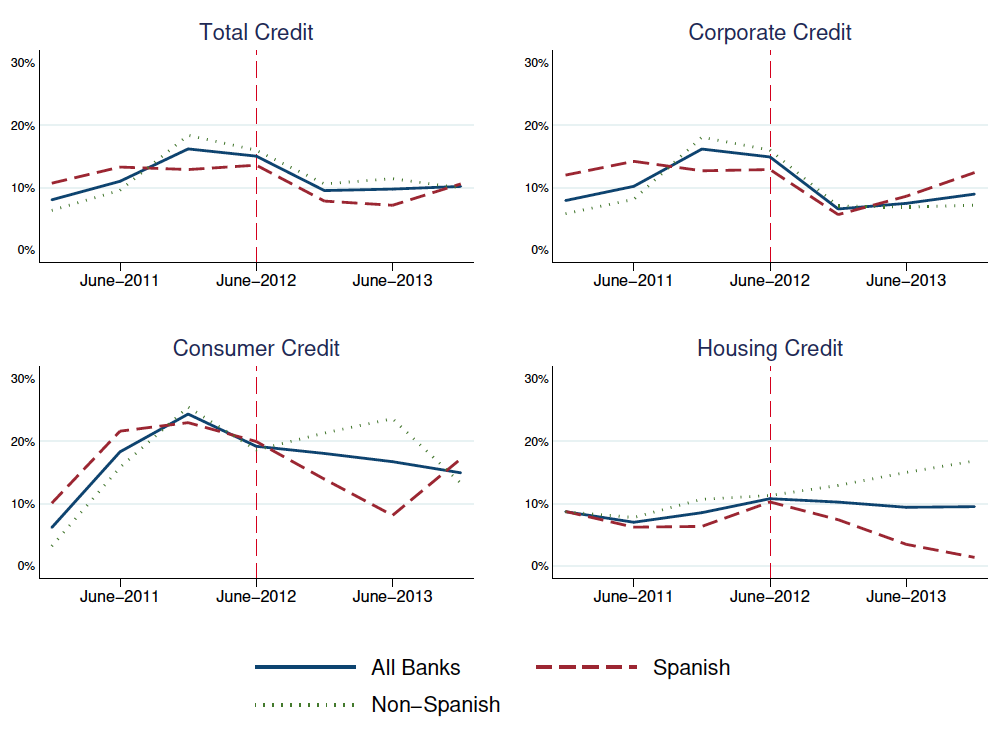

Loan-loss provisions introduced in Spain in 2012 imposed a significant burden on the balanced sheet of Spanish banks. This regulation was unrelated to the Mexican financial system or the credit conditions of Mexican households. However, Mexican subsidiaries of two large Spanish banks, BBVA and Santander, reduced lending to Mexican households in response to the regulation (Fig. 1).

Fig. 1. Growth in credit lending by Spanish and non-Spanish banks in Mexico.

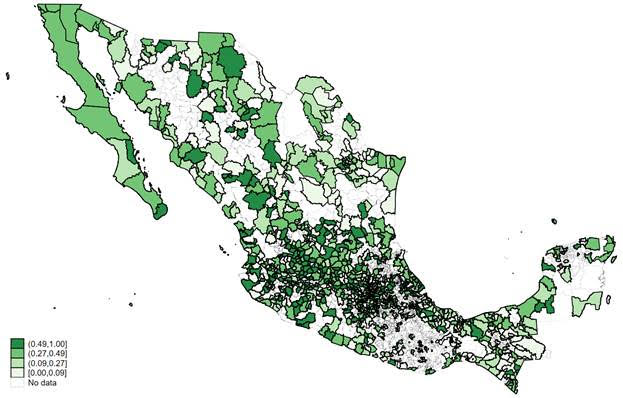

Mexican municipalities with a higher exposure to Spanish banks (Fig. 2) experienced a larger contraction in lending to households. This drop in lending to households (i.e. a drop in credit supply) was associated with a reduction in lending to the local non-tradable sector driven by a drop in local demand. This shows (1) cross-border effects of a macroprudential regulation on lending and economic activity, and (2) the macroeconomic effects of shocks in lending to households in an emerging economy.

Fig. 2. Share of Spanish banks in the household credit market across Mexican municipalities.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Paper abstract

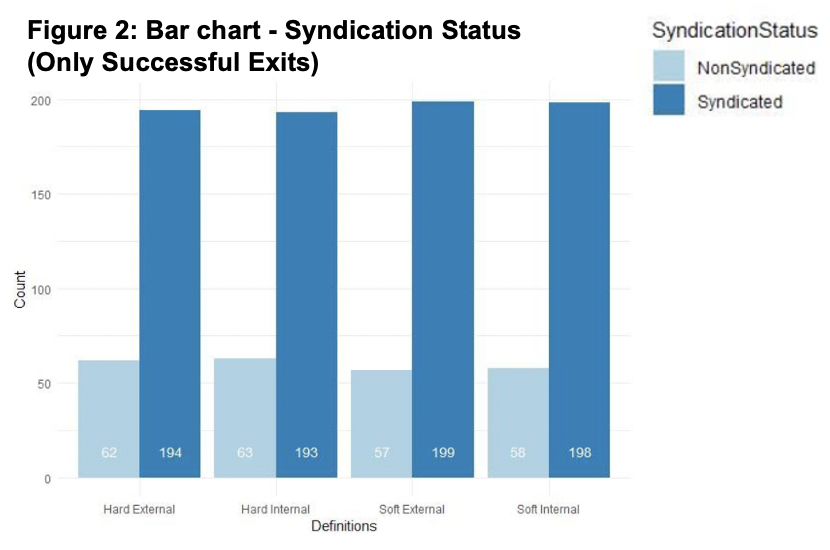

In venture capital, two or more venture capitalists (VC) often form syndicates to participate in the same financing rounds. Historically, syndicated investments have been found to have a positive effect on the investment performance. The paper provides insight into the effects of syndication on the likelihood of a successful exit for the venture-backed firm. It addresses the possible driving components such as the composition of the syndicates and, in particular, the internal investment funds being classed as external firms in two of the four models proposed, as well as a relaxation on the definition of investment round. One of the main conclusions is that in the analysis, using the chance of exiting and money in minus money out as success factors, syndication coefficients across all models are shown to have a higher chance of exiting. This supports the Value-add hypothesis and opposes the alternative, the Selection hypothesis, as it proposes that syndicated VC firms bring varying expertise to the project in order to increase the success factors post-investment. The paper advises to proceed with caution as the story is not consistent across the analysis.

Main conclusions

The paper aimed at looking to add to the literature of debates on reasons for syndication, such as the Valueadd vs Selection hypothesis as set out from various points of views. Uncertainty around profitability is the reason for syndication through the Selection hypothesis, however, the Value-add hypothesis suggests that VCs syndicate to add additional value to the venture post-investment. This is where the varying definitions of syndication we introduced, in order to draw inferences from the data. If the Soft definition of syndication (where syndication can occur across multiple investment rounds), was more successful, it may favour the Value-add hypothesis. However, in the initial test using “exited” as success, the Soft syndication models did not show a significant difference compared to the Hard syndication models.

Using the chance of exiting as a success factor, syndication coefficients across all models showed a higher chance of exiting. Using this as a success factor, you could argue for the Value-add and against the Selection hypothesis, as syndicated investments across all models resulted in a higher chance of exiting the investment. Including the key controls, resulted in similar conclusions to be drawn, with syndication increasing the log odds of exiting. This does support the conclusions of Brander, Amit and Antweiler (2002) that highlight that the Valueadd hypothesis dominates.

Using Money Out minus Money In as a success factor it was shown syndicated investments increased this which would be in line with the Value-add hypothesis according to Brander, Amit and Antweiler (2002), however, this could be down to successful companies being input with greater investments which are already successful.

Using exit duration as a success factor, conclusions were unable to be drawn about syndication, as the syndication coefficients were not significant. A potential reason for this, as the literature suggests, Guo, Lou and Pérez-Castrillo (2015), highlight, that the type of fund the investment is being purchased for has an impact on the duration and amount of funding, therefore impacting the returns of the VCs. They find that CVC (corporate venture capital) backed startups receive a significantly higher investment amount and stay in the market for longer before they exit (Guo, Lou and Pérez-Castrillo, 2015). The data did not allow us to analyse the type of fund, meaning the investment strategy could differ from the outset. As no control variable exists for the type of fund it is therefore assumed this does not significantly impact the outcome. Controlling for the type of fund may have shed light on this aspect of the results.

Can economics be trusted in taking care of the most pressing questions of today in a neutral and un-ideological way? That is the topic of an essay written by Economics alum Pablo Hubacher Haerle ’20 for Chasmotics, an online publishing platform which seeks to question and problematize contemporary times through philosophical thought.

“The Babylonian Marriage Market.” Edwin Long (1875).

Exploring the link between politics and economics

Economics has long been perceived as an unattractively technocratic discipline. Recently, this trend seems to reverse, as economics becomes more popular among young people devoted to change the world for the better. Effective altruists, who seek to do the most good in the most efficient way, recommend that students acquire a PhD in economics, because “you have a high chance of landing an impactful research job” and it is “one of the most promising graduate study options for people who want to make a difference” (Duda 2015).

It is argued that tackling some of today’s pressing political problems such as climate change, income inequality or racism within the economical framework has the advantage of, unlike in less quantitative subjects such as history or sociology, dealing with such political issues with evidence, instead of ideology. But what exactly is the link between politics and economics? How do these two fields interact? And, can economics be trusted in taking care of the most pressing questions of today in a neutral and unideological way?

Looking at the relationship between economic thinking and politics, this essay suggests an answer.

Maximilian and Elliot connected through social media due to the Barcelona GSE connection and started working together on this piece due to shared research interests.

The COVID-19 pandemic is changing the way that we live our lives. As time passes it is becoming apparent that even once the lockdown policies have been eased and some level of normality has been resumed, the new world that we live in will be different to the one we knew before. This article focuses on emerging trends within the UK that have largely taken place as a result of COVID-19, or in some cases the pandemic has simply accelerated a trend that was already occurring. We then look to offer a range of public policy solutions for the recovery period where the overarching objective is to increase wellbeing in society in a sustainable way. These are focused towards the UK but several could be paralleled to other advanced economies.

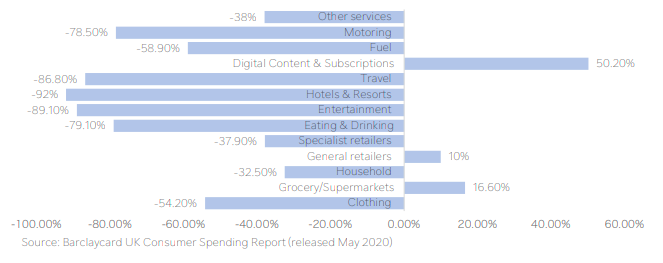

Chart 1. Consumer spending in April 2020 by category, % change year-on-year

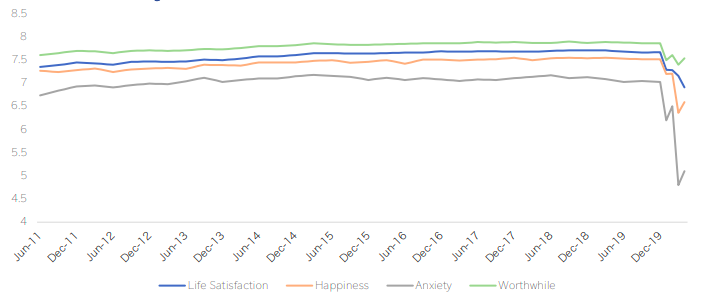

But first, before we get to the policy solutions, briefly, what have been the main economic and wellbeing effects that we have seen as a result of COVID-19? In 2020, it is expected that the fall in overall economic output is going to be larger than during the financial crisis in 2008. Much of this is due to the level of decline in economic activity as a result of the UK governments lockdown policy. This was a necessary decision in order to reduce the spread of the virus and ensure the health service still has capacity to treat those that have unfortunately caught the disease. However, it has led to a significant liquidity shock for both households and businesses. Large portions of the labour market are now out of work and levels of consumer spending have declined rapidly (Chart 1). Alongside sharp falls in measures of economic performance, measures of wellbeing have declined rapidly as well (Chart 2). Increases in measures of uncertainty have mirrored increases in anxiety. While, social distancing policies are having a large impact on measures of happiness.

Chart 2. ONS wellbeing measures (2011-2020)

Source: ONS. Notes: Each of these questions is answered on a scale of 0 to 10, where 0 is “not at all” and 10 is “completely”. Question: “Overall, how satisfied are you with your life nowadays?”, “Overall, to what extent do you feel that the things you do in your life are worthwhile?”, “Overall, how happy did you feel yesterday?”, “Overall, how anxious did you feel yesterday?”.

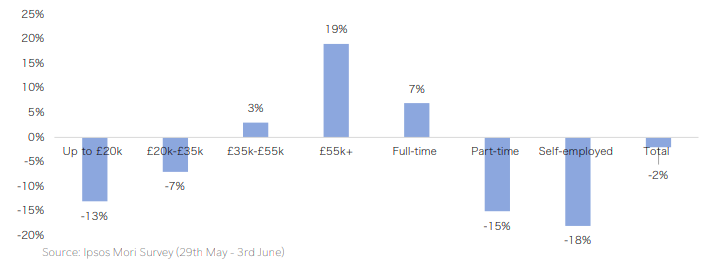

The UK government responded to the shock posed by COVID-19 with a range of policy interventions to provide funding to those that have been most impacted. At a macro level, the long-lasting effects of this crisis will be more pertinent if economic activity does not respond quickly after the government’s schemes have ended. Large portions of UK businesses have limited cash reserves to fall back on in a scenario where demand remains subdued for some time. However, even if the recovery period is strong there will still have been some clear winners and losers during this crisis. Younger workers, those on lower incomes and those with atypical work contracts are the ones that have been most heavily impacted (Chart 3). Whilst those on higher incomes, that are more likely to be able to work from home, have increased their household savings during this period, due to less opportunities to consume.

Chart 3. Impact of COVID-19 on household savings by income and employment type

The policy solutions outlined below aim to be complementary of one another and look to amplify observed trends that are positive for wellbeing and to provide intervention where trends have been negative for wellbeing:

Climate at the centre of the response: This is less a policy recommendation and more a theme for the response. However, our message here is that increased public spending projects, focused towards green initiatives should be combined with a coherent carbon tax policy which influences incentives and helps to support the UK’s transition to a low carbon economy.

Labour market reforms: The government should look to develop a centralised job retraining and job matching scheme that supports workers most impacted by COVID-19, helps to encourage structural transformation towards emerging industries and increases the amount of highly skilled workers in the UK workforce.

Tough decisions on business: Some businesses will require further assistance from the UK government in the form of equity funding, rather than the debt funding seen so far. This should be done on a conditional basis, requiring all these businesses to comply with the UK’s climate objectives and should only be provided to businesses in industries that are expanding or strategically important to the UK economy.

Modernising the regions on a cleaner, greener and higher level: Looking to build on the governments ‘levelling up the regions’ policy to reduce regional inequalities, our policy consists of government funded infrastructure policies that include green investments for regions outside of the UK’s capital.

Harbouring that rainbow effect: Building on the increased community spirit that has been observed during the pandemic, this policy solution looks to increase localised community funding to maintain social cohesion and support those with mental health issues.

Lastly, as the policy recommendations focus on expanding public investment to support the recovery, it is important to consider what this means for public debt sustainability in the UK. The conclusion is that as a result of the low interest rate environment, the most efficient way out of this recession is to borrow and spend on projects that will increase resilience to future shocks and support the UK’s transition to a low carbon economy.

Please click on the link below to read about this in more detail. Comments are welcome.

We investigate unemployment due to mismatch in the United States over the past three and a half decades. We propose an accounting framework that allows us to estimate the contribution of each of the frictions that generated labor market mismatch. Barriers to job mobility account for the largest part of mismatch unemployment, with a smaller role for barriers to worker mobility. We find little contribution of wage-setting frictions to mismatch.

VoxEU article by Adilzhan Ismailov ’15 (Economics) and Professor Antonio Ciccone

CEPR’s policy portal VoxEU has published the article “Democratic tipping points” by Economics alum Adilzhan Ismailov ’15 and Antonio Ciccone, professor at the Barcelona GSE and the UPF Economics department, where Adilzhan is currently doing his PhD.

VoxEU promotes “research-based policy analysis and commentary by leading economists.” The site receives about a half million page views per month.

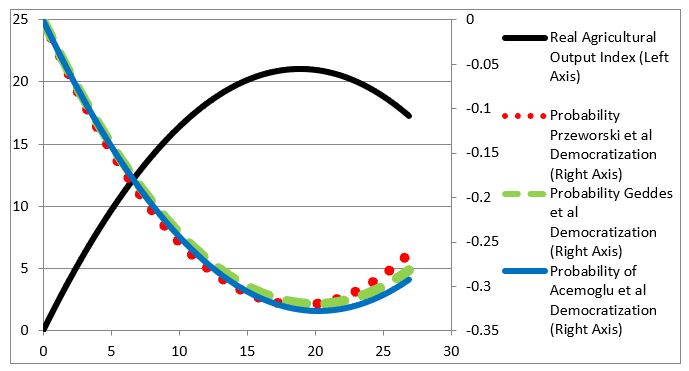

Persistence of democratisation following transitory economic shocks plays an important role in the theory of political institutions. This column tests the theory of democratic tipping points using rainfall shocks in the world’s most agricultural countries since 1946. Negative rainfall shocks have a strong and transitory effect on agricultural output, but a persistent positive effect on the probability of democratisation even after ten years.

Key conclusions

The recent history of democratic (non-)transitions in the world’s most agricultural countries indicates that transitory events can have enduring effects on democratic institutions. When lower rainfall led to below-average agricultural output in these countries, countries ruled by authoritarian regimes were more likely to democratise and more likely to be democratic ten years later.

The shape of the effect of rainfall on the probability of democratisation indicates that the effect is through agricultural output. The agricultural economics literature finds an inverted-U-shaped effect of rainfall on agricultural output. In the theory of Acemoglu and Robinson (2001, 2006) we build on, transitorily lower output raises the probability of democratisation, and transitorily higher output lowers the probability of democratisation. Hence, the inverted-U-shaped effect of rainfall on agricultural output should translate into a U-shaped effect of rainfall on the probability of democratisation. We find this to be the case. Moreover, our results indicate that rainfall shocks tend to produce the largest change in the probability of democratisation when the estimated effect of rainfall on agricultural output is largest.

Figure. Effect of rainfall on real agricultural output and on the probability of democratisation

Note: The inverted-U-shaped solid black line is the effect of rainfall in year t on real agricultural output in year t and is measured on the left axis. The U-shaped coloured lines are the effect of rainfall on the probability of democratisation between years t-1 and t (one year later). The three classifications of democratic and autocratic regimes used in the figure are those of Acemoglu et al. (2019) (blue solid line); Przeworski et al. (2000) (red dotted line), as updated by Cheibub et al. (2010) and Bjornskov and Rode (2020); and Geddes et al. (2014) (green dashed line). The effect of rainfall on the probability of democratisation is calculated using the effect of rainfall in year t in column (1) of Tables 2 and 3 in the paper respectively for the Acemoglu et al. and the Przeworski et al. democratisation indicator. For the Geddes et al. democratisation indicator, the effect of rainfall on the probability of democratisation is calculated using the effect of rainfall in year t-1 in column (5) of Table 3. This is because of Geddes et al.’s unconventional start date for democratic regime transitions; see page 16 for details. Real agricultural output is an index with the base period 2004-2006. Rainfall is measured in dm.

Her research on the topic was also featured in The Washington Post last year!

Paper abstract

Do forced assimilation policies always succeed in integrating immigrant groups? This paper examines how a specific assimilation policy – language restrictions in elementary school – affects integration and identification with the host country later in life. After World War I, several US states barred the German language from their schools. Affected individuals were less likely to volunteer in WWII and more likely to marry within their ethnic group and to choose decidedly German names for their offspring. Rather than facilitating the assimilation of immigrant children, the policy instigated a backlash, heightening the sense of cultural identity among the minority.

BIS Bulletin by Sebastian Doerr ’13 (Economics) and Leonardo Gambacorta

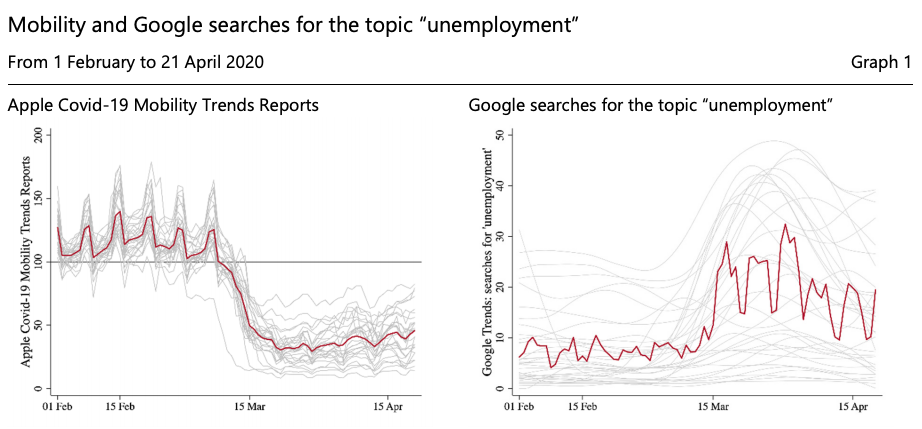

The outbreak of Covid-19 and the ensuing measures to contain the pandemic have brought Europe into a deep downturn. GDP is expected to drop by around 8% in the euro area this year (ECB (2020)), a significantly steeper decline than forecasted for the United States or Asia (IMF (2020)). One of the major reasons why the European economy is expected to be so hard-hit is its high share of small firms, especially in southern and eastern European countries. Small firms are financially more constrained and bank-dependent than larger firms. They also sell goods predominantly in local markets and with less diversified sources of revenue.

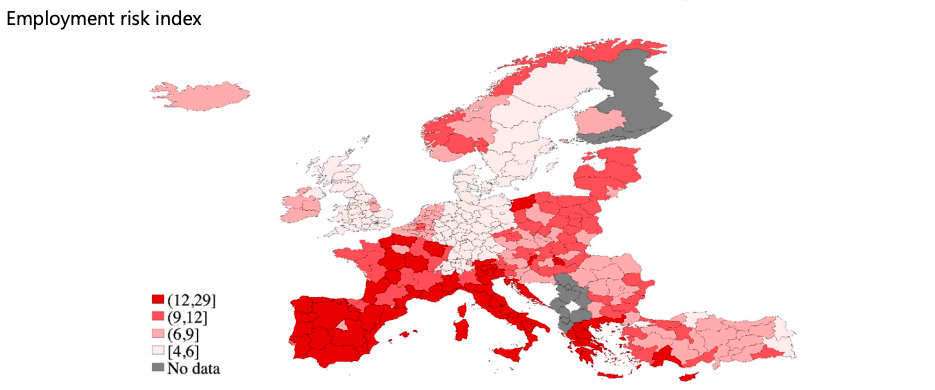

This Bulletin investigates which European regions face higher risks to employment from Covid-19. We first use data on local industry-level employment before the outbreak and construct a measure of local employment exposure to Covid-19, using the methodology developed in Doerr and Gambacorta (2020) for the US. We then extend the analysis by taking into account the share of employment among small firms in different regions. Specifically, we calculate an employment risk index based on the interaction of sectoral exposure and the share of small business employment. Our results show that while several European regions employ a high share of people in sectors particularly exposed to the economic consequences of the pandemic, the high share of small firms in southern Europe puts employment in those regions particularly at risk. We show that regions with a higher employment risk index, ie those with higher sectoral exposure and a higher share of small businesses, also exhibit a stronger increase in Google searches for unemployment, providing a cross-check of our measure of local employment risk.

The left-hand panel shows the evolution of Apple Covid-19 Mobility Trends Reports from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). The index is averaged across all subcategories. The Mobility Trends index reflects requests for directions in Apple Maps and is standardised to 100 on 13 January 2020. The right-hand panel shows the relative frequency of Google searches for the topic “unemployment” from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). For illustration, country-specific lines are Hodrick Prescott-filtered trend components with a smoothing parameter of 500.

Sources: Apple Covid-19 Mobility Trends Reports; Google Trends; authors’ calculations.

Key takeaways

We construct employment risk indices for European regions that reflect the share of jobs under threat from Covid-19. The risk index is based on local employment in sectors that are more exposed to the pandemic and on the regional incidence of small firms.

Employment in regions in southern Europe and France is shown to have high risk indices, while regions in northern Europe have lower risk indices. Eastern and central European regions have intermediate risk indices.

Regions with a higher risk index have a bigger jump in Google searches for unemployment-related terms.

The challenge for the EU is to deliver a policy response that reduces, not exacerbates differences. This requires a level playing field (e.g. for state aids) and a high degree of coordination.

Help Economics alum Steffi Huber ’10 by participating this survey!

I’d like to invite Barcelona GSE students and alumni to participate in a survey I’m conducting with Isabelle Salle (Bank of Canada, research fellow at the University of Amsterdam) to help understanding households’ consumption and investment responses to the prolonged “dance” phase of the COVID-19 crisis.

As yet, policymakers and academics do not have good estimates for how people might behave in this crucial period. You can help to fill this gap, and in the process help to build a collective understanding of the economic consequences of the pre-vaccine crisis.

We’ve received around 1,000 responses to the survey so far, and we are using it as a trial survey which will be adjusted for a large grant application to run a representative survey in all major European countries.

Please read below to know more about what is involved.

Purpose of the research

This research survey aims to shed light on household responses to the COVID-crisis in two ways. First, we want to investigate how the crisis has already changed investment and consumption demands. Second, we want to understand the expected consumption and investment behavior of households when lockdown restrictions are progressively lifted but prior to an effective treatment or vaccine being available.

What taking part involves

There will be a series of questions about your current and planned consumption and investments. The survey requires no special knowledge for you to complete it. Your participation is voluntary, you do not have to answer all the questions if you do not want to, and you may withdraw from the study at any point.

Your data

The information provided by you in the survey will be held anonymously, so it will be impossible to trace this information back to you individually. The anonymous data itself will be held indefinitely and may be used to produce reports, presentations, and academic publications. If you have any questions or concerns about this research please feel free to contact any of the researchers involved in the project, using the contact details below.

The survey can be answered in 16 different languages. So, don’t hesitate to forward this email to all your international friends!

See this website for more info on the objectives of this project.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

In my all-time favourite book ‘Antifragile’, Nassim Taleb divides the world into 3 categories- fragile, robust and antifragile. He refers to fragility as the state of being that involves avoiding disorder and disruption for fear of the mess that threatens to disrupt your life: you think you are keeping safe, but really you are making yourself vulnerable to the shock that will tear everything apart. Robustness is the ability to stand up to shocks without flinching, without changing who you are. But you are antifragile if shocks make you better able to adapt to each new challenge you face. You are antifragile if you can opportune from disruptions, to be stronger and more creative. Taleb thinks we should all try to be antifragile!

On March 11, 2020, declared a world pandemic, the COVID-19, is an epitome of the chaotic disruption Taleb was referring to. The onset of this crisis got me pondering whether populations, institutions, financial bodies, governments and policy-makers -i.e. the world as a whole will be able to be resilient in the face of the aftermath of this crisis? Do we have the acceptance, courage and strength besides the technical, innovative and problem-solving skills to start afresh and turn this disequilibrium around into the most memorable salvation story we have ever seen? Or will we succumb to this dooming, seemingly apocalyptic spiral, and lose everything we take for granted in our day-to-day lives? When the noise of this unprecedented shock dies, will we be left at the inception of a brand new system that will push us to rethink policies, and rewrite mandates that shape, govern and structure the world?

The outbreak of this global health crisis saw a strong backlash against globalization in the form of acceleration of trends underway. Before COVID-19 slammed the global economy earlier this year, China had adopted selective international exchange rates for political incentives. This had consequently led to US-China trade wars involving up to 25% tariff imposition on Chinese imports.

In March, COVID-19 contributed to this backdrop by declining the number of cargo ships setting off for the United States by 10%. The cost of shipping goods by air nearly doubled, restricting trade further. In order to contain the outbreak of the rapidly spreading virus, countries were forced to close their borders to foreign visitors which severely restricted the movement of people worldwide.

With no signs of the situation returning to normalcy, countries are desperately trying to be “self-sufficient” by ordering factories at home to produce ventilators, banning exports of face masks, and localizing pharmaceutical supply chains even at the cost of added expenses. The declaration of a potential suspension of immigration into the U.S by the President seemed like a final nail in the coffin for the era of globalization.

The world’s response to COVID comes across as ratifying Trump’s argument for protectionism and supply chain controls. This alludes to a pressing question in such uncertain times: Will the world remain flat after the curve flattens after all? Let’s first look at what does it mean for the “world to be flat”? In the book, ‘The world is flat’ by Thomas L. Friedman, the author endorses his view of the world as a level-playing field, wherein all players have equal opportunity and the world is a global market where historical and geographic boundaries are becoming increasingly irrelevant.

Globalization has persisted in different forms for decades. In my opinion, just like the dotcom bubble, 9/11 debacle, 2008 financial crisis, the COVID-19 pandemic too, is a temporary shock, which will perhaps change the face of globalization but not sink it. In the near future, we will likely either have a vaccine or much of the world will be infected by the virus. Either way, the current restrictions will neither be needed nor sustainable in the long run.

For instance, by the time the curve peaks, most countries will perhaps already have bought or produced enough inventory. In that case, will it really make sense to use tax-payers money on incurring exorbitant production costs to set up ventilator factories at home when their supply is already bolstered by sufficient purchase? Evidently, medical supply chains will change less than politicians currently promise!

But even after the shock evanesces, COVID-19 will heavily influence the decision-making process with regards to investment and relocation. Many argue that the crisis was an exemplary demonstration of increased risks associated with globalised supply-chains. A flip-side to the dispute is that in the quest to maximize profits and reduce the risk of localized disruption from the crisis, if anything, firms might only expand production lines across the world, creating employment more evenly, and promoting eventual global recovery. In fact, the renowned economist, Obstfeld, who served as IMF’s chief from late 2015 through 2018, said that “While global supply chains will undoubtedly change in a post-crisis economy, much of that change will be in the form of diversification, not on-shoring.”

While layoffs and increasing unemployment in a post-crisis recessive economy are inevitable, they will not mark the end of outsourcing. Turning to autarky-like economies will be too costly to be sustainable for countries world-over. There will be plenty of opportunities to employ people in jobs that demand highly skilled labour to meet the needs of the recovering economies. This will pave the way for Globalisation 3.0, described in Friedman’s book as individuals focusing on finding their foothold in the present global competition and making significant global collaborations. In fact, skill up-gradation of this form, to ensure relevance as demanded by the need of the hour, will push humans towards becoming antifragile, as recommended by Taleb.

However, “Outsourcing is just one dimension of a much more fundamental thing happening today in the world”, Friedman claims. Experts often view globalization from a one-dimensional perspective- physical goods and services crossing borders. But in fact, many intangibles- data, value, ideas, innovation frequently cross borders. In his book, Friedman emphasizes that “You don’t need to emigrate to innovate”. “Globalization in recent times has created a platform where intellectual work, intellectual capital, can be delivered from anywhere. It could be disaggregated, delivered, distributed, produced and put back together again — and this gave a whole new degree of freedom to the way work is done, especially work of an intellectual nature.” In light of this view of global integration, I believe that the world is going to get flatter. With workforces across nations getting training on Zoom video conferencing, to extensive sharing of knowledge in research on medical advances, the spillover of ideas and innovation is going to witness only an onward spur. The quantity and value of data transmitting between countries are increasing and with the high-value data processing replacing supply chains as the predominant channel of global economic exchange, I see this only increasing further.

So is the world after coronavirus tending to globalization or deglobalization? I think it depends on where you look. COVID can make it harder to ship Chelsea fan-club merchandise around the world, but no quarantine can contain cryptos from crossing borders!

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.