This paper studies the spillover of a macroprudential regulation in Spain to the Mexican financial system via Mexican subsidiaries of Spanish banks. The spillover caused a drop in the supply of household credit in Mexico. Municipalities with a higher exposure to Spanish subsidiaries experienced a larger contraction in household credit. These localized contractions caused a drop in macroeconomic activity in the local non-tradable sector. Estimates of the elasticity of loan demand by the non-tradable sector to changes in household credit supply range from 1.2–1.8. These results emphasize cross-border effects of regulations in the presence of global banks.

Key takeaways

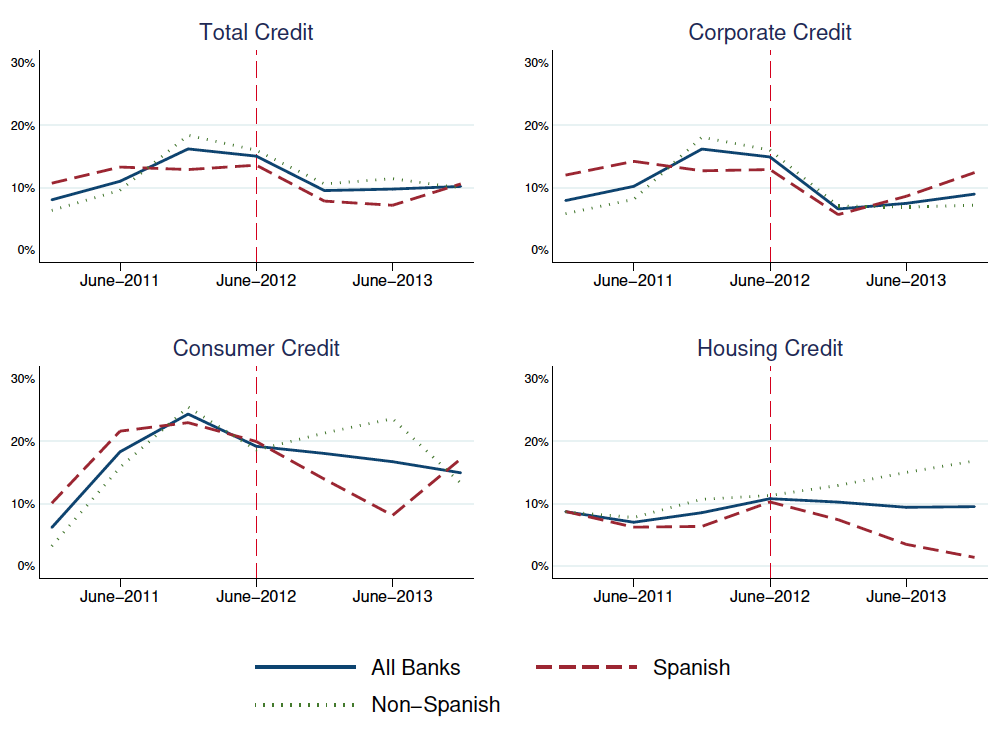

Loan-loss provisions introduced in Spain in 2012 imposed a significant burden on the balanced sheet of Spanish banks. This regulation was unrelated to the Mexican financial system or the credit conditions of Mexican households. However, Mexican subsidiaries of two large Spanish banks, BBVA and Santander, reduced lending to Mexican households in response to the regulation (Fig. 1).

Fig. 1. Growth in credit lending by Spanish and non-Spanish banks in Mexico.

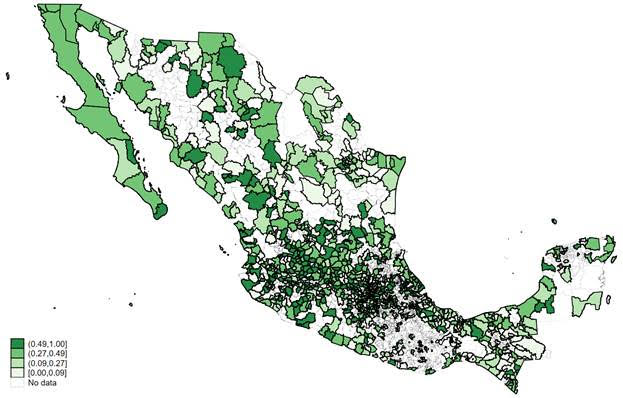

Mexican municipalities with a higher exposure to Spanish banks (Fig. 2) experienced a larger contraction in lending to households. This drop in lending to households (i.e. a drop in credit supply) was associated with a reduction in lending to the local non-tradable sector driven by a drop in local demand. This shows (1) cross-border effects of a macroprudential regulation on lending and economic activity, and (2) the macroeconomic effects of shocks in lending to households in an emerging economy.

Fig. 2. Share of Spanish banks in the household credit market across Mexican municipalities.

Maximilian and Elliot connected through social media due to the Barcelona GSE connection and started working together on this piece due to shared research interests.

The COVID-19 pandemic is changing the way that we live our lives. As time passes it is becoming apparent that even once the lockdown policies have been eased and some level of normality has been resumed, the new world that we live in will be different to the one we knew before. This article focuses on emerging trends within the UK that have largely taken place as a result of COVID-19, or in some cases the pandemic has simply accelerated a trend that was already occurring. We then look to offer a range of public policy solutions for the recovery period where the overarching objective is to increase wellbeing in society in a sustainable way. These are focused towards the UK but several could be paralleled to other advanced economies.

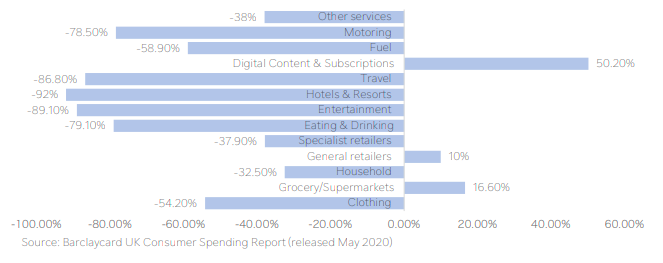

Chart 1. Consumer spending in April 2020 by category, % change year-on-year

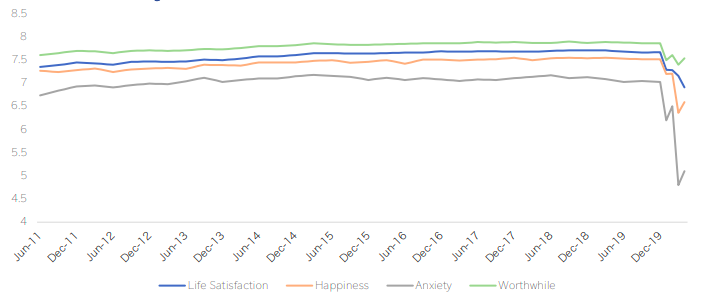

But first, before we get to the policy solutions, briefly, what have been the main economic and wellbeing effects that we have seen as a result of COVID-19? In 2020, it is expected that the fall in overall economic output is going to be larger than during the financial crisis in 2008. Much of this is due to the level of decline in economic activity as a result of the UK governments lockdown policy. This was a necessary decision in order to reduce the spread of the virus and ensure the health service still has capacity to treat those that have unfortunately caught the disease. However, it has led to a significant liquidity shock for both households and businesses. Large portions of the labour market are now out of work and levels of consumer spending have declined rapidly (Chart 1). Alongside sharp falls in measures of economic performance, measures of wellbeing have declined rapidly as well (Chart 2). Increases in measures of uncertainty have mirrored increases in anxiety. While, social distancing policies are having a large impact on measures of happiness.

Chart 2. ONS wellbeing measures (2011-2020)

Source: ONS. Notes: Each of these questions is answered on a scale of 0 to 10, where 0 is “not at all” and 10 is “completely”. Question: “Overall, how satisfied are you with your life nowadays?”, “Overall, to what extent do you feel that the things you do in your life are worthwhile?”, “Overall, how happy did you feel yesterday?”, “Overall, how anxious did you feel yesterday?”.

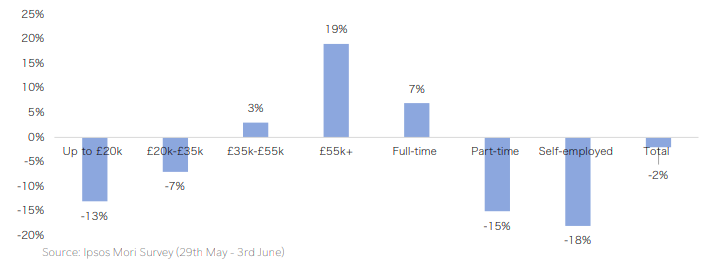

The UK government responded to the shock posed by COVID-19 with a range of policy interventions to provide funding to those that have been most impacted. At a macro level, the long-lasting effects of this crisis will be more pertinent if economic activity does not respond quickly after the government’s schemes have ended. Large portions of UK businesses have limited cash reserves to fall back on in a scenario where demand remains subdued for some time. However, even if the recovery period is strong there will still have been some clear winners and losers during this crisis. Younger workers, those on lower incomes and those with atypical work contracts are the ones that have been most heavily impacted (Chart 3). Whilst those on higher incomes, that are more likely to be able to work from home, have increased their household savings during this period, due to less opportunities to consume.

Chart 3. Impact of COVID-19 on household savings by income and employment type

The policy solutions outlined below aim to be complementary of one another and look to amplify observed trends that are positive for wellbeing and to provide intervention where trends have been negative for wellbeing:

Climate at the centre of the response: This is less a policy recommendation and more a theme for the response. However, our message here is that increased public spending projects, focused towards green initiatives should be combined with a coherent carbon tax policy which influences incentives and helps to support the UK’s transition to a low carbon economy.

Labour market reforms: The government should look to develop a centralised job retraining and job matching scheme that supports workers most impacted by COVID-19, helps to encourage structural transformation towards emerging industries and increases the amount of highly skilled workers in the UK workforce.

Tough decisions on business: Some businesses will require further assistance from the UK government in the form of equity funding, rather than the debt funding seen so far. This should be done on a conditional basis, requiring all these businesses to comply with the UK’s climate objectives and should only be provided to businesses in industries that are expanding or strategically important to the UK economy.

Modernising the regions on a cleaner, greener and higher level: Looking to build on the governments ‘levelling up the regions’ policy to reduce regional inequalities, our policy consists of government funded infrastructure policies that include green investments for regions outside of the UK’s capital.

Harbouring that rainbow effect: Building on the increased community spirit that has been observed during the pandemic, this policy solution looks to increase localised community funding to maintain social cohesion and support those with mental health issues.

Lastly, as the policy recommendations focus on expanding public investment to support the recovery, it is important to consider what this means for public debt sustainability in the UK. The conclusion is that as a result of the low interest rate environment, the most efficient way out of this recession is to borrow and spend on projects that will increase resilience to future shocks and support the UK’s transition to a low carbon economy.

Please click on the link below to read about this in more detail. Comments are welcome.

We investigate unemployment due to mismatch in the United States over the past three and a half decades. We propose an accounting framework that allows us to estimate the contribution of each of the frictions that generated labor market mismatch. Barriers to job mobility account for the largest part of mismatch unemployment, with a smaller role for barriers to worker mobility. We find little contribution of wage-setting frictions to mismatch.

VoxEU article by Adilzhan Ismailov ’15 (Economics) and Professor Antonio Ciccone

CEPR’s policy portal VoxEU has published the article “Democratic tipping points” by Economics alum Adilzhan Ismailov ’15 and Antonio Ciccone, professor at the Barcelona GSE and the UPF Economics department, where Adilzhan is currently doing his PhD.

VoxEU promotes “research-based policy analysis and commentary by leading economists.” The site receives about a half million page views per month.

Persistence of democratisation following transitory economic shocks plays an important role in the theory of political institutions. This column tests the theory of democratic tipping points using rainfall shocks in the world’s most agricultural countries since 1946. Negative rainfall shocks have a strong and transitory effect on agricultural output, but a persistent positive effect on the probability of democratisation even after ten years.

Key conclusions

The recent history of democratic (non-)transitions in the world’s most agricultural countries indicates that transitory events can have enduring effects on democratic institutions. When lower rainfall led to below-average agricultural output in these countries, countries ruled by authoritarian regimes were more likely to democratise and more likely to be democratic ten years later.

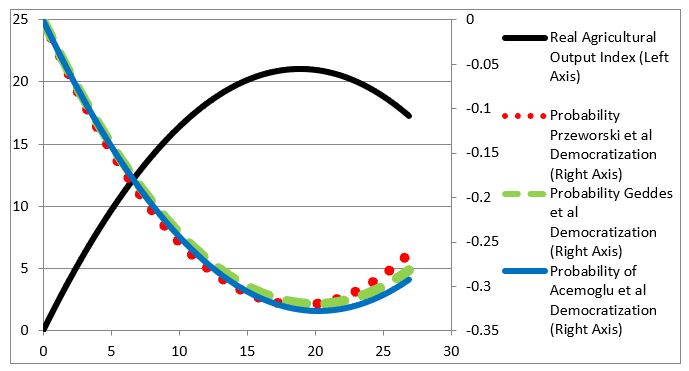

The shape of the effect of rainfall on the probability of democratisation indicates that the effect is through agricultural output. The agricultural economics literature finds an inverted-U-shaped effect of rainfall on agricultural output. In the theory of Acemoglu and Robinson (2001, 2006) we build on, transitorily lower output raises the probability of democratisation, and transitorily higher output lowers the probability of democratisation. Hence, the inverted-U-shaped effect of rainfall on agricultural output should translate into a U-shaped effect of rainfall on the probability of democratisation. We find this to be the case. Moreover, our results indicate that rainfall shocks tend to produce the largest change in the probability of democratisation when the estimated effect of rainfall on agricultural output is largest.

Figure. Effect of rainfall on real agricultural output and on the probability of democratisation

Note: The inverted-U-shaped solid black line is the effect of rainfall in year t on real agricultural output in year t and is measured on the left axis. The U-shaped coloured lines are the effect of rainfall on the probability of democratisation between years t-1 and t (one year later). The three classifications of democratic and autocratic regimes used in the figure are those of Acemoglu et al. (2019) (blue solid line); Przeworski et al. (2000) (red dotted line), as updated by Cheibub et al. (2010) and Bjornskov and Rode (2020); and Geddes et al. (2014) (green dashed line). The effect of rainfall on the probability of democratisation is calculated using the effect of rainfall in year t in column (1) of Tables 2 and 3 in the paper respectively for the Acemoglu et al. and the Przeworski et al. democratisation indicator. For the Geddes et al. democratisation indicator, the effect of rainfall on the probability of democratisation is calculated using the effect of rainfall in year t-1 in column (5) of Table 3. This is because of Geddes et al.’s unconventional start date for democratic regime transitions; see page 16 for details. Real agricultural output is an index with the base period 2004-2006. Rainfall is measured in dm.

Her research on the topic was also featured in The Washington Post last year!

Paper abstract

Do forced assimilation policies always succeed in integrating immigrant groups? This paper examines how a specific assimilation policy – language restrictions in elementary school – affects integration and identification with the host country later in life. After World War I, several US states barred the German language from their schools. Affected individuals were less likely to volunteer in WWII and more likely to marry within their ethnic group and to choose decidedly German names for their offspring. Rather than facilitating the assimilation of immigrant children, the policy instigated a backlash, heightening the sense of cultural identity among the minority.

BIS Bulletin by Sebastian Doerr ’13 (Economics) and Leonardo Gambacorta

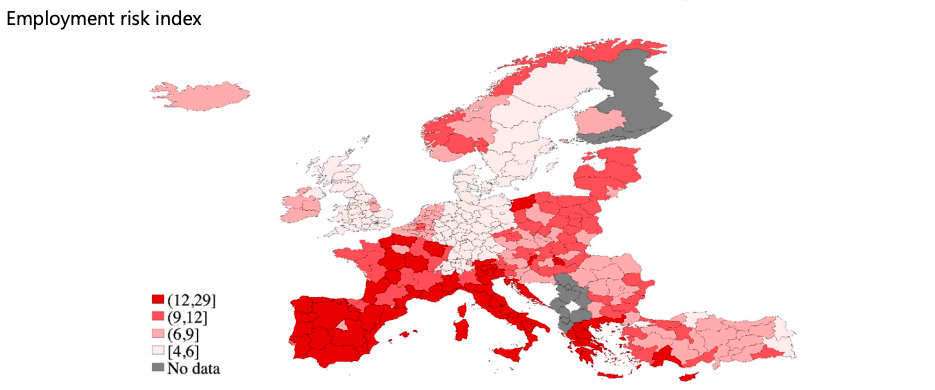

The outbreak of Covid-19 and the ensuing measures to contain the pandemic have brought Europe into a deep downturn. GDP is expected to drop by around 8% in the euro area this year (ECB (2020)), a significantly steeper decline than forecasted for the United States or Asia (IMF (2020)). One of the major reasons why the European economy is expected to be so hard-hit is its high share of small firms, especially in southern and eastern European countries. Small firms are financially more constrained and bank-dependent than larger firms. They also sell goods predominantly in local markets and with less diversified sources of revenue.

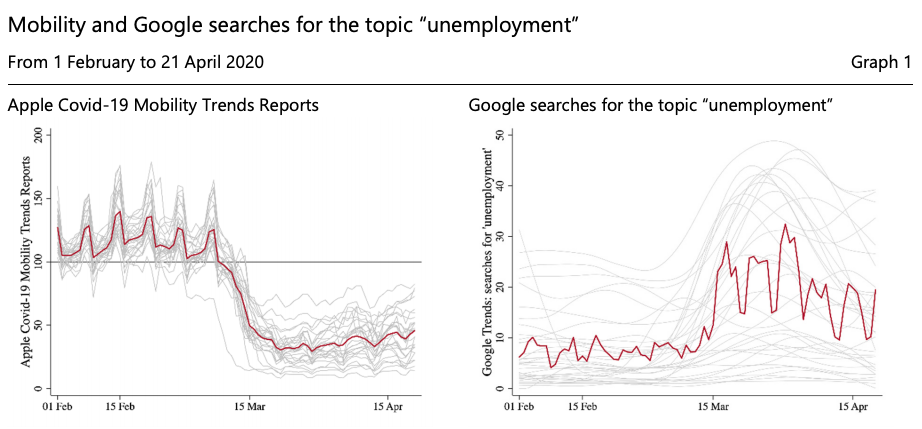

This Bulletin investigates which European regions face higher risks to employment from Covid-19. We first use data on local industry-level employment before the outbreak and construct a measure of local employment exposure to Covid-19, using the methodology developed in Doerr and Gambacorta (2020) for the US. We then extend the analysis by taking into account the share of employment among small firms in different regions. Specifically, we calculate an employment risk index based on the interaction of sectoral exposure and the share of small business employment. Our results show that while several European regions employ a high share of people in sectors particularly exposed to the economic consequences of the pandemic, the high share of small firms in southern Europe puts employment in those regions particularly at risk. We show that regions with a higher employment risk index, ie those with higher sectoral exposure and a higher share of small businesses, also exhibit a stronger increase in Google searches for unemployment, providing a cross-check of our measure of local employment risk.

The left-hand panel shows the evolution of Apple Covid-19 Mobility Trends Reports from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). The index is averaged across all subcategories. The Mobility Trends index reflects requests for directions in Apple Maps and is standardised to 100 on 13 January 2020. The right-hand panel shows the relative frequency of Google searches for the topic “unemployment” from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). For illustration, country-specific lines are Hodrick Prescott-filtered trend components with a smoothing parameter of 500.

Sources: Apple Covid-19 Mobility Trends Reports; Google Trends; authors’ calculations.

Key takeaways

We construct employment risk indices for European regions that reflect the share of jobs under threat from Covid-19. The risk index is based on local employment in sectors that are more exposed to the pandemic and on the regional incidence of small firms.

Employment in regions in southern Europe and France is shown to have high risk indices, while regions in northern Europe have lower risk indices. Eastern and central European regions have intermediate risk indices.

Regions with a higher risk index have a bigger jump in Google searches for unemployment-related terms.

The challenge for the EU is to deliver a policy response that reduces, not exacerbates differences. This requires a level playing field (e.g. for state aids) and a high degree of coordination.

Help Economics alum Steffi Huber ’10 by participating this survey!

I’d like to invite Barcelona GSE students and alumni to participate in a survey I’m conducting with Isabelle Salle (Bank of Canada, research fellow at the University of Amsterdam) to help understanding households’ consumption and investment responses to the prolonged “dance” phase of the COVID-19 crisis.

As yet, policymakers and academics do not have good estimates for how people might behave in this crucial period. You can help to fill this gap, and in the process help to build a collective understanding of the economic consequences of the pre-vaccine crisis.

We’ve received around 1,000 responses to the survey so far, and we are using it as a trial survey which will be adjusted for a large grant application to run a representative survey in all major European countries.

Please read below to know more about what is involved.

Purpose of the research

This research survey aims to shed light on household responses to the COVID-crisis in two ways. First, we want to investigate how the crisis has already changed investment and consumption demands. Second, we want to understand the expected consumption and investment behavior of households when lockdown restrictions are progressively lifted but prior to an effective treatment or vaccine being available.

What taking part involves

There will be a series of questions about your current and planned consumption and investments. The survey requires no special knowledge for you to complete it. Your participation is voluntary, you do not have to answer all the questions if you do not want to, and you may withdraw from the study at any point.

Your data

The information provided by you in the survey will be held anonymously, so it will be impossible to trace this information back to you individually. The anonymous data itself will be held indefinitely and may be used to produce reports, presentations, and academic publications. If you have any questions or concerns about this research please feel free to contact any of the researchers involved in the project, using the contact details below.

The survey can be answered in 16 different languages. So, don’t hesitate to forward this email to all your international friends!

See this website for more info on the objectives of this project.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

ADBI Working Paper by Finance ’18 alumni Lavinia Franco, Ana Laura García, Vigor Husetović, and Jes Lassiter

A master project by four alumni of the Finance Program Class of 2018 is soon to be added to the working paper series of the Asian Development Bank Institute (ADBI).

Abstract

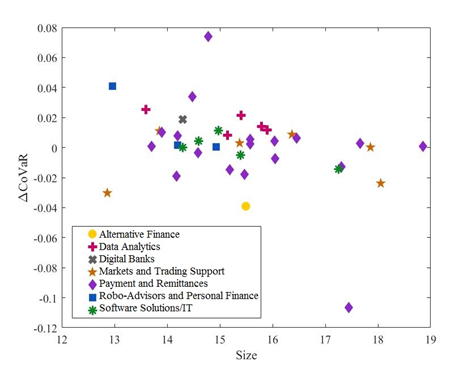

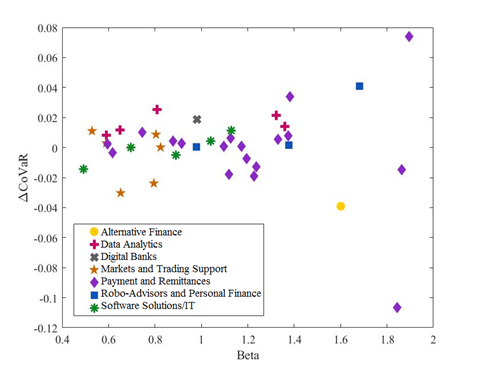

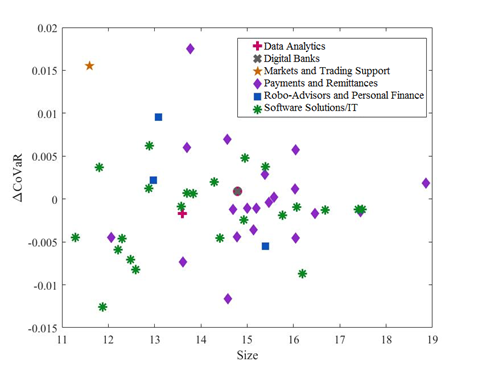

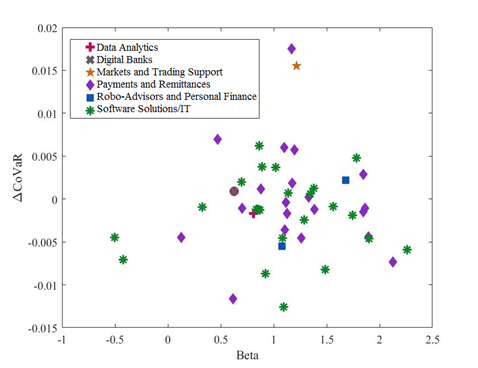

Fintech has increasingly become part of the global economy with the evolution of technology, increasing investments in fintech firms, and greater integration between traditional incumbent financial firms and fintech. Since the 2007–2009 financial crisis, research has also paid more attention to systemic risk and the impact of financial institutions on systemic risk. As fintech grows, so too should the concern about its possible impact on systemic risk. This paper analyzes two indices of public fintech firms (one for the United States and another for Europe) by computing the ∆CoVaR of the fintech firms against the financial system to measure their impact on systemic risk. Our results show that at this time fintech firms do not contribute greatly to systemic risk.

Figure B.2: US Fintech: ∆CoVaR and Size

Figure B.3: US Fintech: ∆CoVaR and Beta

Figure B.4: European Fintech: ∆CoVaR and Size

Figure B.5: European Fintech: ∆CoVaR and Beta

Conclusions and key results

Our results show that, for the US, the payment and remittances and the market and trading support categories contribute the most to the VaR of the fintech industry. Instead, in Europe, fintech firms that provide software solutions and information technologies seem to be contributing the most to the risk of the sector. The estimation that includes fintech firms and the representative sample of the financial sectors show that fintech firms are not systemically important. Within the US financial system, the fintech companies that do contribute to systemic risk increase it by around 0.03%, while, in Europe, fintech firms contribute very little to the systemic impact (close to 0%). The Spearman’s rank correlation between a fintech firm’s ∆CoVaR and its respective size and between a fintech firm’s ∆CoVaR and its beta strengthens the importance of our estimations for a better assessment of systemic risk rather than just relying on the size and the beta of the firms to determine their likely contribution to systemic risk.

Some limitations of our study include the scope of our analysis method (∆CoVaR), the representation of the fintech sector, and the analysis of only two markets. However, micro-level data analysis focusing on each individual fintech category and changing the focus on emerging markets could reveal the specific risks, highlighting key research lines.

The financial cycle plays a key role in the functioning of the economy, as we have seen in the previous articles of this Dossier. But what are the specific consequences of the relationship between the financial and business cycle? Below we analyse its implications for one of the key macrofinancial relationships: the one that exists between the financial cycle and equilibrium interest rates.

The ECB and the Fed have initiated a process to review their strategy, the results of which will be published during the course of 2020. This review has been driven by certain structural changes in advanced economies, such as the decline in the equilibrium interest rate and the flattening of the Phillips curve.

While we do not anticipate disruptive changes, it is likely that the Fed will reinforce the symmetry of its inflation target and that the ECB will adopt a similar model in order to shore up inflation expectations.

El envejecimiento poblacional será uno de los factores clave que, junto con la revolución tecnológica y el cambio climático, redefinirán nuestras sociedades en las próximas décadas. Una población más envejecida cambiará forzosamente no solo la configuración de nuestras sociedades sino también la de nuestras economías, pues el envejecimiento poblacional tiene un impacto significativo sobre el crecimiento económico. Esta es la cuestión que abordaremos en este y en los siguientes artículos del Dossier, poniendo el foco en las economías española y portuguesa.

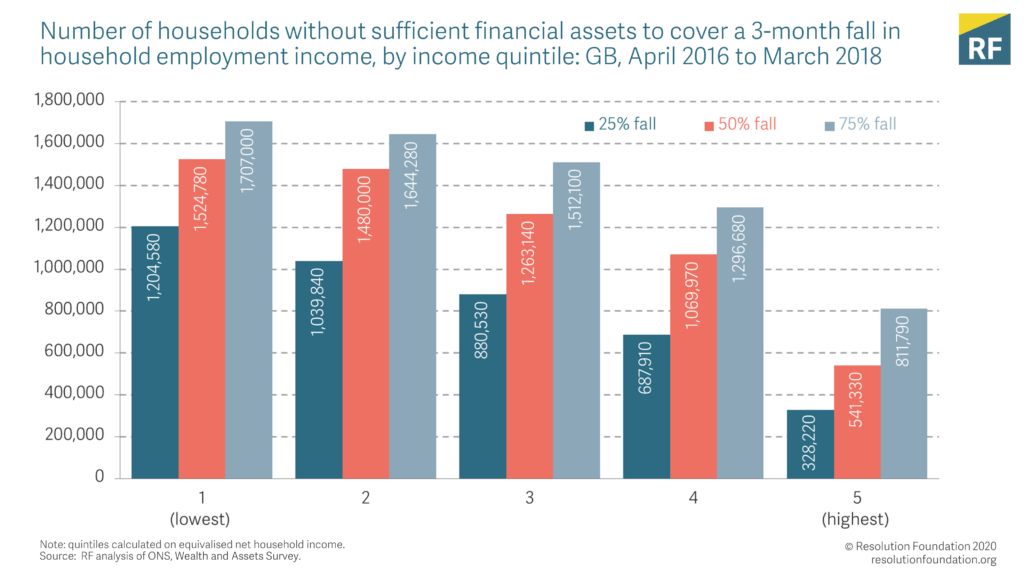

Article by George Bangham ’17 (Economics of Public Policy)

In an article for the Resolution Foundation, George Bangham ’17 (Economics of Public Policy) looks at data on UK family finances in the period before the coronavirus pandemic and thinks about policy measures for those who may lose their primary source of income during the crisis.

Here is an excerpt:

We won’t know exactly how many people have lost their jobs due to coronavirus until at least the summer, when official statistics come out. But as well as monitoring the ongoing impact of the crisis, it’s equally important to consider the state of the country as the economic downturn hit home…

Amid the horror of the pandemic, and the legitimate fears of many families for their finances, it might seem frivolous to worry about statistics for the time being. But the lessons from the data are vital. They point us to new issues that the Government must fix. In a crisis, statistics can save livelihoods and save lives.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.