Barcelona GSE alum Miguel Ángel Santos (ITFD ’11 and Economics ’12) is Senior Research Fellow at the Center for International Development at Harvard University. He recently won an award for a paper he has written with Harvard Professor Carmen Reinhart. In this post, he shares some background on the paper and some results.

I approached Carmen Reinhart last year, while I was a Mason Fellow at the Kennedy School. She said she would be very interested in writing something about Venezuela. It turns out that Venezuela is such an anachronic, chaotic economy, that it allows us to study some economic phenomena in a way no other place does.

My idea was writing about foreign debt sustainability and default probabilities, etc. Carmen suggested otherwise. After all, lots of people have been working on foreign debt sustainability, and it would not be interesting adding to that pile of work.

Instead, she suggested looking into domestic debt default via financial repression, and associating that to leakages in the capital account that in turn weakened the foreign asset position. It goes against some market analysts’ assessment that Venezuela can go wild internally, wild being able to serve its external debt without any trouble. So we used two modified formulas for estimating financial repression for the previous 30 years, differentiating free market years from years of exchange controls.

Our results

We proved that financial repression it is not only significantly higher in periods of exchange controls, but also that the sheer size in Venezuela was astounding, equivalent to more developed countries with much larger internal debt-to-GDP ratios. That is to say, with a smaller stock of domestic debt, the Venezuelan regime needs a lot more repression to collect that. So they actually engineer it, creating mechanisms to produce it: right now inflation is running at a rate five times higher than yields on domestic bonds or bank deposits.

We moved on to show that capital flight, conceived in broader sense, including the over-invoice of imports, was higher in periods of exchange controls. Since financial repression is rampant in periods of controls, people will run risks just to jump out of domestic currency and get into dollars (capital flight). They do that by two means: buying dollar-denominated bonds that the government has been selling in exchange for domestic currency, and over-invoicing imports. We measured the latter by a very innovative process, contrasting Central Bank reported imports with the sum of imports reported at Venezuelan customs. The difference is not only significantly higher across years of controls, but over those years it is 3-4 standard deviations away from the distribution of this error worldwide.

I presented the paper two weeks ago in San Juan, Puerto Rico, within the Business Association of Latin American Studies (BALAS), where it was granted the Sion Raveed Award, given to the best paper of the conference.

Comments welcome from the Barcelona GSE community

CID has published the paper on their working paper series. All comments from the BGSE Alumni and scholars community are welcome at this point. It is a modest paper, dealing with a small, crazy economy. And yet I think it makes a significant contribution.

Barcelona GSE Macro alum Naomi Fink ’13 offers analysis of Japan’s recent structural reforms in The Diplomat this month.

Barcelona GSE Macro alum Naomi Fink ’13 offers analysis of Japan’s recent structural reforms in The Diplomat this month:

Japan analyst Naomi Fink, chief executive of Europacifica Consulting, argues that stagnant “total factor productivity” (TFP) and unstable labor/capital shares of income are at the heart of the nation’s economic problems – and short-term fiscal and monetary adjustments simply “won’t cut it.”

Thomas Walsh ’14 is a Research Assistant at Bruegel and graduate of the Barcelona GSE Master in Macroeconomic Policy and Financial Markets. His recent post on the think tank’s blog, co-authored with Research Fellow Grégory Claeys, examines recovery numbers for countries coming out of deep recessions:

The recovery in certain economies (particularly in the Baltics and more recently in the UK or Spain) is often attributed to decisive economic policies (e.g. quick structural adjustment in Latvia, quantitative easing in the UK or labour market reforms more recently in Spain). While this view may be true, a theory suggested by Milton Friedman in 1964 (and revisited in 1993) proposes a complementary hypothesis: these strong recoveries are just natural after particularly deep recessions…

Mr. Walsh also recently co-authored a post about the vulnerabilities of the Greek banking system on the think tank’s blog with Bruegel director Guntram Wolff: The Greek banking system: a tragedy in the making?

Jana Bobosikova ’10 is a graduate of the Barcelona GSE master program in International Trade, Finance and Development.

I was sitting in the Conference Room 1 at the United Nations in New York in summer 2013 amidst the Nexus Global Youth Summit attendees, listening to the opening address from Roland Rich, Executive Head of the United Nations Democracy Fund. The message I was hearing was clear and bold: we are here to take action. Not “we” as in policy makers and government funded multilateral agencies” but rather “we” as in Nexus, the global movement of Doers from the circles of the largest philanthropists, hardest working and most daring social entrepreneurs, investors, international advocates and NGOs.

Part of me was elated: so many influencers, all on the same page, with substantial financial and human commitment to contributing to making the world a better place!

Another part of me, the one I cultivated through the study of economic analysis at the ITFD program at Barcelona GSE, was a bit nervous about so much “good doing”.

I felt too aligned with the work of my former professor Xavier Sala-i-Martin and William Easterly that suggest that much of external help to date has had none or negative effect on socio-economic growth to simply embrace the possibility that Nexus Youth Summit was different and effective.

I sent a mental greeting to Prof. Antonio Ciccone and his often restated quest for the “one-handed economist” – creating one best solution with all relevant sets of variables – conclusions with no caveats “on the other hand.” Had I found them? What were the Nexus development solutions that gathered at the UN?

Let’s see:

We have been conditioned to include savings as a basic variable for economic growth models. At Nexus, Aron Ping D’Souza felt so compelled by the meeting of Sir Richard Cohen at an earlier Nexus Europe Youth Summit that he started an impact investing annulation fund, using the best practice from classic and impact investing to target over AUS$1.7 trillion pension funds to a creating a 2.0 return for the economy.

We learned about girls’ education challenges in developing countries. One of Nexus’ members, Nikki Agrawal, invested in researching and launching menstruation-absorbing underwear to address one of the most significant school attendance problems for girls.

We studied about how to create policies that incentivize investing into R&D for a healthier global population. At Nexus, it was a great honor to be joined by Jake Glaser, the son of Elizabeth Glaser who pioneered and prompted research and development in pediatric AIDs in early 1990s. It was the one case of AIDS transmission via blood transfusion during Elizabeth Glaser’s giving birth and her subsequent fight to save her children that has kickstarted the largest research and movement on eliminating pediatric AIDS – a vision that is now becoming a reality.

I could probably keep going and catalogue the amazing encounters and inspiring efforts of the hundreds (!) of international innovators, family offices that fund some of the largest projects as well as startup social entrepreneurs – that make up Nexus.

And maybe I should, so that the passion and commitment of the Nexus movement and the research and rigorous analysis from the realms of development economists could start catalyzing into aligned efforts to improve international trade, finance and socio-economic development.

“…One of my research projects is on the Panic of 1907. In many ways, it resembles our recent economic crisis. For me, the most startling resemblance is the absolute fear that the monetary authority had about any contraction in the credit market.”

Excerpt from the blog post Nothing New Under the Sun Brian C. Albrecht ’14 (Master in Economics)

PhD student at University of Minnesota

Barcelona GSE grad Alvaro Leandro looks at the EU’s Stability and Growth Pact through the lens of the draft budget plans of France and Italy.

The following post by Alvaro Leandro (ITFD’13 and Economics ’14) has been previously published by Bruegel.

Mr. Leandro is Research Assistant at Bruegel in Brussels, Belgium.

The EU’s fiscal framework, the Stability and Growth Pact (SGP), is a complicated system of fiscal rules. Rather than trying to assess the virtues and failures of the SGP, this blogpost aims at understanding its complex rules through the lens of the draft budget plans of France and Italy. France is in the corrective arm of the SGP, while Italy is now in the preventive arm, which allows the examination of various SGP requirements, such as the

structural balance pillar,

expenditure balance pillar,

and the debt criterion

which apply to countries in the preventive arm (like Italy), and the

headline budget deficit criterion,

the structural balance criterion,

and the cumulative structural balance criterion

which apply to countries in the corrective arm (like France). We also discuss the rules regarding financial sanctions.

On 28 November 2014, the European Commission released its opinions on the euro area Member States’ Draft Budgetary Plans for 2015. The purpose of these opinions is to assess each country’s compliance with the SGP, and to recommend appropriate action if there are risks of non-compliance.

Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”

One of the surprises was that, in the case of Italy and France (as well as Belgium), the Commission decided to postpone its recommendations until March 2015, “in the light of the finalisation of the budget laws and the expected specification of the structural reform programmes announced by the authorities“. Both Italy and France are “at risk of non-compliance with the provisions of the Stability and Growth Pact”, according to the Commission.

The Framework

The Stability and Growth Pact is composed of a preventive and a corrective arm. The corrective arm is called the Excessive Deficit Procedure (EDP), which is triggered for countries with a general government deficit larger than 3 percent of GDP or with debt larger than 60 percent of GDP not being reduced at a satisfactory pace. France is currently under the corrective arm and Italy was as well until 2013. Italy is therefore now subject to the rules of the preventive arm.

Source: Country Stability and Convergence Programmes for MTOs, AMECO for forecast of 2014 and 2015 Structural Balances

Notes: Data labels are for the MTOs. According to the Treaty on Stability, Coordination and Governance (TSCG), signed by all euro area members in March 2012, all signatory Member States must have an MTO higher than -0.5% of GDP (or -1% for countries with a debt/GDP ratio lower than 60%). The “fiscal” part of the TSCG is often called the ‘Fiscal Compact’.

The fundamental variables used to assess compliance with the preventive arm of the SGP are the country-specific medium-term budgetary objectives (MTOs), which are defined as structural balances (a measure of the government budget balance adjusted for the economic cycle and one-off revenue and expenditure items; this blog post by Zsolt Darvas explains the estimation methodology and why it has some drawbacks). MTOs are chosen by each Member State following strict guidelines set out by the Commission, in order to ensure sustainability in its public finances (a higher MTO is required from countries with a high debt ratio or with a rapidly-ageing population faced with increasing age related expenditure for example, while the ‘Fiscal Compact’ limits the MTO for euro area member states, see the notes to Figure 1). A few examples of MTOs can be found in Figure 1: France, Italy and Spain have an MTO of 0 percent of GDP, while Germany’s MTO is -0.5 percent. This means that in the case of Germany, for example, a structural deficit of 0.5 percent of GDP is deemed enough to ensure the sustainability of its public finances.

The Fiscal Compact is not binding for non-euro area Member States, which therefore have more freedom in setting their MTOs. For example, Hungary has an MTO of -1.7 percent, the Polish and Swedish MTO is -1 percent, while it is zero for the United Kingdom.

To comply with the preventive arm of the SGP, all Member States must be at their MTOs or be on a path to reach them, with an annual improvement of their structural balance of 0.5 percent of GDP towards the MTO as a benchmark.

A higher effort might be required for countries with high debt/GDP ratios and pronounced risks to overall debt sustainability. A higher effort is also required in good economic times, and a lower effort in economic downturns. A Member State could also be allowed to deviate from the adjustments if it experiences “an unusual event outside its control with a major impact on the financial position of the general government”.

Therefore compliance with the preventive arm is not defined by the Member State’s structural balance, but by its path towards the MTO.

Italy

Structural balance pillar: Table 1 shows the recommended path for Italy. On the 28th of November 2014 the Commission decided that “severe economic conditions” (namely a real GDP contraction and a large negative output gap: see Table 3) justified that Italy is not required to adjust its structural balance towards the MTO by the 0.5 percent of GDP benchmark in 2014. This is why the required change in the structural balance for 2014 is 0. Italy had originally planned a large correction of its structural budget for 2014 in its 2013 Stability Program, of 0.7 percentage points. In its Draft Budget Plan for 2014 Italy revised this adjustment to 0.3. Finally it invoked Article 5 of Regulation 1175/2011 in its 2014 Stability Program which allows a deviation from the required adjustment “in the case of an unusual event outside the control of the Member State concerned which has a major impact on the financial position of the general government”. The required adjustment is also 0 in 2013 for the same reason: negative real output growth makes Italy eligible to the escape clause. In 2015 real GDP is forecast by the Commission to increase by 0.6 (see Table 3), which means that Italy can no longer apply for the escape clause regarding economic downturns.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of Italy (28 November 2014), European Commission Autumn Forecast (November 2014), Italy’s Stability Programme April 2014, Italy’s Stability Programme April 2013, Vade Mecum on the Stability and Growth Pact (May 2013)

Note: ΔSB denotes the percentage point change in the structural balance. MLSA: minimum linear structural adjustment. DBP: draft budget plan

(1): Deviation of the growth rate of public expenditure net of discretionary revenue measures and revenue increases mandated by law from the applicable reference rate in terms of the effect on the structural balance. A negative sign implies that expenditure growth exceeds the applicable reference rate.

Expenditure balance pillar: Member States in the preventive arm of the SGP also have to comply with the expenditure benchmark pillar, which complements the structural balance pillar. It requires countries that are not at their MTO to contain the growth rate of expenditure net of discretionary revenue measures to a country-specific rate below that of its medium-term potential GDP growth. This medium-term potential GDP growth is calculated as a 10-year average (of the 5 preceding years, the current year and forecasts for the next 4 years), and in the case of Italy it is 0 percent in 2014 and 2015. Had Italy been at its MTO it would have had to contain net expenditure growth to 0 percent. However, not being at its MTO, it is required to contain net expenditure growth to a reference rate below medium-term potential GDP growth: -1.1 percent in 2015 (which is calculated so that it is consistent with a tightening of the budget balance of 0.5 percent of GDP when GDP grows at its potential rate). The applicable reference rate in 2014 is 0 because of the “severe economic conditions”. In 2013 the applicable reference rate was 0.3, which is different to that in 2014 and 2015 because it is revised every three years. The commission allows one-year and two-year average deviations of a maximum of 0.5 pp of GDP in terms of their impact on the structural balance. In 2015 the deviation in terms of its effect on the structural balance is forecast to be of 0.7 pp. of GDP, which is a deviation larger than the allowed 0.5 pp.

Debt Criterion: Countries which have recently left the EDP are subject to a 3-year transition period aimed at ensuring that the debt level is being reduced at an acceptable pace. Italy is in such a transition period, since it left the EDP in 2013. It is thus subject to required medium-term linear structural adjustments (MLSAs) aimed at ensuring that it will comply with the debt criterion. These MLSAs are formulated in terms of adjustments to the structural balance. Since Italy is in the preventive arm and therefore also subject to required adjustments towards the MTO, the largest one is applicable. The 2.5 pp. MLSA in 2015 (larger than the 0.5 pp. required change under the preventive arm) is at serious risk of not being met according to Commission forecasts. This violation of the debt criterion could lead to a reopening of the Excessive Deficit Procedure.

Commission’s view: In its opinion on Italy’s Draft Budget Plan released at the end of November 2014, the Commission points to risks of non-compliance with the requirements of the SGP, and “invites the authorities to take the necessary measures […] to ensure that the 2015 budget will be compliant with the Stability and Growth Pact”. It then says that “The Commission is also of the opinion that Italy has made some progress with regard to the structural part of the fiscal recommendations issued by the Council in the context of the 2014 European Semester and invites the authorities to make further progress. In this context, policies fostering growth prospects, keeping current primary expenditure under strict control while increasing the overall efficiency of public spending, as well as the planned privatisations, would contribute to bring the debt-to-GDP ratio on a declining path consistent with the debt rule over the coming years.”

France

Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit.

Headline budget deficit criterion: Once a country has been identified as having an excessive deficit, which was the case for France in 2009, it is turned over to the corrective arm, the EDP, the purpose of which is to correct such a deficit. France has now been under the EDP for 5 consecutive years, and is subject to requirements set out in the latest Council recommendation to end the excessive deficit situation (June 2013). The recommendation released in 2009 originally planned a correction of the deficit (below 3 percent) by 2012, which was then postponed to 2013 in view of the actions taken and the “unexpected adverse economic events with major unfavourable consequences for government finances”. In June 2013, the Council again postponed the correction of the deficit to 2015 for the same reasons: France fell slightly short of the required 1 percent average annual fiscal effort for the period 2010-2013 (the actual average annual fiscal effort was 0.9 percent), but this was again against a backdrop of “unexpected adverse economic events”.

Source: Commission Staff Working Document: Analysis of the draft budgetary plan of France (November 28, 2014), Council recommendation to end the excessive deficit situation (June 2013), European Commission Autumn Forecast (November 2014)

Note: ΔSB denotes the percentage point change in the structural balance

The latest Council recommendation (June 2013) sets out a path for France’s headline government balance, which you can see in Table 2. By 2015, the headline balance should be reduced to -2.8 percent of GDP. The forecast headline balance of -4.5 percent falls significantly short of this requirement.

Structural balance criteria: Additionally the adjusted change in the structural balance from 2014 to 2015 is forecast to be of 0.0 pp., and its cumulative change from 2012 to 2015 is forecast to be 1.6 pp., falling short of the requirements of 0.8 pp. and 2.9 pp. respectively (1). The structural budget also deviates from the requirements for 2014.

Commission’s view: Thus France is “at a risk of non-compliance” with the SGP, and, contrary to Italy, the Commission “is also of the opinion that France has made limited progress with regard to the structural part of the fiscal recommendations issued by the Council […] and thus invites the authorities to accelerate implementation”. In his letter to the President of the European Commission, France reiterated its determination to go ahead with reforms, most notably in the labour market. It remains to be seen whether progress by March 2015 will be assessed to be sufficient by the Commission.

Table 3: France and Italy: main macroeconomic indicators in 2014 and 2015

Sanctions

Non-compliance with the SGP can lead to sanctions. In the preventive arm, a Council recommendation which is not respected can lead to an interest-bearing deposit of 0.2 percent of GDP. A euro-area country in the corrective arm of the SGP may be required to make a non-interest bearing deposit until the deficit has been corrected, after which it can also be sanctioned with a fine worth up to 0.5 percent of GDP (with a fixed component of 0.2 percent of GDP and a variable component (2)). France and Italy are both at a risk of non-compliance with the requirements of the SGP. Failure to meet the required efforts in terms of fiscal consolidation and structural reforms by March 2015 could bring them closer to possible sanctions, unless the flexibility of the SGP is stretched further. Recent growth and inflationary figures suggest continued weak economic activity, and if economic data of 2014 qualified for “severe economic conditions”, 2015 may qualify too, especially if growth and inflation will disappoint relative to the November 2014 ECFIN forecasts. And in the preventive arm, structural reforms which have a verifiable positive impact on the long-term sustainability of public finances (such as by raising potential growth) could be considered when assessing the adjustment path to the medium-term objective.

Notes:

(1) The adjusted changes in the structural balance correct for the negative impact of the changeover to ESA 2010 as well as for changes in potential growth and revenue windfalls/shortfalls.

(2) This variable component is equal to “a tenth of the absolute value of the difference between the balance as a percentage of GDP in the preceding year and either the reference value for government balance, or, if non-compliance with budgetary discipline includes the debt criterion, the government balance as a percentage of GDP that should have been achieved in the same year according to the notice issued”

Liyun Chen ’11 (Economics) is Senior Analyst for Data Science at eBay. She recently moved from the company’s offices in Shanghai, China to its headquarters in San Jose, California. The following post originally appeared on her economics blog in English and in Chinese. Follow her on Twitter @cloudlychen

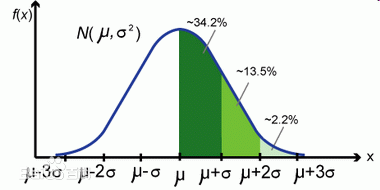

Variance is an interesting word. When we use it in statistics, it is defined as the “deviation from the center”, which corresponds to the formula , or in the matrix form (1 is a column vector with N*1 ones). From its definition it is the second (order) central moment, i.e. sum of the squared distance to the central. It measures how much the distribution deviates from its center — the larger the sparser; the smaller the denser. This is how it works in the 1-dimension world. Many of you should be familiar with these.

Variance has a close relative called standard deviation, which is essentially the square root of variance, denoted by // . There is also something called the six-sigma theory– which comes from the 6-sigma coverage of a normal distribution.

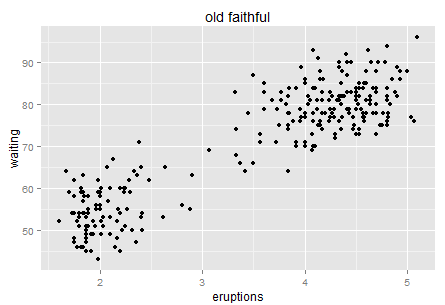

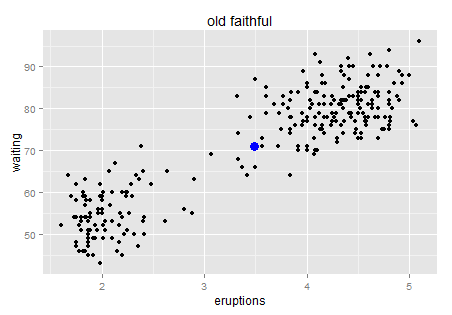

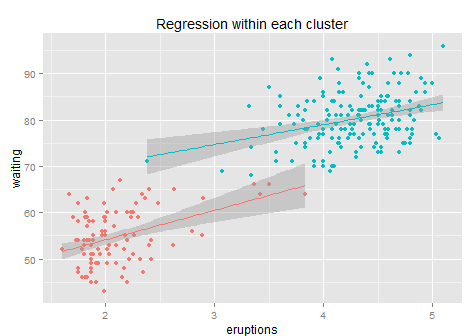

Okay, enough on the single dimension case. Let’s look at two dimensions then. Usually we can visualize the two dimension world with a scatter plot. Here is a famous one — old faithful.

Old faithful is a “cone geyser located in Wyoming, in Yellowstone National Park in the United States (wiki)…It is one of the most predictable geographical features on Earth, erupting almost every 91 minutes.” We can see there are about two hundreds points in this plot. It is a very interesting graph that can tell you much about Variance.

Here is the intuition. Try to use natural language (rather than statistical or mathematical tones) to describe this chart, for example when you take your 6 year old kid to the Yellowstone and he is waiting for next eruption. What would you tell him if you have this data set? Perhaps “I bet the longer you wait, the longer next eruption lasts. Let’s count the time!”. Then the kid has a glance on your chart and say “No. It tells us that if we wait for more than one hour (70 minutes) then we will see a longer eruption in the next (4-5 minutes)”. Which way is more accurate?

Okay… stop playing with kids. We now consider the scientific way. Frankly, which model will give us a smaller variance after processing?

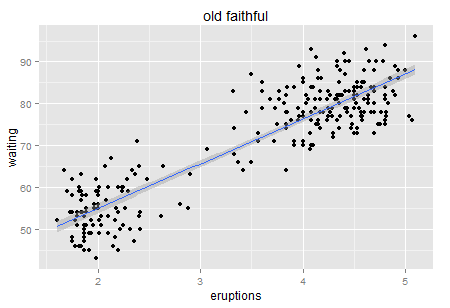

Well, always Regression first. Such a strong positive relationship, right? ( no causality…. just correlation)

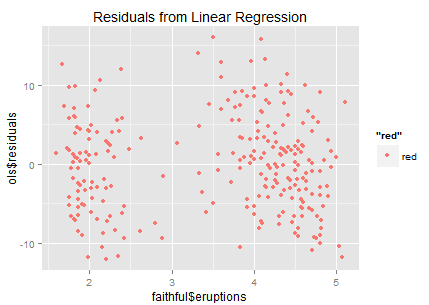

Now we obtain a significantly positive line though R-square from the linear model is only 81% (could it be better fitted?). Let’s look at the residuals.

It looks like that the residuals are sparsely distributed…(the ideal residual is white noise which carries no information). In this residual chart we can roughly identify two clusters — so why don’t we try clustering?

Before running any program, let’s have a quick review the foundations of the K-means algorithm. In a 2-D world, we define the center as // , then the 2-D variance is the sum of squares of each pint going to the center.

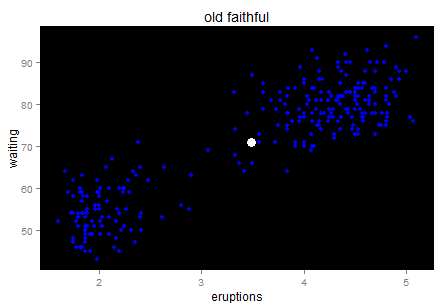

The blue point is the center. No need to worry about the outlier’s impact on the mean too much…it looks good for now. Wait… doesn’t it feel like the starry sky at night? Just a quick trick and I promise I will go back to the key point.

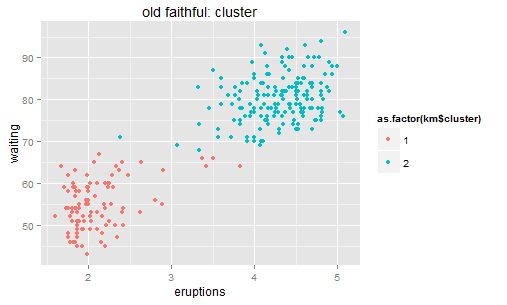

For a linear regression model, we look at the sum of squared residuals – the smaller the better fit is. For clustering methods, we can still look at such measurement: sum of squared distance to the center within each cluster. K-means is calculated by numerical iterations and its goal is to minimize such second central moment (refer to its loss function). We can try to cluster these stars to two galaxies here.

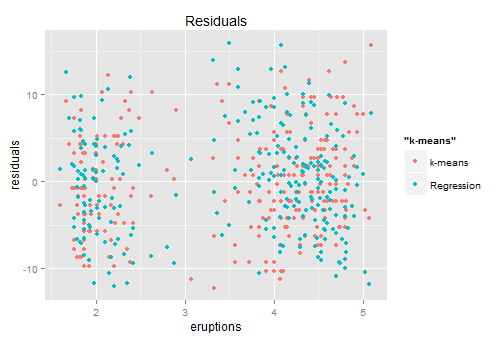

After clustering, we can calculate the residuals similarly – distance to the central (represents each cluster’s position). Then the residual point.

Red ones are from K-means which the blue ones come from the previous regression. Looks similar right?… so back to the conversation with the kid — both of you are right with about 80% accuracy.

Shall we do the regression again for each cluster?

Not many improvements. After clustering + regression the R-square increases to 84% (+3 points). This is because within each cluster it is hard to find any linear pattern of the residuals, and the regression line’s slope drops from 10 to 6 and 4 respectively, while each sub-regression only delivers an R-square less than 10%… so not much information after clustering. Anyway, it is better than a simple regression for sure. (the reason why we use k-means rather than some simple rules like x>3.5 is that k-means gives the optimized clustering results based on its loss function).

Here is another question: why do not we cluster to 3 or 5? It’s more about overfitting… only 200 points here. If the sample size is big then we can try more clusters.

Fair enough. Of course statisticians won’t be satisfied with these findings. The residual chart indicates an important information that the distribution of the residuals is not a standard normal distribution (not white noise). They call it heteroscedasticity. There are many forms of heteroscedasticity. The simplest one is residual increases when x increases. Other cases are in the following figure.

The existence of heteroscedasticity makes our model (which is based on the training data set) less efficient. I’d like to say that statistical modelling is the process that we fight with residuals’ distribution — if we can diagnose any pattern then there is a way to improve the model. The econometricians prefer to name the residuals “rubbish bin” — however it is also a gold mine in some sense. Data is a limited resource… wasting is luxurious.

Some additional notes…

Residuals and the model: as long as the model is predictive, then residuals exist, regardless of the model’s type, either a tree or linear or whatever. Residual is just the true Y minus the prediction of Y (based on training data set).

Residuals and loss function: for ordinary least squares, if you solve it in the numerical way then it iterates by the SSR (sum of squared residuals) loss function (equals to the variance of residuals). In fact many machine learning algorithms relay on a similar loss function setting — either first order or higher order moments of residuals. From this perspective statistical modelling is always fighting with residuals. This differs from what the econometricians do so there was a huge debate on the trade off between consistency and efficiency. Fundamentally different believes of modelling.

Residuals, Frequentists and Bayesians: In the above paragraphs I mainly followed the Frequentist’s language. There was nothing on posterior… From my understanding many items there would be mathematically equivalent to the Bayesian’s frameworks so it should not matter. I will mention some Bayesian ideas in the following bullets so go as you wish.

Residuals, heteroscedasticity and robust standard error: We love and hate heteroscedasticity at the same time. It tells us that our model is not perfect while there is a chance to make some improvements. Last century people tried to offset heteroscedasticity’s impact by introducing the robust standard error concept — Heteroscedasticity-consistent standard errors, e.g. Eicker–Huber–White. Eicker–Huber–White changes the common sandwich matrix (bread and meat) we use for the significant test (you may play with it using the sandwich() package in R). Although Eicker–Huber–White contributes to the variance estimation by re-weighing with estimated residuals, this approach does not try to identify any patterns from the residuals. Thus there are methods like Generalized least square (GLS) and Feasible generalized least square (FGLS) that try to use a linear pattern to reduce the variance. Another interesting idea is clustered robust standard error which allows heterogeneity among clusters but constant variance within each cluster. This approach only works when the number of groups approaches infinite asymptotically. (otherwise you will be getting stupid numbers like me!)

Residuals and reduction of dimensions: generally speaking the more relevant co-variates introduced to the model the less the noise is; while there is also a trade-off towards overfitting. That is why we need to reduce the dimensions (e.g. via regularization). Moreover, it is not necessary that we want to make a prediction every time; sometimes we may want to filter out the significant features — a sort of maximizing the information we could get from a model (e.g. AIC or BIC or attenuation speed which increasing the punishment in regularization). In addition regularization is not necessarily linked to train-validation… not the same goal.

Residuals and experimentation data analysis: heteroscedasticity will not influence the consistency of Average Treatment Effect estimation in an experimentation analysis. The consistency originates from randomization. However people are still eager to learn more beyond a simple test-control comparison, especially when the treated individuals are very heterogenous; they look for heterogenous treatment effect. Quantile regression may help in some case if there is a strong covariate observed…but what could we do when there are thoudsands of dimensions? Reduce the dimension first?

Well, the first reaction to “heterogeneous” should be variance…right? otherwise how could we quantify heterogeneity? There is also a bundle of papers that try to see whether we would be able to find more information for treatment effects rather than simple ATE. This one for instance:

Ding, P., Feller, A., and Miratrix, L. W. (2015+). Randomization Inference for Treatment Effect Variation. http://t.cn/RzTsAnl

Víctor Burguete ’11 (International Trade, Finance and Development) is an Economic Researcher and Public Policy Analyst at IESE’s Public-Private Sector Research Center (IESE-PPSRC) in Barcelona. In this post, he shares the process of preparing a policy brief on Spanish policy reforms and provides an overview of the brief’s findings.

Preparing a Policy Brief like this took me over a month. It is necessary to consider than working in a research institution implies getting involved in many projects and there is usually less time than what I would like to devote to one specific project. In my opinion, it is very important to work open-minded and to continuously consider the possible connections among different projects. In the case of this Policy Brief, most of the data (international economic policy recommendations) were collected during the past few months. In late September I proposed this topic and the IESE-PPSRC research center decided to inaugurate these series of papers. After reviewing the literature (Table 1), I analyzed the data and I started creating some graphs and building the story I wanted to tell. Of course, the final text was reviewed several times until it was finally published.

“Spain’s response to EC and OECD economic policy recommendations” analyses the overall reformist progress of the Spanish Government in an international perspective. According to the international assessment, Spain ranks as one of the top reformers in the Euro Area and the EU as a whole. A second insight one gets from our Policy Brief is that Spain’s delivery, in relative terms to other countries, accelerated between 2011 and 2013.

Of course, this is the general trend and the Policy Brief offers details on the progress in the 18 policy sub-areas we cover at the SpanishReforms project, including how the reform priorities prescribed to Spain by these institutions have changed over time. Substantial progress is recognized in addressing the financial system reform, mainly in the area of recapitalization and restructuring but also by adopting other financial measures. However, both the OECD and the EC point to active labour market policies and professional services as the main structural reforms lagging behind.

More information in www.spanishreforms.com, a new an academic, non‐governmental website that aims at being a useful reference for those interested in independent, rigorous and up‐to‐date information about the Spanish economy and its economic policy reforms.

Ms. Tschekassin is Research Assistant at Bruegel in Brussels, Belgium. Follow her on Twitter @OlgaTschekassin

Since the beginning of the global financial crisis, social conditions have deteriorated in many European countries. The youth in particular have been affected by soaring unemployment rates that created an outcry for changes in labour market policies for the young in Europe. Following this development, the Council of Europe signed a resolution in 2012 acknowledging the importance of this issue and asking for implementation of youth friendly policies in the Member States. Yet, almost 5.6 million young people were unemployed in 2013 in the European Union (EU) – in nine EU countries the youth unemployment rate more than doubled since the beginning of the crisis.

Today I want to draw your attention to two more indicators reflecting the social situation of the young generation: the percentage of children living in jobless households and the percentage of young people that are neither in employment nor education nor training.

Children in jobless households

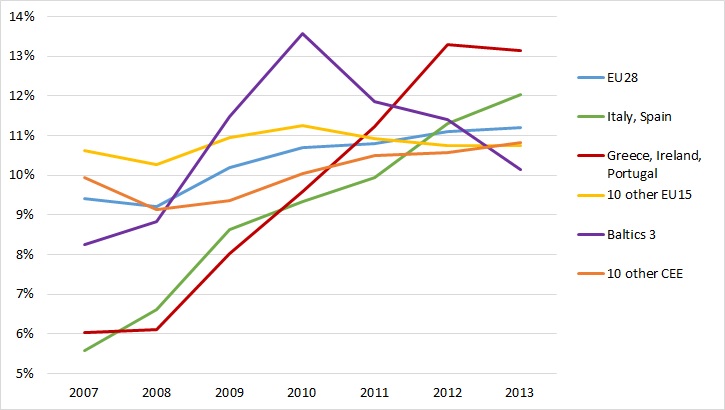

The indicator Children in jobless households measures the share of 0-17 year olds as a share of the total population in this age group, who are living in a household where no member is in employment, i.e. all members are either unemployed or inactive (Figure 1).

Figure 1: Children in jobless households

Source: Eurostat and Bruegel calculations. Country groups: 10 other EU15: Austria, Belgium, Denmark, Finland, France, Germany, Luxembourg, Netherlands, Sweden and United Kingdom; Baltics 3: Latvia, Lithuania, Estonia; 10 other CEE refers to the 10 member states that joined in the last decade, excluding the Baltics: Bulgaria Czech Republic, Croatia, Hungary, Poland, Romania, Slovenia, Slovakia, Cyprus and Malta; Sweden: data for 2007 and 2008 is not available, the indicator is therefore assumed to evolve in line with the other 9 EU15 countries. Such approximation has only a marginal impact on the aggregate of the other EU15 countries, because children in jobless HHs in Sweden represented only 3% of the country group in 2009. Countries in groupings are weighted by population.

In the EU28 countries this share rose only slightly over the past years to 11.2%. It is striking, however, that the ratio of children living in households where no one works more than doubled in the euro-area programme countries (Greece, Ireland, Portugal) as well as in Italy and Spain to 13% and 12%, respectively. And even more shocking – while the share stabilized in the programme countries, in Italy and Spain it is still sharply increasing. In Ireland in 2013 more than one in every six children lived in a household where no one worked. This is indeed an alarming development. Only the Baltics, which experienced a very deep recession among the first countries hit by the crisis, are reporting a sizable turning point in the statistic in 2010 and the share is presently continuing to decline. The numbers are, however, still well above pre-crisis levels.

A high share of children living in jobless households is not only problematic at the moment but can also have negative consequences for the young people’s future since it often means that a child may not only have a precarious income situation in a certain time period, but also that the household cannot make an adequate investment in quality education and training (see a paper on this issue written for the ECOFIN Council by Darvas and Wolff here). Therefore a child’s opportunities to participate in the labour market in the future are likely to be adversely affected. Moreover, as I discussed in a blog earlier this year, children under 18 years are more affected by absolute poverty than any other group in the EU and the generational divide is widening further.

Not in Education, Employment or Training (NEET)

The financial situation of young people between 18 and 24 years old who finished their education is less dependent on their parents income because they usually enter the labour market and generate their own income. Therefore we are going to have a closer look on their work situation, i.e. how many young people have difficulties participating in the labour market.

Figure 2: Not in Education, Employment or Training

Source: Eurostat and Bruegel calculations. Country groups as in previous chart

The NEET indicator measures the proportion of young people aged 18-24 years which are not in employment, education or training as a percentage of total population in the respective age group. We can see in Figure 2 that the situation among EU28 countries stabilized over the last four years. The good news is that for the first time since 2007 we see a decline in the rate in the euro-area programme countries in 2013. This decline is, however, mostly driven by Ireland with an unchanged situation in Greece and Portugal. Also, in the Baltics the ratio is on a downward trend. More worrying, however, is the situation in Italy and Spain. Among all EU28 countries, the young generation in Italy with 22.2% of all young people being without any employment, education or training, is disproportionately hit by the deterioration in the labour market. Every fifth young person between 18 and 24 is struggling to escape the exclusion trap. Europe and especially Italy is risking a lost generation more than ever.

Labour market policies for young people should therefore stand very high on the national agendas of Member States. The regulations introduced in summer 2013 into the Italian labour market reform which are setting economic incentives for employers to hire young people build an important step towards more labour market integration of the youth in Europe. Their effects are yet to be observed in the employment statistics in the coming years in Italy. More action on the national and European level is needed to improve the situation of the young.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.

Liyun Chen

Liyun Chen

{kind=link}