This paper studies the spillover of a macroprudential regulation in Spain to the Mexican financial system via Mexican subsidiaries of Spanish banks. The spillover caused a drop in the supply of household credit in Mexico. Municipalities with a higher exposure to Spanish subsidiaries experienced a larger contraction in household credit. These localized contractions caused a drop in macroeconomic activity in the local non-tradable sector. Estimates of the elasticity of loan demand by the non-tradable sector to changes in household credit supply range from 1.2–1.8. These results emphasize cross-border effects of regulations in the presence of global banks.

Key takeaways

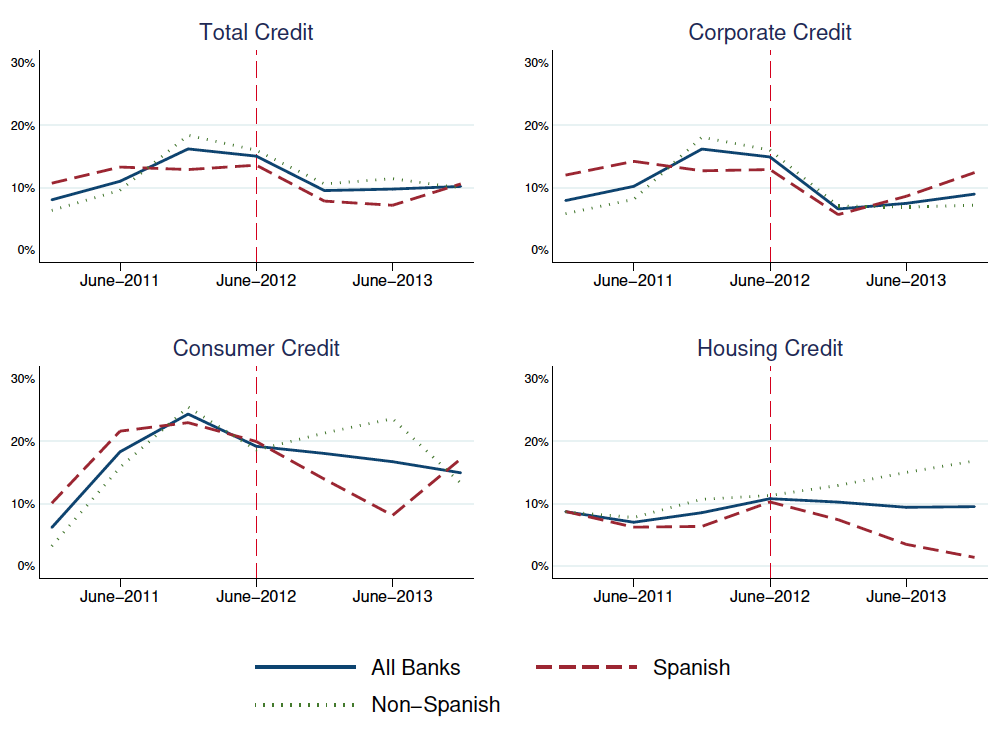

Loan-loss provisions introduced in Spain in 2012 imposed a significant burden on the balanced sheet of Spanish banks. This regulation was unrelated to the Mexican financial system or the credit conditions of Mexican households. However, Mexican subsidiaries of two large Spanish banks, BBVA and Santander, reduced lending to Mexican households in response to the regulation (Fig. 1).

Fig. 1. Growth in credit lending by Spanish and non-Spanish banks in Mexico.

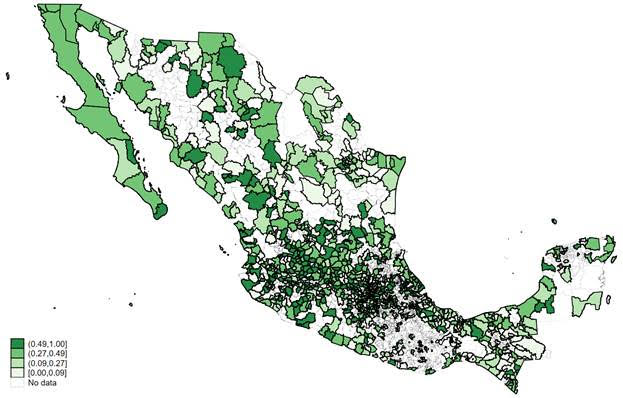

Mexican municipalities with a higher exposure to Spanish banks (Fig. 2) experienced a larger contraction in lending to households. This drop in lending to households (i.e. a drop in credit supply) was associated with a reduction in lending to the local non-tradable sector driven by a drop in local demand. This shows (1) cross-border effects of a macroprudential regulation on lending and economic activity, and (2) the macroeconomic effects of shocks in lending to households in an emerging economy.

Fig. 2. Share of Spanish banks in the household credit market across Mexican municipalities.

Antonia Esser ’11 (International Trade, Finance, and Development)

I started to work on remittances around three years ago when

I joined my current organization, the Centre for Financial Regulation and

Inclusion (or Cenfri in short) as a

researcher. We are an independent, not-for-profit think-and-do-tank based in

Cape Town, South Africa, trying to answer complex questions around the role of

the financial sector in improving individuals’ welfare in emerging economies.

Remittances is one of our key focus areas and we have received donor funding

from Financial Sector Deepening Africa (FSDA)

to understand why the cost of sending funds into Africa is still the highest in

the world.

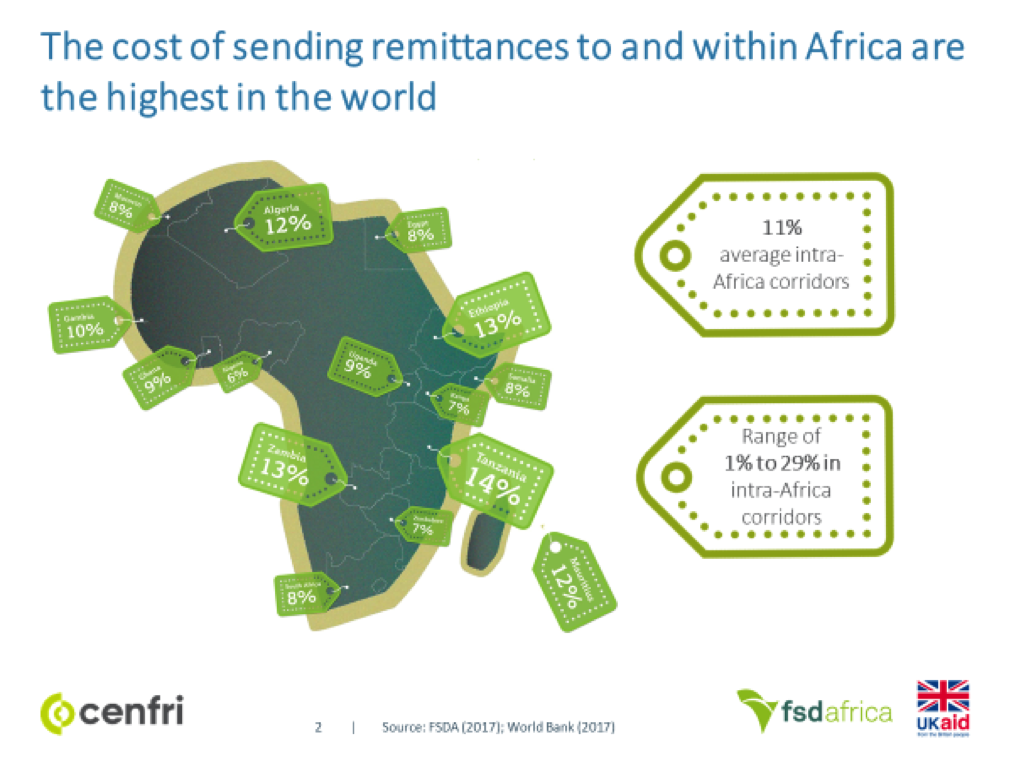

According to the World Bank, the average cost of sending remittances globally stood at just under 7% of the total value of the transfer in the first quarter of this year; in sub-Saharan Africa (SSA), consumers had to pay on average 9.25% – by far the most expensive region in the world. The SDGs want to bring down the cost to between three and five percent. Most disturbingly, intra-Africa transfers can cost way more than 15% in some corridors, even when the countries are neighbours (e.g. Nigeria and Cameroon where a transfer can cost 15%). The following graphic shows the average prices some time in 2017 between the UK and selected African countries.

The cost of sending remittances to and within Africa are the highest in the world. Sources: FSDA (2017) and The World Bank (2017)

When one considers that around 80% of African migrants stay

within Africa, this is an incredibly high burden in terms of cost that reduces

the positive impact of these essential flows for recipients. Many migrants are

therefore forced to use informal mechanisms that are often cheaper, more

trusted and more convenient. Yet informal mechanisms can be fronts for illicit

financial flows, including money laundering and the financing of terrorism.

They also indirectly influence competition as they mask the true size of a

remittance corridor, deterring providers from entering the market.

Formal remittance flows are now higher than the value of

official development assistance (ODA) and foreign direct investment (FDI). They

have shown to have significant positive impact as they flow directly in the

hands of those that rely on these funds as a primary source of income, and they

tend to be more stable than ODA or FDI.

Based on all this evidence, FSDA asked us to understand the cost

drivers and why it is still so expensive to send money to and within the

continent despite all the innovations in the FinTech space with apps from

players such as WorldRemit. We embarked

on a journey to collect evidence through stakeholder interviews (with private

sector players such as money transfer organisations, banks, FinTechs, and post

offices, as well as regulators, policy makers and experts), mystery shopping, speaking

to consumers, and ploughing through existing literature. We travelled to

important remittance markets such as Nigeria, Ethiopia, Côte d’Ivoire and

Uganda last year to understand the situation on the ground.

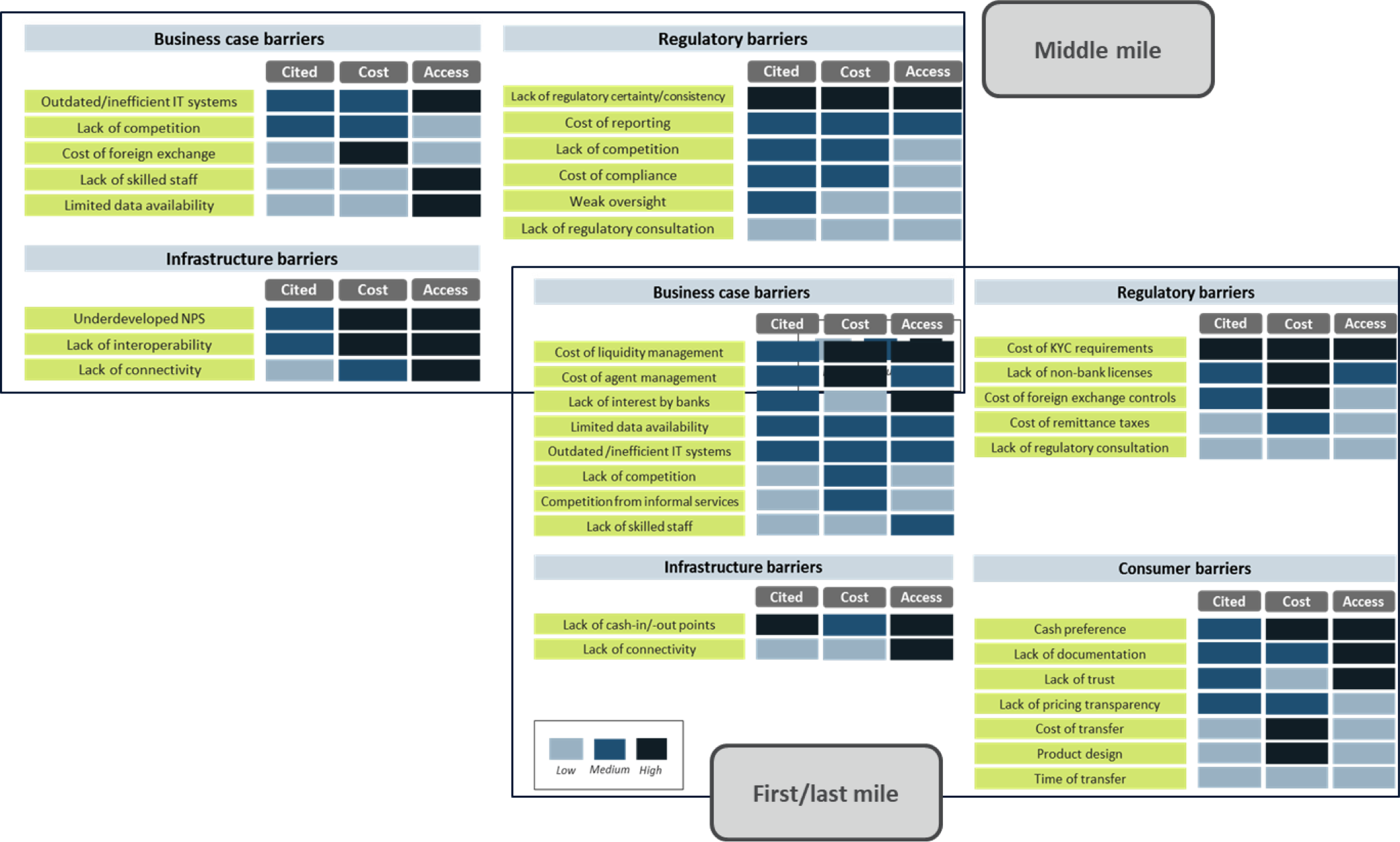

What I’ve learned since then is that remittances are an

incredibly complicated business. It consists of providers in the first mile

(where cash sending happens), the middle mile (where the processing of payments

happens) and the last mile (where the recipient collects the money). The value

chain is therefore very long and brings with it not only partnership complications

but also technical issues. Cross-border money transfers are heavily regulated

due to money laundering fears and severe risk exposure, but especially in

Africa capital outflows of any kind are also heavily controlled in many markets

still. To get a money transfer license can sometimes take a decade, we heard

from some providers.

Overall, there were many interesting insights but at the end of the day we narrowed the reasons for the high costs down to four categories: business case barriers, regulatory barriers, infrastructure barriers and consumer-facing barriers. We then evaluated the number of citations and their impact on cost and access for the consumer to show how severe the barrier is for both providers and consumers:

From these insights we produced a range of reports, that you

can access here,

if you are interested, with the aim to disseminate them at key events and bring

them into relevant discussions with the various stakeholders.

One avenue we are pursuing is to reduce the regulatory

burden for providers to stimulate competition, especially in intra-Africa

corridors. Many cross-border corridors are still dominated by one or two

companies such as Western Union or MoneyGram that can set their prices freely.

They are helped by the regulation as the licensing requirements in some cases

can be incredibly high. For example, you may need to show capital of USD 20

million, be operational in at least seven countries for at least ten years. Of

course, none of the newer players that can offer cheaper remittances through

using apps, for example, can meet all

these requirements.

We were therefore on the hunt to influence regulators to revise some of the regulations. And a lot of regulation touches cross-border remittances: payment system act, banking act, foreign exchange act, agent banking regulation, e-money regulation, telecommunications regulation, cross-border transfer regulation etc – the list goes on and on. Every country seems to have their own set of rules and regulations that need to be made interoperable or at least harmonise to reduce the regulatory burdens in a value chain that can cross many jurisdictions. Definitely not an easy task! Many African countries are still heavily dependent on natural resources, such as Nigeria on oil for example. Their exchange rate with the dollar is fixed by the central bank. Yet, the Nigerian Naira is overvalued, leading to a parallel shadow market where one can get better rates for dollars on the streets of Lagos, impacting the use of formal remittance channels. But of course, the regulator is very concerned with financial stability and the impact a devaluation could have on foreign exchange reserves, inflation etc. Attracting more formal remittances does not sway the regulator enough to change the exchange rate policies. All of these realities need to be taken into consideration when approaching the regulators to try and achieve change based on research, and of course protocols play a huge role.

As part of this effort to reach regulators and based on the

research we had done, I was recently invited to attend the inaugural meeting of

experts, organized by the African Institute for Remittances (AIR), which is a programme established by

the African Union. We were called from all over the continent based on our

research and professional experience to build a cohort that would give

technical assistance to willing African regulators. Last month we met in

Mombasa, Kenya, and learned more about the planned interventions. On the one

hand, we want to achieve better remittance data quality in the individual

countries as the data can be questionable, but on the other hand we want to

assist with writing the right kind of regulation that fosters innovation,

reduces cost without reducing the access for consumers, and incentivise the

uptake of formal remittance mechanisms.

Looking foreward to three days of learning, sharing experiences and plotting the way forward with colleagues from all over Africa with @_AfricanUnion and African Institute for Remittances #remittancepic.twitter.com/kERFXsVpVC

I learned which data point to allocate to which balance of

payment code at the central bank to make sure there is consistency across

countries. I also learned how we will go about understand the regulatory

background, as of course there is a difference between de jure and de facto

regulation, i.e. we need to understand how regulation is interpreted from a

stakeholder point of view.

So far it has been an exciting journey to see how we can

take our insights into regulatory change. Some countries have already shown

interest in being assessed and assisted and we will receive a list of our

country missions as the expert cohort soon. Judging from our past work with

regulators, this process can take many months, years if not decades but the

potential impact of such fundamental changes is immense, especially for the

individual person on the ground. System-level impact takes patience and

perseverance.

ITFD taught me to be precise and on-point with my research to effect change – policy makers do not want to read 300 pages no matter how well-researched the material is. Insights need to be relatable and digestible, yet you also need to be able to raise funding for important interventions even if they seem cumbersome. We are lucky that FSDA has such a mandate and I look forward to continuing this journey with them and the African Union. Hopefully I will be able to report a significant drop in remittance prices due to regulatory change soon..ish.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2014. The project is a required component of every master program.

Too-many-to-fail: a theoretical approach

Author:

Jaume Martí

Master Program:

Finance

Paper Abstract:

The recent financial crisis has generated enormous economic and human costs. New regulatory framework has been proposed in order to provide banks with better incentives.

My goal in this project is to theoretically explain several market failures that happened prior to the financial crisis and propose a model that captures these phenomena in the banking sector. To end up, I suggest different macroprudential measures that could be undertaken with the ultimate objective of providing a more stable financial system.

Editor’s Note: The following post comes from Sergio Gutiérrez. Sergio is a Chicago-based designer and strategist working at the intersection of people, business, and technology. He graduated from BGSE’s MSc Economics of Science and Innovation in 2011.

So, as it seems, healthcare in the U.S. seems to be in of trouble and, all the voices say, design can do a lot to solve the problem. For this reason, many design and innovation consulting firms are making healthcare a strong focus area. For any designer —or any person trained to solve problems for that matter— this type of problem, because of its complexity, potential impact, and evident “higher purpose” is also very attractive.

However, regardless all the hype around this topic, thinking of design as the main driver for structural change may prove a bit unrealistic — as much as I would like to think that design can save the world. In reality, given the magnitude of the problem in the U.S., this needs to be attacked from different angles, with various strategies and tools and, probably, the most critical ones will have to come from outside the design field.

The system that is supposed to take care of us is very sick.

To help you gauge the magnitude of the U.S. healthcare problem, let me start with some background info — it won’t hurt, I promise: This is what we pay for our healthcare in the U.S…

The U.S. 2010 healthcare expenditure was 18% of the GDP, up to $2.6 trillion. That is roughly double the OECD average and this figure is projected to grow up to 26% of GDP by 2037 (scary).

The U.S. has the highest healthcare administration costs in the World at triple the OECD average.

Cost of healthcare per capita is above $8,200. That is more than double the OECD average of $3,200. Second, but not even close, is Switzerland with $5,200.

This is what we get…

There are fewer physicians and hospital beds per person than in most other OECD countries.

Life expectancy has increased over the last few decades but less than compared to other economies. Between 1960 and 2010, 9 years compared in the U.S. to 11 years on average on OECD countries.

33% Americans were obese as of 2009 compared to an average 16% in the OECD countries.

The cost of certain procedures is much higher in the U.S. and the industry seems to favor more expensive diagnosis procedures.

In 2012, 46% of the U.S. population were underinsured or uninsured at some point, if not all year.

The system is terribly complex, especially for users: a new study to be released in September shows how only 14% of all insured Americans “can explain all four key health insurance concepts: deductible, co-pay, co-insurance, out-of-pocket maximum”. Can you?

And finally, healthcare bills is the number one reason for family bankruptcy in the U.S.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.