Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

Authors:

Jordi Gutiérrez, Domenic Kellner, Philip King, Simon Neumeyer, and Dorota Scibisz

Master’s Program:

Paper Abstract:

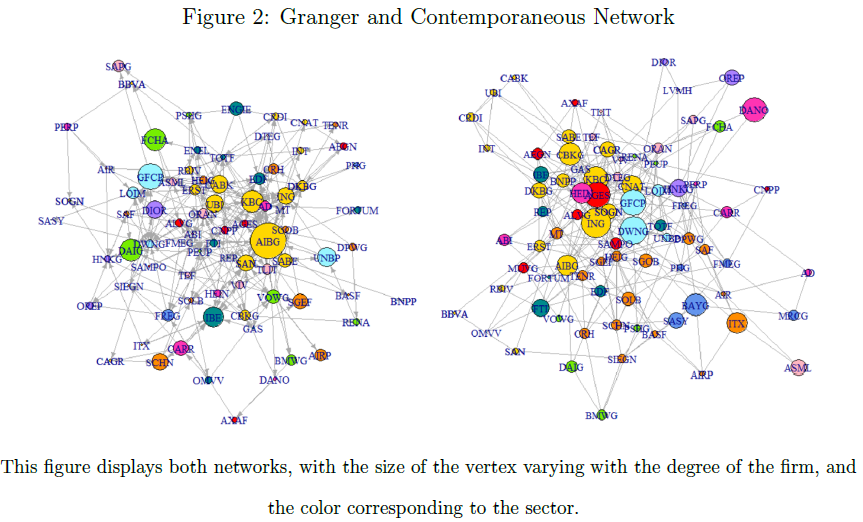

We identify contemporaneous and Granger-causal linkages between the 86 biggest companies, representing both the financial and real sectors, of the Eurozone economy that serve as paths of shock transmission. Network analysis lends itself very naturally to the study of systemic risk due to its preoccupation with interconnections and notions of centrality. We employ an estimation methodology introduced by Barigozzi and Brownlees (2018) using market data for daily volatilities from the Eurostoxx index. Our results are in line with the existing literature – the banking sector is found to be highly interconnected and responsible for most Granger-network spillovers. Moreover, only a small subset of firms appear to Granger-cause other residual volatilities, providing support for regulators’ targeting of Systemically Important Financial Institutions.

Conclusions:

Following the work of Barigozzi and Brownlees (2018), this paper applies the nets algorithm to study the interconnectedness of the 86 biggest firms in the Eurozone for a sample period spanning from May 2008 to April 2018. We have estimated two sparse networks of return volatilities that allow us to measure systemic risk and detect patterns of its transmission. Compared to the original study of the US economy, we have utilised a more detailed set of industries. What is more, country-specific volatilities were added as an extra factor in order to obtain more precise firm-specific residual volatilities, while still uncovering a large number of connections.

At the contemporaneous level almost all industries exhibit high connectedness, a pattern which became immediately apparent on the initial heatmaps of residual correlations. Even when controlling for sectoral and country volatilities we find clusters of firms reacting strongly with other firms within the same business area. These co-movements are especially remarkable within the banking, industrial, and technological sectors.

However, it is a small subset of companies, mostly financial firms, that displays high interconnectedness at the Granger-causal level. Consequently, we conclude that banks are particularly important risk transmitters in the Eurozone network. The subset of banks is especially susceptible to volatilities stemming from other sectors. This makes intuitive sense as we can think of banks being highly leveraged when compared with other entities (Freixas et al., 2015). Moreover, banks amplify and transmit shocks to all the other sectors, which reflects their unique economic role as financial intermediaries. Altogether, this provides empirical support for the regulatory targeting of certain Systemically Important Financial Institutions.

Download the full paper [pdf]

More about the Economics Program at the Barcelona Graduate School of Economics