ADBI Working Paper by Finance ’18 alumni Lavinia Franco, Ana Laura García, Vigor Husetović, and Jes Lassiter

A master project by four alumni of the Finance Program Class of 2018 is soon to be added to the working paper series of the Asian Development Bank Institute (ADBI).

Abstract

Fintech has increasingly become part of the global economy with the evolution of technology, increasing investments in fintech firms, and greater integration between traditional incumbent financial firms and fintech. Since the 2007–2009 financial crisis, research has also paid more attention to systemic risk and the impact of financial institutions on systemic risk. As fintech grows, so too should the concern about its possible impact on systemic risk. This paper analyzes two indices of public fintech firms (one for the United States and another for Europe) by computing the ∆CoVaR of the fintech firms against the financial system to measure their impact on systemic risk. Our results show that at this time fintech firms do not contribute greatly to systemic risk.

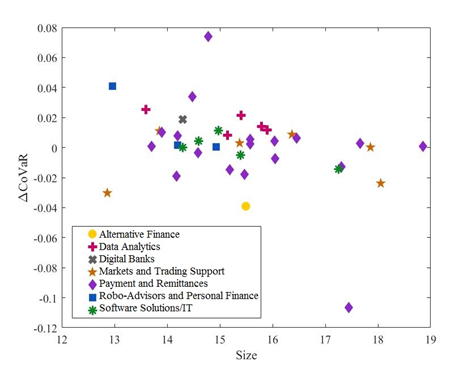

Figure B.2: US Fintech: ∆CoVaR and Size

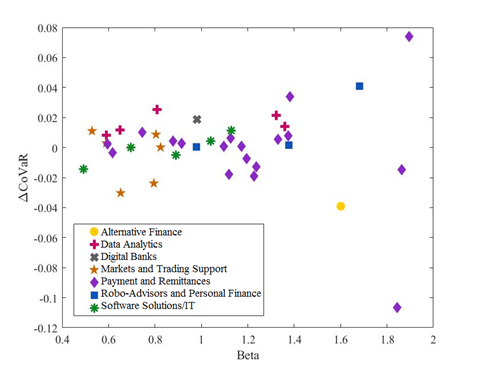

Figure B.3: US Fintech: ∆CoVaR and Beta

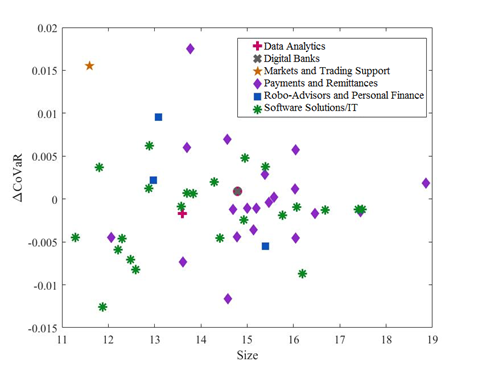

Figure B.4: European Fintech: ∆CoVaR and Size

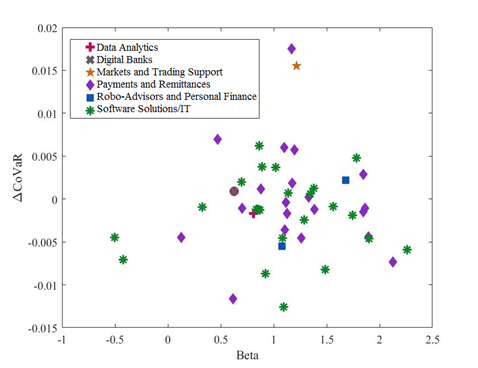

Figure B.5: European Fintech: ∆CoVaR and Beta

Conclusions and key results

Our results show that, for the US, the payment and remittances and the market and trading support categories contribute the most to the VaR of the fintech industry. Instead, in Europe, fintech firms that provide software solutions and information technologies seem to be contributing the most to the risk of the sector. The estimation that includes fintech firms and the representative sample of the financial sectors show that fintech firms are not systemically important. Within the US financial system, the fintech companies that do contribute to systemic risk increase it by around 0.03%, while, in Europe, fintech firms contribute very little to the systemic impact (close to 0%). The Spearman’s rank correlation between a fintech firm’s ∆CoVaR and its respective size and between a fintech firm’s ∆CoVaR and its beta strengthens the importance of our estimations for a better assessment of systemic risk rather than just relying on the size and the beta of the firms to determine their likely contribution to systemic risk.

Some limitations of our study include the scope of our analysis method (∆CoVaR), the representation of the fintech sector, and the analysis of only two markets. However, micro-level data analysis focusing on each individual fintech category and changing the focus on emerging markets could reveal the specific risks, highlighting key research lines.

The financial cycle plays a key role in the functioning of the economy, as we have seen in the previous articles of this Dossier. But what are the specific consequences of the relationship between the financial and business cycle? Below we analyse its implications for one of the key macrofinancial relationships: the one that exists between the financial cycle and equilibrium interest rates.

The ECB and the Fed have initiated a process to review their strategy, the results of which will be published during the course of 2020. This review has been driven by certain structural changes in advanced economies, such as the decline in the equilibrium interest rate and the flattening of the Phillips curve.

While we do not anticipate disruptive changes, it is likely that the Fed will reinforce the symmetry of its inflation target and that the ECB will adopt a similar model in order to shore up inflation expectations.

El envejecimiento poblacional será uno de los factores clave que, junto con la revolución tecnológica y el cambio climático, redefinirán nuestras sociedades en las próximas décadas. Una población más envejecida cambiará forzosamente no solo la configuración de nuestras sociedades sino también la de nuestras economías, pues el envejecimiento poblacional tiene un impacto significativo sobre el crecimiento económico. Esta es la cuestión que abordaremos en este y en los siguientes artículos del Dossier, poniendo el foco en las economías española y portuguesa.

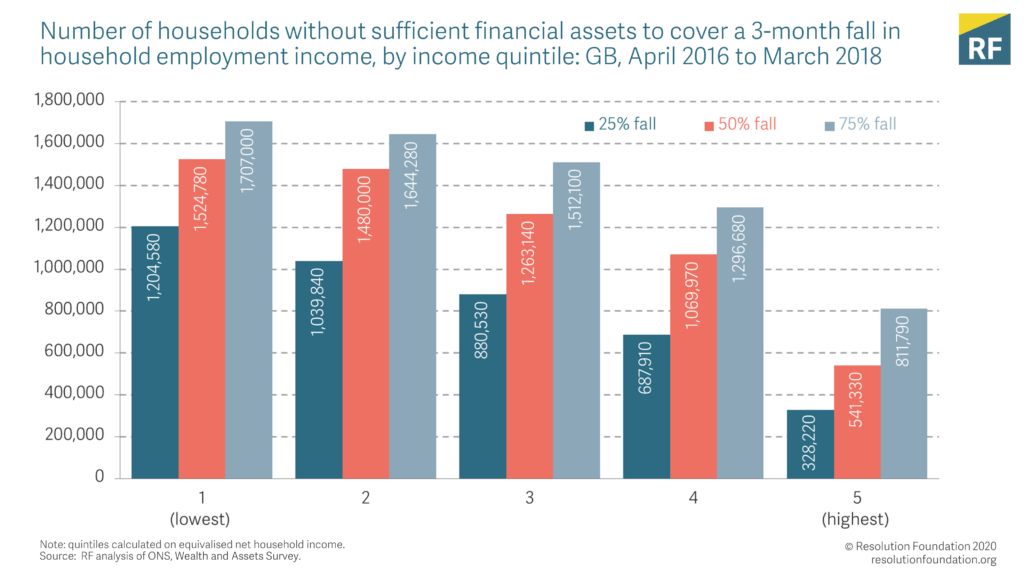

Article by George Bangham ’17 (Economics of Public Policy)

In an article for the Resolution Foundation, George Bangham ’17 (Economics of Public Policy) looks at data on UK family finances in the period before the coronavirus pandemic and thinks about policy measures for those who may lose their primary source of income during the crisis.

Here is an excerpt:

We won’t know exactly how many people have lost their jobs due to coronavirus until at least the summer, when official statistics come out. But as well as monitoring the ongoing impact of the crisis, it’s equally important to consider the state of the country as the economic downturn hit home…

Amid the horror of the pandemic, and the legitimate fears of many families for their finances, it might seem frivolous to worry about statistics for the time being. But the lessons from the data are vital. They point us to new issues that the Government must fix. In a crisis, statistics can save livelihoods and save lives.

Charlie Thompson ’14 (ITFD) has built an RStats dashboard that tracks COVID-19 cases in the United States at the county level using the latest data from The New York Times.

Check it out to see how US communities are “flattening the curve”:

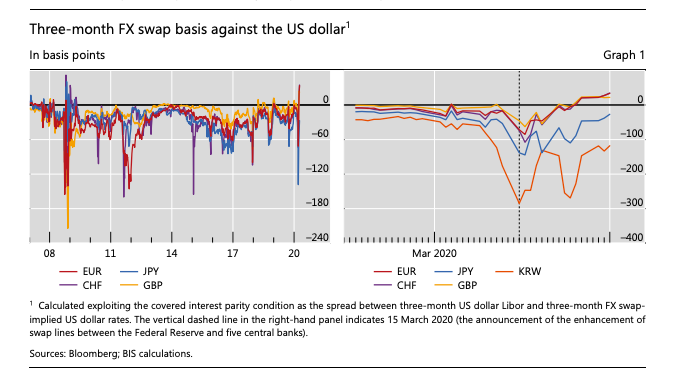

In this new publication for the Bank for International Settlements, Egemen Eren ’09 and co-authors Stefan Avdjiev and Patrick McGuire review recent events in FX swap markets in the context of the longer-term trends in the demand for dollars from institutional investors.

Key takeaways

Since the start of the Covid-19 pandemic, indicators of dollar funding costs in foreign exchange markets have risen sharply, reflecting both demand and supply factors.

The demand for dollar funding has grown in recent years, reflecting the currency hedging needs of corporates and portfolio investors outside the United States.

Against this backdrop, the financial turbulence of recent weeks has crimped the supply of dollar funding from financial intermediaries, sharply lifting indicators of dollar funding costs.

These costs have narrowed after central banks deployed dollar swap lines, but broader policy challenges remain in ensuring that dollar funding markets remain resilient and that central bank liquidity is channelled beyond the banking system.

Opinion piece by Francesco Amodio ’10 (Economics) on Canada’s response to COVID-19 crisis

In a piece published on March 31 in the Montreal Gazette, Francesco Amodio ’10 (Economics) looks at measures taken by the Canadian government in response to the coronavirus pandemic.

Here’s an excerpt:

The measures taken by the Canadian government are in line with those taken in other countries, where governments are adopting either one or the combination of the following two approaches. In the first one, the government lets firms lay off workers, then pays out employment insurance benefits or other kind of income support transfers. The second approach focuses instead on “saving jobs,” with the government subsidizing wages in order to avoid layoffs.

Each approach has its pros and cons. In the short run, the size of wage subsidies and number of potential layoffs will determine which one is costlier. Perhaps more importantly, the two approaches differ in their medium- to long-run impacts.

A displaced worker might rationally prefer to wait through a long spell of unemployment instead of seeking employment at a lower wage in a job he is not trained for. I evaluate this trade-off using micro data on displaced workers. To achieve identification, I exploit the fact that the more a worker has invested in occupation-specific human capital, the more costly it is for him to switch occupations and therefore the higher is his incentive to wait. I find that between 9% and 17% of total unemployment in the United States can be attributed to wait unemployment

Publication in Journal of Banking and Finance by Alex Hodbod (ITFD ’12) and Steffi Huber (Economics ’10, GPEFM ’17)

We have a forthcoming article “Sectoral Risk Weights and Macroprudential Policy” in the Journal of Banking & Finance with our co-author Konstantin Vasilev (Essex).

The authors!

Paper abstract

This paper analyses bank capital requirements in a general equilibrium model by evaluating the implications of different designs of such requirements regarding their impact on the tendency of banks to amplify the business cycle.

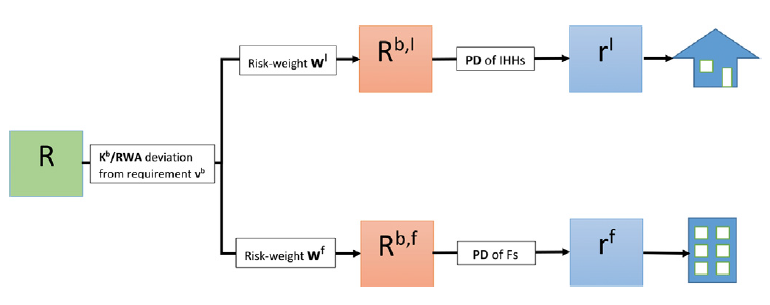

Interest rate spreads structure. This figure gives an overview of the different interest rate spreads within the model and the factors that affect them. The asset-specific interest rate spreads determine the borrowing costs of households and firms and hence the quantities of specific loan types in the economy.

We compare the Basel-established Internal Ratings-Based (IRB) approach to risk-weighting assets with an alternative macroprudential approach which sets risk-weights in response to sectoral measures of leverage. The different methods are compared in a crisis scenario, where the crisis originates from the housing market that affects the banking sector and is then transmitted to the wider economy.

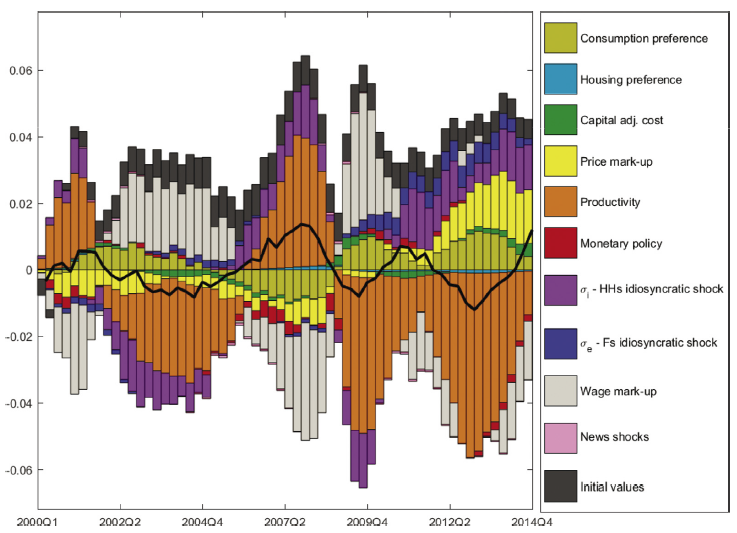

Variance decomposition – real consumption during the Great Recession. This variance decomposition shows that the model identifies the productivity shock and the shock to mortgage lending risk to be the main drivers of the crash in real consumption during the Great Recession. In our model, the main channel through which the shock to mortgage risk has a procyclical effect on consumption is through lending and house prices.

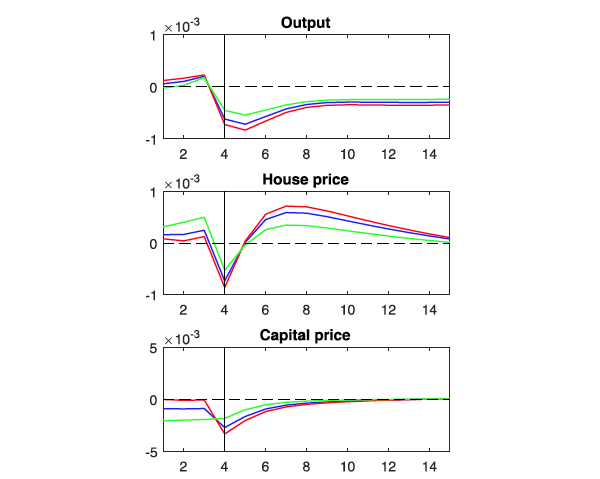

We investigate both boom and bust phases of the crisis by simulating an unrealized news shock that leads to a gradual build-up and rapid crash in the economy. Our results suggest that the IRB approach creates procyclicality in regulatory capital requirements and thereby works to amplify both boom and bust phases of the financial cycle. On the other hand, our proposed macroprudential approach to setting risk-weights leads to counter-cyclicality in regulatory capital requirements and thereby attenuates the financial cycle.

Impulse Response Function – Unrealised news shock. Here, we model both the build-up and crash phases of the crisis and use this to examine how different policy approaches perform in handling the boom phase of the cycle. In periods 1-4 agents start with expectations that a housing boom will occur, but at period 4 a shock arrives as this boom does not materialise. At the top of the chart one sees that the policy setup based on the IRB approach (red) generates the biggest macroeconomic consequences from this shock; it is the most procyclical. The macroprudential approach to risk-weighting (in green) is the least procyclical. An unweighted “leverage ratio” approach (blue) is less procyclical than the IRB approach, but more so than our macroprudential approach.

Conclusions in brief

We show that IRB risk-weights can induce procyclicality of capital requirements and amplify both boom and bust phases of the business cycle. This is particularly concerning because procyclical risk weights could undermine other macroprudential tools, as these other tools are themselves based on risk-based measures of capital requirements e.g. Counter Cyclical Capital Buffers.

Our alternative approach of macroprudential

risk weights could induce countercyclicality of capital requirements, which may

offer benefits in terms of smoothening financial cycles. Targeting

macroprudential intervention on bank risk-weights is likely to be more

effective when it is sector-specific. This will alter banks’ incentives in a

sensitive way – thereby tending to attenuate sectoral asset booms.

The results complement the ongoing debate about the potential merits of a Sectoral Counter Cyclical Capital Buffer, which is ongoing internationally.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

Forthcoming paper in Review of Economics and Statistics by Philipp Ager ’08 and Benedikt Herz ’08 (Economics)

Paper abstract

This paper provides new insights on the relationship between structural change and the fertility transition. We exploit the spread of an agricultural pest in the American South in the 1890s as plausibly exogenous variation in agricultural production to establish a causal link between earnings opportunities in agriculture and fertility. Households staying in agriculture reduced fertility because children are a normal good, while households switching to manufacturing reduced fertility because of the higher opportunity costs of raising children. The lower earnings opportunities in agriculture also decreased the value of child labor which increased schooling, consistent with a quantity-quality model of fertility.

A more in-depth summary of the paper is available in the VoxEU column “From the farm to the factory floor: How the structural transformation triggered the fertility transition.”

Philipp Ager ’08 is an Associate Professor of Economics, University of Southern Denmark and CEPR Research Affiliate. He is an alum of the Barcelona GSE Master’s in Economics.

Benedikt Herz ’08 is member of the Chief Economist’s Team, European Commission Directorate-General for Internal Market and Industry. He is an alum of the Barcelona GSE Master’s in Economics.

Jebb Peria ’10 (Finance), Associate at EV Private Equity

Jebb Peria ’10 recently answered some questions about careers in private equity in a post for his employer, EV Private Equity. Here are a few excerpts from the interview.

I’ve heard of private equity but how does it differ from, say, venture capital or fund management?

Fund management is basically a firm of money managers investing pooled funds from investors. The capital may be invested in traditional asset classes such as equities, fixed income and cash and alternative asset classes such as hedge funds, private equity, real estate, commodities and infrastructure.

Private Equity (PE) is an active form of investment in privately held companies with the objective of growing them over a medium to long-term period. As active investors, PE firms work closely with management to increase and maximise the company’s value through financial engineering, improved governance and operational performance.

At EV Private Equity, we primarily invest in early-growth companies that have: a distinct product or service; the potential to grow rapidly; low levels of debt; and experienced management teams. We seek innovative and disruptive technology companies that can scale and drive superior returns.

Venture Capital (VC) is a subset of PE which provides capital to early-stage businesses, usually in technology-based sectors. Venture capitalists normally invest in high-growth, high-risk, start-up or early-staged ventures, typically with a bias towards technology or innovation. PE tends to focus on later-stage investment in businesses that are more established and are generating cash. VC uses primarily equity while PE may use equity and debt (leverage).

Both PE and VC use a measurement known as MOIC (Multiple On Invested Capital) to calculate the returns they make from their investments. PE target returns range from 2x-5x while VC returns are expected to be higher.

Do I need an MBA from Harvard, a mathematics degree or an accountancy qualification in order to be considered?

No, not necessarily. As a matter of fact, I don’t have any of those credentials. I graduated with a BA in Economics (with highest distinction) from York University in Canada, an MA in Economics from the University of Toronto, and an MSc in Finance from Barcelona GSE. I am also a CFA® charterholder. I guess this depends on which type of PE firm you want to work with as there are generalists and specialists.

As energy specialists, our team at EV Private Equity is comprised of people with substantial experience in the energy industry [oil and gas (O&G), oil field services (OFS)] as well as those from technical disciplines (reservoir, drilling, mechanical, chemical, and software engineering as well as geophysics and naval architecture). We also recruit candidates with graduate business degrees in areas such as MBA, finance, economics, strategy etc.

Is it true that private equity is very secretive and is not accountable to any regulators or governments?

False.

EV Private Equity is regulated by the Financial Conduct Authority in the UK and the SEC in the US under the Investment Advisor Act of 1940.

Like any other firm, EV Private Equity and its portfolio companies are obliged to abide by the laws and regulations of all countries we operate in. This is also part of the fiduciary duty towards the firm’s institutional investors, comprised mainly of large public and private pension funds, insurance companies, university endowment funds and sovereign wealth funds.

What is a typical day like in private equity?

I typically start the morning reading through the latest news and market trends. I skim-through DagensNæringsliv, Bloomberg, Financial Times and even LinkedIn to check on the latest oil price, mergers and acquisitions (M&As) and geopolitical news. Then, I read through my emails to check for any updates on the portfolio companies I’m involved with and any immediate requests from the partners.

My day is normally split between fixed deliveries and ad hoc tasks. My deliveries would range from weekly meetings and operational updates with portfolio companies to monthly, quarterly and yearly financial reporting to updating fair market values of portfolio companies to weekly meetings with the digital marketing team. I would also participate in quarterly investor meetings, board meetings as well as annual strategy meetings with my portfolio companies.

If there’s a deal I am involved in, I would build the financial model, perform valuation and sensitivity analysis and support the drafting of the investment paper. I would also be participating in weekly call updates with the due diligence providers regarding any red flags and show stoppers (in other words, developments that may affect our decision to invest).

If one of my portfolio companies is preparing for an exit, I might be having calls with the management and the financial advisors discussing the potential buyers, the market sentiment and the status of the Information Memorandum (IM), the document we share with prospective buyers.

There is not much slack time. If I do have some spare time, I can always find something to work on: a process to simplify and make more efficient; a model to automate; improvements to our social media presence; or offering support to other office locations.

What are the rewards?

Helping to create value for the company and produce superior returns for investors is rewarding and gratifying.

I also get to work with different partners, management teams, board members and technologies. These teach me different insights, strategies, and management styles.

It is very rewarding to work with the smart, entrepreneurial and down-to-earth group of individuals at EV Private Equity. They make the workplace fun and invigorating.

Of course, the job is also financially rewarding. I would like to believe that I am fairly and reasonably remunerated given my performance and contributions, the skillset I bring to the table, and my dedication to my craft.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.