Alessandro Franconi ’17 (Macroeconomic Policy and Financial Markets)

In a new LUISS Working Paper, “Opening the Black Box of Austerity: Evidence from Fiscal Consolidation Plans,” Alessandro Franconi ’17 (Macro) explores the effects of austerity measures on labour markets and on income inequality and finds evidence of a mechanism that can mitigate the size of the economic contraction.

Paper abstract

This paper explores the effects of austerity measures on labour markets and on income inequality and finds evidence of a mechanism that can mitigate the size of the economic contraction. The results indicate that: (i) Fiscal consolidation causes greater distortions for the youth, hence they deserve a special attention to avoid severe long-term economic costs. (ii) While at first glance transfers cuts seem to be ideal, a careful examination suggests that these policies can jeopardise the success of fiscal consolidation. (iii) Tax hikes, negatively affecting the productive sector, trigger frictions in the labour market that give rise to recessionary effects. (iv) Spending cuts, targeting public sector wages and employment, can endanger the capabilities of the current and future labour force. (v) Lastly, income inequality increases with tax hikes and spending cuts, whereas the muted response to transfers cuts is explained by the reaction of labour demand.

A new tool created by Elliot Jones ’18 (Macro Program)

Elliot Jones ’18 (Macroeconomic Policy and Financial Markets) is a Sovereign Credit Risk Analyst at the Bank of England. Together with co-creator Jessica Golding, he has established Exploring Happiness, a research organization that looks to bring produce evidence-based research in order to generate policy recommendations focused towards sustainably increasing wellbeing across all areas of society.

The latest project to come out of the initiative is the Exploring Happiness Index. This is an online tool that anyone can use to help them achieve their goals and to support their mental health.

Learn more about the index in the video and read on to find out how to start using it:

Explaining the concept of the index

Everyone is different and what makes each of us happy is also different. Some people are career-driven, others live for the social scene and some are highly family-orientated. Despite this, we all also have a lot in common – we all value our health, both mental and physical, the quality of our personal relationships matters a lot and we all like to have something to do that makes us feel worthwhile. It is these basic fundamentals that we use to build our index. We take evidence-based research on the main determinants of life satisfaction (which is taken as being synonymous with happiness) to bring together a group of components that we all have in common and these become the building blocks of the index.

Methodology

The differences of users are captured in two main ways – by identifying the circumstances and preferences of each user. When creating an account each user can choose from 13 different individual types such as an employed worker, a student or a retired person. As a result of this choice, the components that make up the index will change to reflect that individual types circumstances (e.g. an employed worker has a ‘Work’ component, a student has an ‘Education’ component and a retired person has neither of these, but greater weight is applied to their ‘Leisure Time’ component).

Next, users are then able to choose how important each of the components are to them and the weights in the index will shift to reflect these choices. These two steps make the index unique for each user.

Being informed: Our decisions, big or small, will play an important role in determining our happiness and we are more likely to make the right decision when we have better information available to draw upon. The usage of this index provides users with this information, perhaps meaning just knowing how happy you are could make you happier.

Mental health tool: Using this index allows users time to reflect, to think about what has been going well and what has been more challenging. There is good evidence available which points to the benefits of self-reflection on mental health. This has been shown for self-reflection in a number of forms (e.g. from expressive writing to gratitude journaling), across various life stages and as an effective treatment for those with diagnosed mental illnesses. Our view, which we intend to robustly test in the future, is that the method of self-reflection that this index requires will boost users resilience and mental wellbeing.

The ultimate tracker: Nowadays, it is not uncommon to track several parts of our lives, from steps to sleep to calories. But what’s the point in tracking these things? For most people, it’s because they believe if they do more steps or sleep better, they will end up feeling better. This index allows you to check whether that’s true in practice.

VoxEU article by Manuel A. Muñoz ’13 (Macroeconomic Policy and Financial Markets)

I am honoured to share my new VoxEU article (with you), which I believe it’s relevant for the ongoing debate on how to strengthen the macroprudential regulatory framework for nonbanks:

Ensuring that institutional real estate investors are subject to countercyclical leverage limits would be particularly effective in smoothing the housing price and the credit cycle.

In addition, the associated ECB working paper suggests that this type of regulation would allow for rental housing prices to increase less abruptly during the boom, an issue that policymakers in several countries of the euro area have attempted to handle via price regulation (an alternative that could generate price distortions).

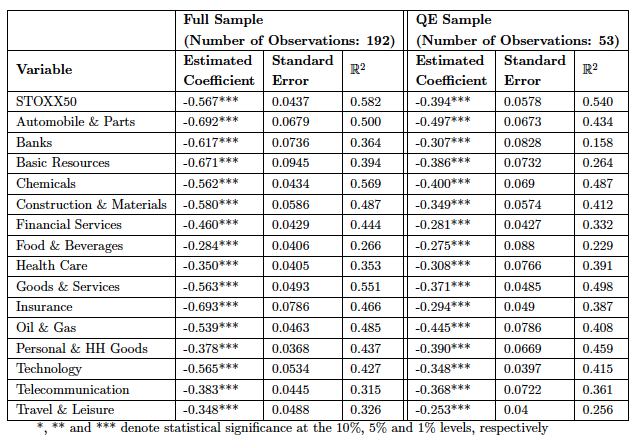

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

The Global Financial Crisis prompted central banks to adopt unconventional monetary policies such as the asset purchase programs. In our thesis, we analyze whether securities purchases carried out by the ECB have had an impact on stock prices and whether these effects vary across sectors. We decompose the central bank announcement surprises into two opposing effects, a pure monetary policy shock and an information shock. We find that the pure monetary policy shock has indeed significant effects on stock prices across all sectors, suggesting that controlling for the information shock is important when analyzing the effects of central bank announcements.

Conclusions

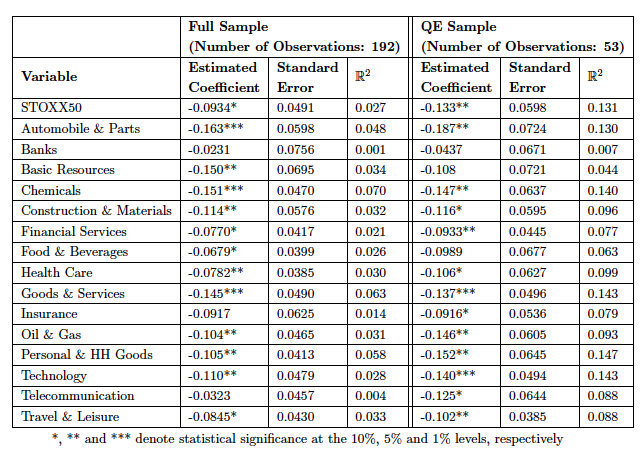

In our paper, we analyzed the effects of Quantitative Easing on stock prices in the Euro Area. Adding to previous literature, we not only analyzed the effect on the benchmark index but considered sectoral indices as well in order to allow for heterogeneous responses across different industries. Using the methodology of Altavilla et al. (2019), we first extracted the QE factor from each ECB press conference, starting from 2002. In a first exercise, we used the QE factor as a regressor to explain stock price changes on the press conference days. In line with asset pricing theory, we find negative effects of the QE shock on all sectoral stock price indices, yet, significance differs.

Overall QE Shock

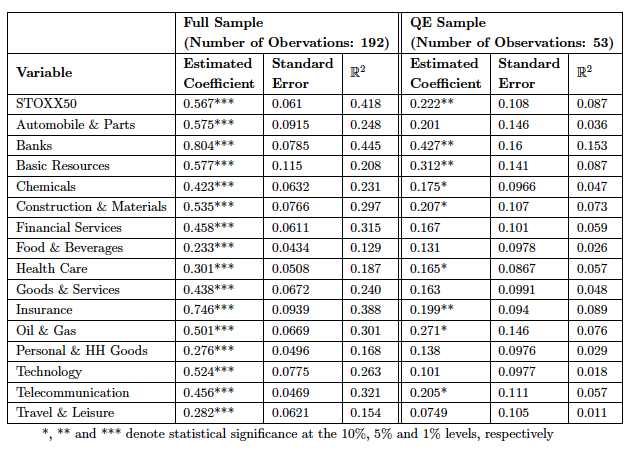

In a second step, we decomposed the shock into two components, using sign restrictions. The two shocks are referred to as information shock and pure monetary policy shock and are characterized by positive co-movement and negative co-movement of interest rates and stock prices, respectively.

Information Shock

Pure Policy Shock

We looked at these two components separately in order to assess whether insignificant results obtained in the overall regression may be due to the two components off-setting each other, a presumption which was confirmed. Furthermore, we find that the pure monetary policy shock has significant effects on stock prices across all sectors, while the information shock appears to be more important on specific sectors, which are more related to financial markets. A more in-depth analysis of the reasons for this heterogeneity could provide further insight into the effects of QE on stock prices. Moreover, repeating this exercise with a larger sample and intraday stock price data might yield improved results. Other extensions could be the analysis of specific sectors for various countries.

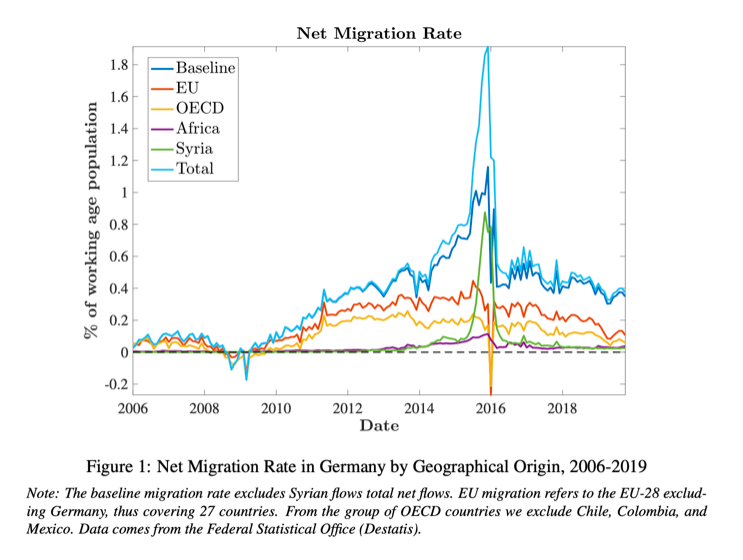

Working Paper by Nicolò Maffei Faccioli (Macro ’15 and IDEA) and Eugenia Vella (Sheffield)

What is the macroeconomic impact of migration in the second-largest destination for migrants after the United States?

In this paper, we uncover new evidence on the macroeconomic effects of net migration shocks in Germany using monthly data from 2006 to 2019 and a variety of identification strategies in a structural vector autoregression (SVAR). In addition, we use quarterly data in a mixed-frequency SVAR.

While a large literature has analyzed the impact of immigration on employment and wages using disaggregate data, the migration literature in the context of macroeconometric models is still limited due to a lack of data at high frequency. Interestingly, such data is available for Germany. The Federal Statistical Office (Destatis) has been collecting monthly data on the arrivals of foreigners by country of origin on the basis of population registers at the municipal level since 2006. The figure below shows the net migration rate by origin.

Key takeaways

Migration shocks are persistently expansionary, increasing industrial production, per capita GDP, investment, net exports and tax revenue.

Our analysis disentangles the positive effect on inflation of job-related migration from OECD countries from the negative effect of migration (including refugees) from less advanced economies. In the former case, a demand effect seems prevalent while in the latter case, where migration is predominantly low-skilled and often political in nature (including refugees), a supply effect prevails.

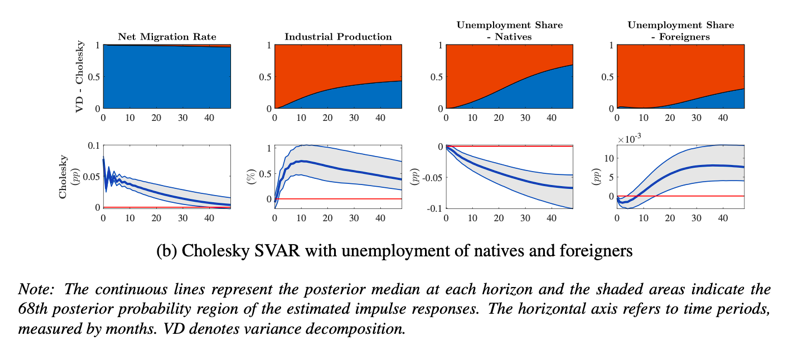

In the labor market, migration shocks boost job openings and hourly wages. Unemployment falls for natives, driving a decline in total unemployment, while it rises for foreigners (see figure below). Interestingly, migration shocks (blue area in the first row) play a relevant role in explaining fluctuations in industrial production and unemployment of both natives and foreigners, despite the bulk of these being explained by other shocks (red area in the first row), like business cycle and domestic labor supply.

We also shed light on the employment and participation responses for natives and foreigners. Taken together, our results highlight a job-creation effect for natives and a job-competition effect for foreigners.

Conclusion

The COVID-19 recession may trigger an increase in migration flows and exacerbate xenophobic sentiments around the world. This paper contributes to a better understanding of the migration effects in the labor market and the macroeconomy, which is crucial for migration policy design and to curb the rise in xenophobic movements.

Niccolò Maffei-Faccioli ’15 (Macroeconomic Policy and Financial Markets) is a PhD candidate in Economics at Universitat Autònoma de Barcelona and Barcelona GSE (IDEA).

Maximilian and Elliot connected through social media due to the Barcelona GSE connection and started working together on this piece due to shared research interests.

The COVID-19 pandemic is changing the way that we live our lives. As time passes it is becoming apparent that even once the lockdown policies have been eased and some level of normality has been resumed, the new world that we live in will be different to the one we knew before. This article focuses on emerging trends within the UK that have largely taken place as a result of COVID-19, or in some cases the pandemic has simply accelerated a trend that was already occurring. We then look to offer a range of public policy solutions for the recovery period where the overarching objective is to increase wellbeing in society in a sustainable way. These are focused towards the UK but several could be paralleled to other advanced economies.

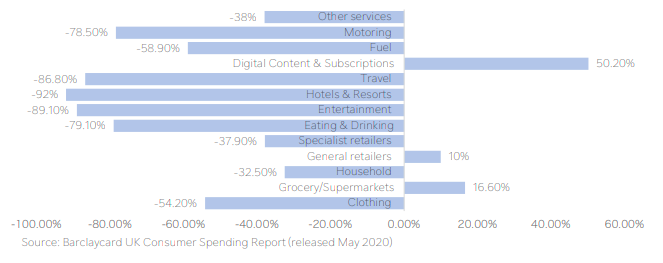

Chart 1. Consumer spending in April 2020 by category, % change year-on-year

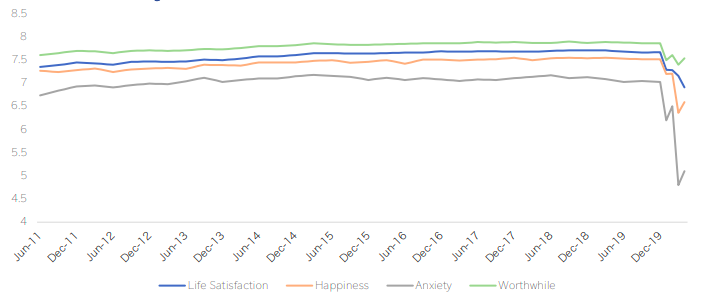

But first, before we get to the policy solutions, briefly, what have been the main economic and wellbeing effects that we have seen as a result of COVID-19? In 2020, it is expected that the fall in overall economic output is going to be larger than during the financial crisis in 2008. Much of this is due to the level of decline in economic activity as a result of the UK governments lockdown policy. This was a necessary decision in order to reduce the spread of the virus and ensure the health service still has capacity to treat those that have unfortunately caught the disease. However, it has led to a significant liquidity shock for both households and businesses. Large portions of the labour market are now out of work and levels of consumer spending have declined rapidly (Chart 1). Alongside sharp falls in measures of economic performance, measures of wellbeing have declined rapidly as well (Chart 2). Increases in measures of uncertainty have mirrored increases in anxiety. While, social distancing policies are having a large impact on measures of happiness.

Chart 2. ONS wellbeing measures (2011-2020)

Source: ONS. Notes: Each of these questions is answered on a scale of 0 to 10, where 0 is “not at all” and 10 is “completely”. Question: “Overall, how satisfied are you with your life nowadays?”, “Overall, to what extent do you feel that the things you do in your life are worthwhile?”, “Overall, how happy did you feel yesterday?”, “Overall, how anxious did you feel yesterday?”.

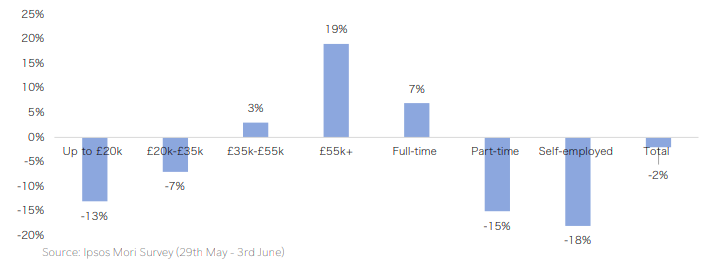

The UK government responded to the shock posed by COVID-19 with a range of policy interventions to provide funding to those that have been most impacted. At a macro level, the long-lasting effects of this crisis will be more pertinent if economic activity does not respond quickly after the government’s schemes have ended. Large portions of UK businesses have limited cash reserves to fall back on in a scenario where demand remains subdued for some time. However, even if the recovery period is strong there will still have been some clear winners and losers during this crisis. Younger workers, those on lower incomes and those with atypical work contracts are the ones that have been most heavily impacted (Chart 3). Whilst those on higher incomes, that are more likely to be able to work from home, have increased their household savings during this period, due to less opportunities to consume.

Chart 3. Impact of COVID-19 on household savings by income and employment type

The policy solutions outlined below aim to be complementary of one another and look to amplify observed trends that are positive for wellbeing and to provide intervention where trends have been negative for wellbeing:

Climate at the centre of the response: This is less a policy recommendation and more a theme for the response. However, our message here is that increased public spending projects, focused towards green initiatives should be combined with a coherent carbon tax policy which influences incentives and helps to support the UK’s transition to a low carbon economy.

Labour market reforms: The government should look to develop a centralised job retraining and job matching scheme that supports workers most impacted by COVID-19, helps to encourage structural transformation towards emerging industries and increases the amount of highly skilled workers in the UK workforce.

Tough decisions on business: Some businesses will require further assistance from the UK government in the form of equity funding, rather than the debt funding seen so far. This should be done on a conditional basis, requiring all these businesses to comply with the UK’s climate objectives and should only be provided to businesses in industries that are expanding or strategically important to the UK economy.

Modernising the regions on a cleaner, greener and higher level: Looking to build on the governments ‘levelling up the regions’ policy to reduce regional inequalities, our policy consists of government funded infrastructure policies that include green investments for regions outside of the UK’s capital.

Harbouring that rainbow effect: Building on the increased community spirit that has been observed during the pandemic, this policy solution looks to increase localised community funding to maintain social cohesion and support those with mental health issues.

Lastly, as the policy recommendations focus on expanding public investment to support the recovery, it is important to consider what this means for public debt sustainability in the UK. The conclusion is that as a result of the low interest rate environment, the most efficient way out of this recession is to borrow and spend on projects that will increase resilience to future shocks and support the UK’s transition to a low carbon economy.

Please click on the link below to read about this in more detail. Comments are welcome.

Alessandro Franconi ’17 (Macroeconomic Policy and Financial Markets)

“Mini-Bot: Ingenuity or Ignorance” is my first policy brief for the Luiss School of European Political Economy.

“The concept of using mini-BOTs to pay off trade payables may seem like a good idea, but if we analyze it in detail we can intuitively conclude that such a tool is futile and limited…It is clear that the mini-BOTs are a completely sterile, if not harmful, device for public finances, as their implementation (or just the information that the government is officially studying their implementation) would put again Italy on the road to leaving the euro.

Publication by Nataša T. Jemec ’09 (Economics) and Ludmila Fadejeva ’11 (Macro)

Nataša Todorović Jemec ’09 (Economics) and Ludmila Fadejeva ’11 (Macroeconomic Policy and Financial Markets) have published a paper in the IZA Journal of Labour Policy, together with a few other colleagues from central banks of new EU member states. The paper, “How do firms adjust to rises in the minimum wage?Survey evidence from Central and Eastern Europe,” studies the transmission channels for rises in the minimum wage using a unique firm-level dataset from eight Central and Eastern European countries.

They wrote the publication within the ECB Wage Dynamics Network (WDN). At the time, Nataša and Ludmila were working at the Central Bank of Slovenia and the Central Bank of Latvia respectively, and they were their banks’ representatives in the WDN. Increase of the minimum wage was a common topic of many new EU members, and they decided to write a paper on that based on the data that they collected through a WDN survey in their countries.

Researchers can use this form to request access to the data of the WDN network which includes many EU countries.

Paper abstract

We study the transmission channels for rises in the minimum wage using a unique firm-level dataset from eight Central and Eastern European countries. Representative samples of firms in each country were asked to evaluate the relevance of a wide range of adjustment channels following specific instances of rises in the minimum wage during the recent post-crisis period. The paper adds to the rest of literature by presenting the reactions of firms as a combination of strategies and evaluates the relative importance of those strategies. Our findings suggest that the most popular adjustment channels are cuts in non-labour costs, rises in product prices, and improvements in productivity. Cuts in employment are less popular and occur mostly through reduced hiring rather than direct layoffs. Our study also provides evidence of potential spillover effects that rises in the minimum wage can have on firms without minimum wage workers.

Macroeconomic master project by Ivana Ganeva and Rana Mohie ’19

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Introduction

The question of whether a currency crisis can be predicted beforehand has been discussed in the literature for decades. Economists and econometricians have been trying to develop different prediction models that can work as an Early Warning System (EWS) for a currency crisis. The significance of such systems is that they provide policy makers with a valuable tool to aid them in tackling economic issues or speculation pressure, and in taking decisions that would prevent that from turning into a crisis. This topic is especially relevant to Emerging Markets Economies due to the presence of a greater number of fluctuations in their exchange rate translating to a bigger currency crisis risk.

In this paper, we propose an Early Warning System for predicting currency crises that is based on an Artificial Neural Networks (ANN) algorithm. The performance of this EWS is then evaluated both in-sample and out-of-sample using a data set of 17 developed and developing countries over the period of 1980-2019. The performance of this Neural-Network-based EWS is then compared to two other models that are widely used in the literature. The first one is the Probit model dependent variable which is considered the standard model in predicting currency crises, and is based on Berg and Patillo, 1999. The second model under consideration is a regime switching prediction model based on that proposed by Abiad, 2006.

Artificial Neural Networks

Artificial Neural Networks (ANN-s) is a Machine Learning technique which drives its inspiration from biological nervous systems and the (human) brain structure. With recent advancement in the computing technologies, computer scientists were able to mimic the brain functionality using artificial algorithms. This has motivated researchers to use the same brain functionality to design algorithms that can solve complex and non-linear problems. As a result, ANN-s have become a source of inspiration for a large number of techniques across a vast variety of fields. The main financial areas where ANN-s are utilized include credit authorisation and screening, financial and economic forecasting, fixed income investments, and prediction of default and bankruptcy and credit card manipulations (Öztemel, 2003).

Main Contributions

1. Machine Learning Techniques:

(a) Using an Artificial Neural Network predictive model based on the multi-layered feed forward neural network (MLFN), also known as the “Back-propagation Network” which is one of the most widely used architectures in the financial series neural network literature (Aydin and Savdar 2015). To the best of our knowledge, this is the first study that used a purely neural network model in forecasting currency crises.

(b) Improving the forecast performance of the Neural Network model by allowing the model to be trained (learn) from the data of other countries in the cluster; i.e countries with similar traits and nominal exchange rate depreciation properties. The idea behind this model extension is mainly adopted from the “Transferred Learning” technique that is used in image recognition applications.

2. The Data Set: Comparing models across a large data set of 17 countries in 5 continents, and including both developing and developed economies.

3. Crisis Definition: Adding an extra step to the Early Warning System design by clustering the set of countries into 6 clusters based on their economy’s traits, and the behavior of their nominal exchange rate depreciation fluctuations. This allows for having a crisis definition that is uniquely based on each set of countries properties – we call it the ’middle-ground’ definition. Moreover, this allowed to test for the potential of improving the forecasting performance of the neural network by training the model on data sets of other countries within the same cluster. 4. Reproducible Research: Downloading and Cleaning Data has been automated, so that the results can be easily updated or extended.

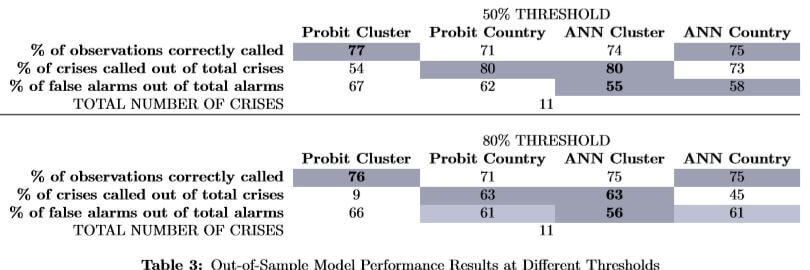

Conclusions

We compare between models based on two main measures. The Good Signals measure captures the percentage of currency crises predicted out of the total crises that actually occurred in the data set. The second measure used for comparing across models is the False Alarms measure. That is, the percentage of false signals that the EWS gives out of the total number of crises it predicts. In other words, that is the percentage of times when the EWS predicts a crisis that never happens.

The tables presented below show our findings and how the models perform against each other on our data set of 17 countries. We also provide the relevant findings from literature as a benchmark for our research.

The results in Table 1 show that Berg & Patillo’s clustering of all countries together generally works worse than our way of clustering data. Therefore, we can confirm that the choice of a ’middle-ground’ crisis definition has indeed helped us preserve any potential important country- or cluster-specific traits. In brief, we get comparable results to the ones found in the literature when using conventional methods, as highlighted by the table to follow.

After introducing the ANN model and its extension, we observe their Out-of-Sample models performance and obtain some of the key results to our research.

Summary of the key results

The proposed Artificial Neural Network model crisis predictability is shown to be comparable to the standard currency crisis forecasting model across both measures of Good Signals and less False Alarms. However, the modified Neural Network model on the special clustering data set has shown superior performance to the standard forecasting model.

The performance of the Artificial Neural Network model observed a tangible improvement when introducing our method of clustering the data. That is, data from similar countries as part of the training set of the network could indeed serve as an advantage rather than a distortion. To the contrary, using the standard Probit model with the panels of clustered data resulted in lower performance as compared to the respective country-by-country measures.

It’s our second roundup of articles by Barcelona GSE Alumni who are now working as research assistants and economists at CaixaBank Research in Barcelona (see Vol. 1).

This roundup includes posts and videos from the second half of 2018 and early 2019, listed in reverse chronological order. Click each author’s name to view all of his or her articles from CaixaBank Research in English, Catalan, and Spanish.

Ricard Murillo ’17 (International Trade, Finance, and Development)

The importance of education for people’s well-being throughout all stages of their lives is beyond any doubt. At the economic level, individuals with higher levels of education tend to enjoy higher employment rates and income levels. What is more, all the indicators suggest that in the years to come, the role of education will be even more important. The challenges posed by technological change and globalisation have a profound effect on the educational model.

Faced with the major transformation of the productive system brought about by technological change and globalisation, as well as the challenges posed by an ageing population, it is important to take action to strengthen social cohesion – an indispensable element if we are to carry out reforms that foster an inclusive and sustained form of growth.

The US and the euro area are at different stages of their financial cycles: while the Fed’s monetary policy is close to becoming neutral or even restrictive, the ECB remains in clearly accommodative territory. However, to some extent, both are facing a common risk: the decoupling between their monetary policy and the financial conditions. The two institutions will try to manage their tools carefully, in order to facilitate a gradual adjustment of the financial conditions in the US and, in the case of the euro area, to keep them in accommodative territory.

Gerard Arqué ’09 (Macroeconomic Policy and Financial Markets)

Thanks to the implementation of the measures introduced following the financial crisis, today the financial sector is more robust than before. This will help to minimise the impact to the economy and financial stability in periods of upheaval, since countries with better-capitalised banking systems tend to experience shorter recessions and less contraction in the supply of credit. However, the outstanding tasks we have mentioned should be properly addressed sooner rather than later.

Central banks are facing the challenge of removing the extraordinary measures imposed during the financial crisis of 2007-2008 and the subsequent economic recession. In normal times, central banks would simply raise interest rates up to the desired level. However, monetary policy is currently in a rather unconventional cycle.

If you’re an alum and you’re also writing about Economics, let us know where we can find your stuff!

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.