Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

Authors:

Sybrand Brekelmans, Guillermo Sanz Marin, and Luca Tomassetti

Master’s Program:

Macroeconomic Policy and Financial Markets

Paper Abstract:

In this paper we study the dynamics and drivers of 10 year’s sovereign bond yields using a panel of the original 11 Eurozone countries (excluding Luxembourg). The interest of this study relies on the fact that despite very different macroeconomic policy stances in the variables that we believe determine interest rates among these countries, 10 years Eurozone bond yields almost perfectly converged during the 2000’s, before they suffered a sudden disconnection in the aftermath of the Great Financial Crisis.

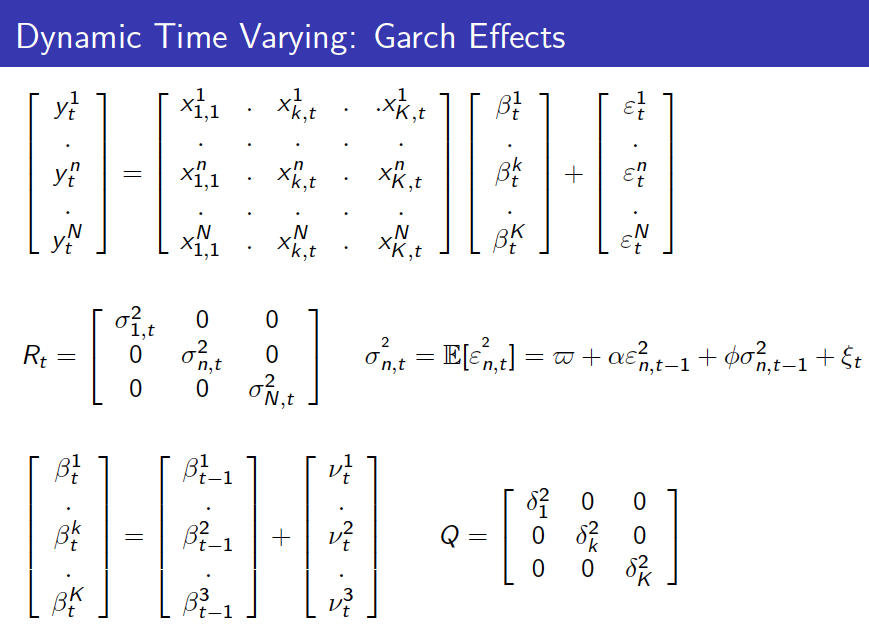

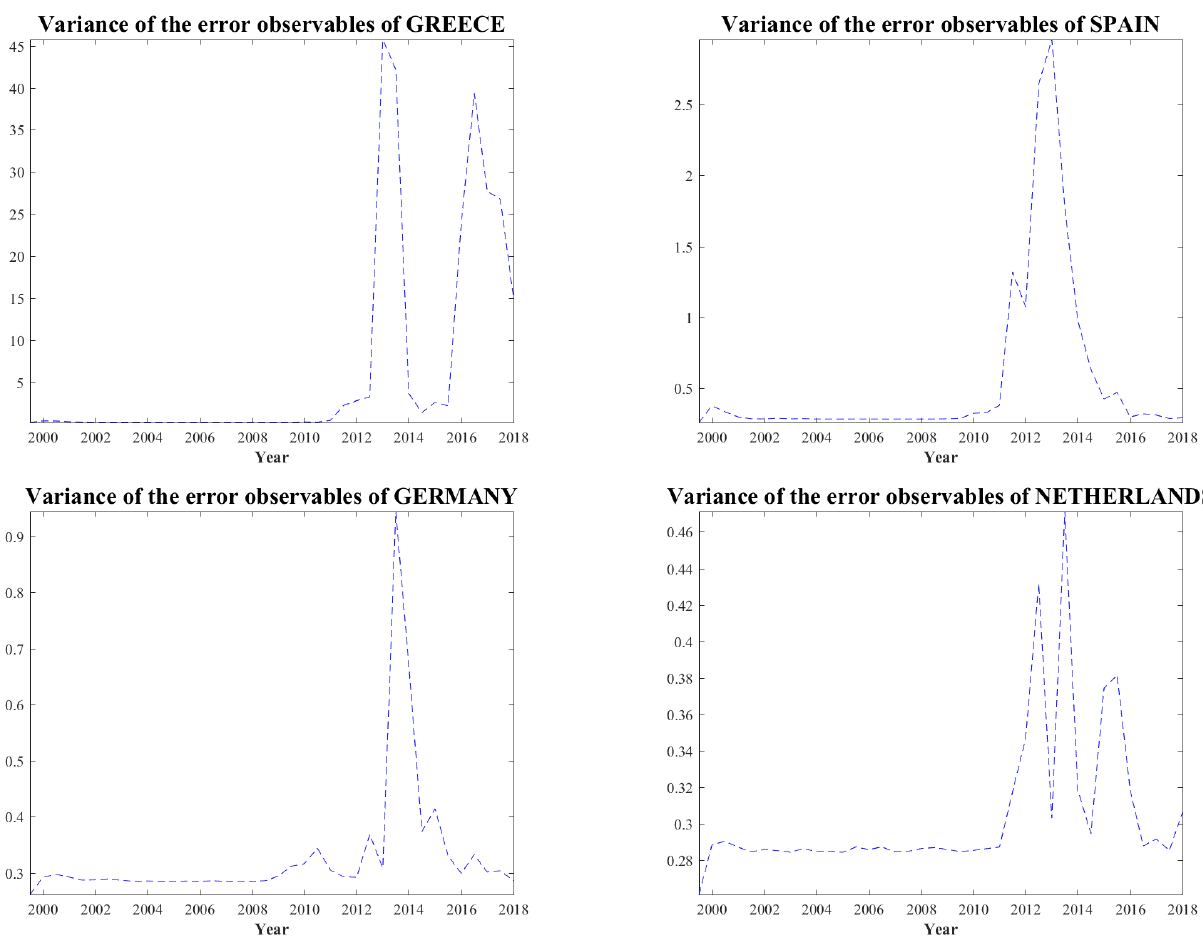

To this end, we apply two different methodologies. A Panel Data approach (that we end discarding) and a Time Varying Coefficients model using the Kalman Filter, which allows us for capturing changes in the pricing mechanism of bond yields over time. Initially, by using the latter methodology without controlling for the volatility of the interest rates (which dramatically increased after 2008), we obtain very noisy results that are barely explainable, since the coefficients seem to be capturing these changes in volatility. Once we introduce in the filter a GARCH process for the variance-covariance matrix of the interest rates that we use in the Time Varying Coefficients approach, we manage to obtain much more meaningful and explicative results.

One of our key contributions is the inclusion of new fiscal and macroeconomic variables as determinants of yields in the different Eurozone countries, which were discarded by other studies in the field. We also contribute by controlling by common determinants to all the Eurozone countries, which we obtained by applying a common component approach. Furthermore, our findings confirm that after the period of divergence in interest rates, started in the aftermath of the Great Financial Crisis, and caused by a refocus on fundamentals, Eurozone interest rates have converged again under the effect of a normalization of bond yield drivers, similarly to their pre-crisis levels, although not to the same extent. Another implication that we find is that in times of economic uncertainty and financial hysteresis, when default risk becomes an issue, the effects of government policy on interest rates can significantly lead to accentuated crowding out effects.

Conclusions and key results:

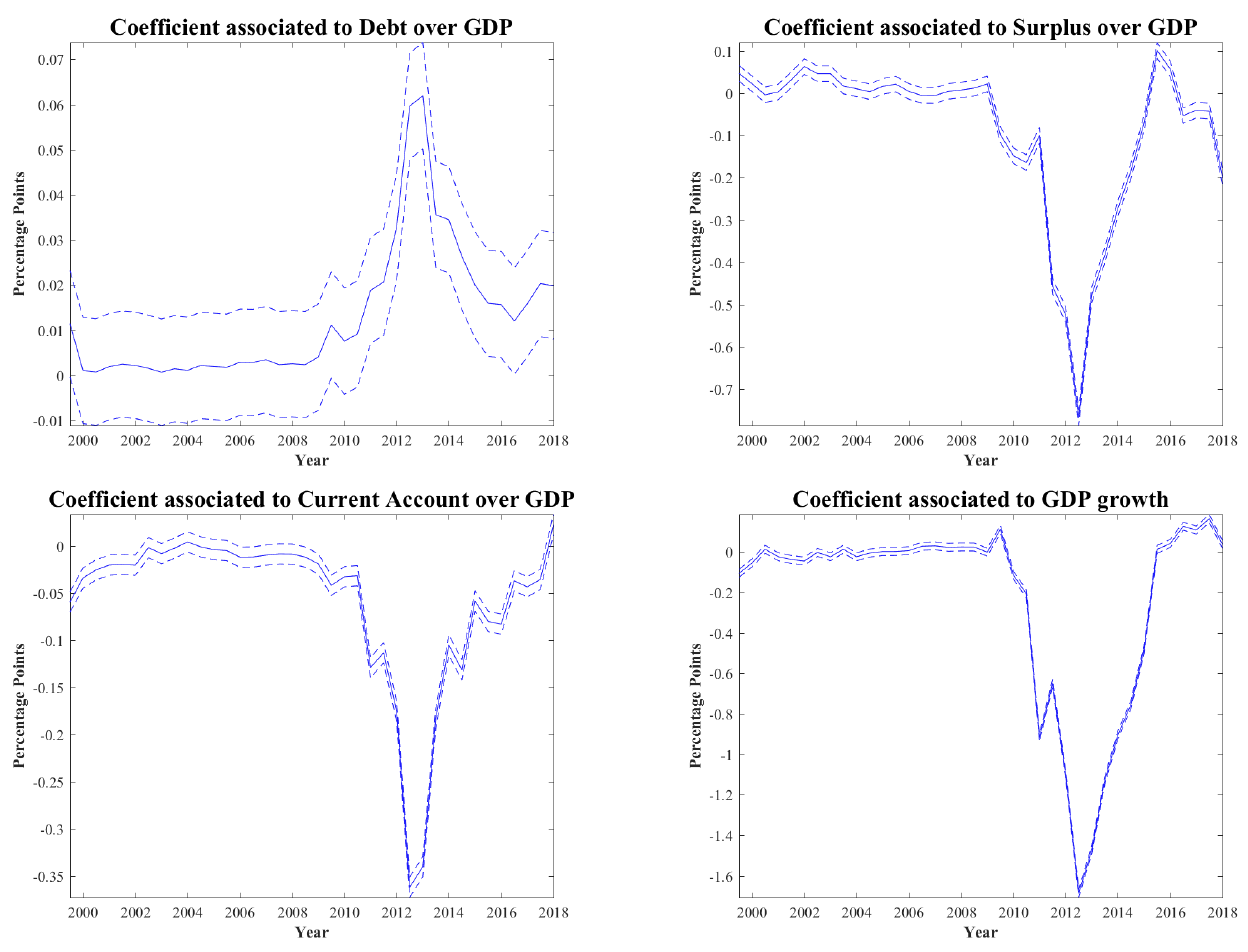

Our work indicates that there has been a significant break in the way sovereign debt was priced after the Great Financial Crisis of 2008, indicating a return to fundamentals as main drivers of sovereign yields. We find that several factors reflective of fiscal and macroeconomic stances became increasingly important during the crisis, after having been ignored in previous years. As such, Debt to GDP, Deficit to GDP, GDP growth and Current Account balances to GDP, among others, started to play important roles in the determination of long term interest rates for Eurozone government bonds. In line with previous research, our findings confirm the existence of 3 distinct phases in the euro bond market. A period of high integration, a period of disintegration, and a phase of partial reintegration (Adam and Lo Duca (2017)).

Our findings suggest that during periods of economic uncertainty characterized by high volatility in the financial markets, investors tend to focus on fundamentals, while in times of economic boom they do not discriminate too much among the different stance of these macroeconomic determinants. This finding has important policy implications since it suggests that during economic crises interest rates react much more to unsustainable fiscal policies and macroeconomic imbalances than during calmer times, causing a great private sector crowding out effect (Laubach (2011)).

Therefore, our results suggest that governments should pay closer attention to their fiscal stances during times of economic turbulence in order to avoid the detrimental effects of high interest rates on activity in a period of economic agent´s lack of confidence. As argued before by De Grauwe and Ji (2013), this former effect is exacerbated by the fact that Eurozone governments have no control over monetary policy, making impossible for them to reduce interest rates by no other means than sound fiscal policies. In line with this result, we notice that the ECB’s unconventional monetary policy (we obtain that the impact of short term interest rates -one of our common determinants obtained by principal components- on long yields has diminished over time) helped to bring down European bond yields after 2014. This fact contributed to put the fiscal stances of these countries, and other essential macroeconomic variables, back to sustainable levels, that along with the structural reforms carried out (which in addition to the former effect, have also contributed to bring back economic confidence and dynamism) have had by its own another loosening impact in the interest rates that these countries have been facing in every debt issuance.

Regarding the methodologies used to address our research question, we were able to obtain robust results and determine which method was the most appropriate to investigate the drivers of 10 year’s sovereign bond yields. We found that panel data approaches, which are widely used in the literature, lead to unstable and unsatisfactory results, causing us to attach limited credibility to the outcomes of such analysis. However, the Time Varying Coefficients approach seems more reliable and yields more robust and plausible results after we model the changes in volatility appropriately. We believe that having a larger sample (we use the forecasts released twice a year by the IMF in its World Economic Outlook and by the OECD in their Economic Outlook in order to control by the effect of the market´s forward looking in current levels of interest rates, as well as by reverse causality) would have allowed us to obtain more reliable results on this approach as well.

A suggestion for further research would be to apply Bayesian techniques to estimate our model. Indeed, given the limited amount of data available and the complexity of our models, these methods seem to suit better in this kind of estimation, where the great amount of parameters, as well as the possible presence of non-linearities, can make the optimization process very costly. Consequently, this methodology would have allowed us to also model the variance of the Time Varying Parameters, and not only the ones of the interest rates (our observables) with another GARCH or stochastic volatility process, since we expect that these variances could also follow a conditional process, which might have an impact on our estimation results.

Download the full paper [pdf]

More about the Macro Program at the Barcelona Graduate School of Economics