Steffi gave an interview to CEPR’s Tim Phillips about the team’s research:

Policies to avoid zombification of the economy

In an accompanying VoxEU column, the authors discuss the risks that government responses to COVID-19 could “zombify” the economy.

“A representative consumer survey in five EU countries indicates that many consumers do not miss certain goods and services they have cut down on since the COVID-19 outbreak,” the authors explain in their column. “Fiscal policy must recognise that some firms will become obsolete in the altered post-COVID-19 environment. To achieve a swift recovery, these obsolete firms must be allowed to fail fast so that resources can be reallocated to more efficient uses. Instead, fiscal support should be laser-like in targeting those households who are particularly hard hit by the crisis. Such support should be oriented towards helping displaced workers retrain and find new jobs.”

Prospective economic developments depend on the behavior of consumer spending. A key question is whether private expenditures recover once social distancing restrictions are lifted or whether the COVID-19 crisis has a sustained impact on consumer confidence, preferences, and, hence, spending. Changes in consumer behavior may not be temporary, as they may reflect long-term changes in attitudes arising from the COVID-19 experience. This paper uses data from a representative consumer survey in five European countries conducted in summer 2020, after the release of the first wave’s lockdown restrictions. We document the underlying reasons for households’ reduction in consumption in five key sectors: tourism, hospitality, services, retail, and public transports. We identify a large confidence shock in the Southern European countries and a permanent shift in consumer preferences in the Northern European countries. Our results suggest that horizontal fiscal support to all firms risks creating zombie firms and would hinder necessary structural changes to the economy.

Alexander Hodbod ’12 (International Trade, Finance, and Development). Counsellor to ECB Representative to the Supervisory Board, European Central Bank (DGSGO-SO), Frankfurt, Germany.

Cars Hommes. Professor of Economic Dynamics at CeNDEF, Amsterdam School of Economics, University of Amsterdam, and research fellow of the Tinbergen Institute, Amsterdam, The Netherlands, Senior Research Director (Financial Markets Department), Bank of Canada.

Stefanie J. Huber ’10 (Economics). Assistant Professor at CeNDEF, Amsterdam School of Economics, University of Amsterdam, and research candidate fellow of the Tinbergen Institute, Amsterdam, The Netherlands.

Isabelle Salle. Principal Researcher at the Bank of Canada (Financial Markets Department), research fellow at the Amsterdam School of Economics, University of Amsterdam, and research fellow of the Tinbergen Institute, Amsterdam, The Netherlands.

BIS Bulletin by Sebastian Doerr ’13 (Economics) and Leonardo Gambacorta

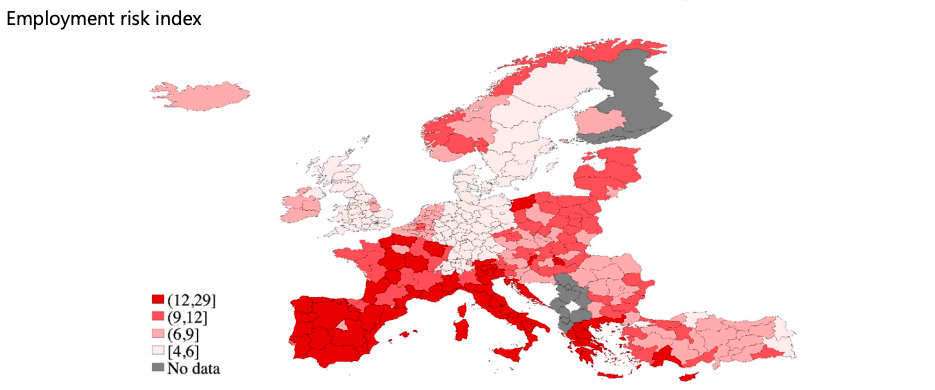

The outbreak of Covid-19 and the ensuing measures to contain the pandemic have brought Europe into a deep downturn. GDP is expected to drop by around 8% in the euro area this year (ECB (2020)), a significantly steeper decline than forecasted for the United States or Asia (IMF (2020)). One of the major reasons why the European economy is expected to be so hard-hit is its high share of small firms, especially in southern and eastern European countries. Small firms are financially more constrained and bank-dependent than larger firms. They also sell goods predominantly in local markets and with less diversified sources of revenue.

This Bulletin investigates which European regions face higher risks to employment from Covid-19. We first use data on local industry-level employment before the outbreak and construct a measure of local employment exposure to Covid-19, using the methodology developed in Doerr and Gambacorta (2020) for the US. We then extend the analysis by taking into account the share of employment among small firms in different regions. Specifically, we calculate an employment risk index based on the interaction of sectoral exposure and the share of small business employment. Our results show that while several European regions employ a high share of people in sectors particularly exposed to the economic consequences of the pandemic, the high share of small firms in southern Europe puts employment in those regions particularly at risk. We show that regions with a higher employment risk index, ie those with higher sectoral exposure and a higher share of small businesses, also exhibit a stronger increase in Google searches for unemployment, providing a cross-check of our measure of local employment risk.

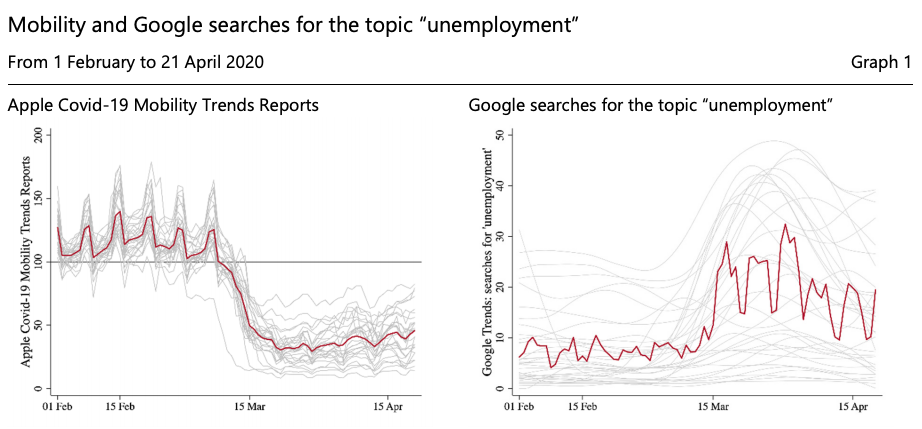

The left-hand panel shows the evolution of Apple Covid-19 Mobility Trends Reports from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). The index is averaged across all subcategories. The Mobility Trends index reflects requests for directions in Apple Maps and is standardised to 100 on 13 January 2020. The right-hand panel shows the relative frequency of Google searches for the topic “unemployment” from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). For illustration, country-specific lines are Hodrick Prescott-filtered trend components with a smoothing parameter of 500.

Sources: Apple Covid-19 Mobility Trends Reports; Google Trends; authors’ calculations.

Key takeaways

We construct employment risk indices for European regions that reflect the share of jobs under threat from Covid-19. The risk index is based on local employment in sectors that are more exposed to the pandemic and on the regional incidence of small firms.

Employment in regions in southern Europe and France is shown to have high risk indices, while regions in northern Europe have lower risk indices. Eastern and central European regions have intermediate risk indices.

Regions with a higher risk index have a bigger jump in Google searches for unemployment-related terms.

The challenge for the EU is to deliver a policy response that reduces, not exacerbates differences. This requires a level playing field (e.g. for state aids) and a high degree of coordination.

In my all-time favourite book ‘Antifragile’, Nassim Taleb divides the world into 3 categories- fragile, robust and antifragile. He refers to fragility as the state of being that involves avoiding disorder and disruption for fear of the mess that threatens to disrupt your life: you think you are keeping safe, but really you are making yourself vulnerable to the shock that will tear everything apart. Robustness is the ability to stand up to shocks without flinching, without changing who you are. But you are antifragile if shocks make you better able to adapt to each new challenge you face. You are antifragile if you can opportune from disruptions, to be stronger and more creative. Taleb thinks we should all try to be antifragile!

On March 11, 2020, declared a world pandemic, the COVID-19, is an epitome of the chaotic disruption Taleb was referring to. The onset of this crisis got me pondering whether populations, institutions, financial bodies, governments and policy-makers -i.e. the world as a whole will be able to be resilient in the face of the aftermath of this crisis? Do we have the acceptance, courage and strength besides the technical, innovative and problem-solving skills to start afresh and turn this disequilibrium around into the most memorable salvation story we have ever seen? Or will we succumb to this dooming, seemingly apocalyptic spiral, and lose everything we take for granted in our day-to-day lives? When the noise of this unprecedented shock dies, will we be left at the inception of a brand new system that will push us to rethink policies, and rewrite mandates that shape, govern and structure the world?

The outbreak of this global health crisis saw a strong backlash against globalization in the form of acceleration of trends underway. Before COVID-19 slammed the global economy earlier this year, China had adopted selective international exchange rates for political incentives. This had consequently led to US-China trade wars involving up to 25% tariff imposition on Chinese imports.

In March, COVID-19 contributed to this backdrop by declining the number of cargo ships setting off for the United States by 10%. The cost of shipping goods by air nearly doubled, restricting trade further. In order to contain the outbreak of the rapidly spreading virus, countries were forced to close their borders to foreign visitors which severely restricted the movement of people worldwide.

With no signs of the situation returning to normalcy, countries are desperately trying to be “self-sufficient” by ordering factories at home to produce ventilators, banning exports of face masks, and localizing pharmaceutical supply chains even at the cost of added expenses. The declaration of a potential suspension of immigration into the U.S by the President seemed like a final nail in the coffin for the era of globalization.

The world’s response to COVID comes across as ratifying Trump’s argument for protectionism and supply chain controls. This alludes to a pressing question in such uncertain times: Will the world remain flat after the curve flattens after all? Let’s first look at what does it mean for the “world to be flat”? In the book, ‘The world is flat’ by Thomas L. Friedman, the author endorses his view of the world as a level-playing field, wherein all players have equal opportunity and the world is a global market where historical and geographic boundaries are becoming increasingly irrelevant.

Globalization has persisted in different forms for decades. In my opinion, just like the dotcom bubble, 9/11 debacle, 2008 financial crisis, the COVID-19 pandemic too, is a temporary shock, which will perhaps change the face of globalization but not sink it. In the near future, we will likely either have a vaccine or much of the world will be infected by the virus. Either way, the current restrictions will neither be needed nor sustainable in the long run.

For instance, by the time the curve peaks, most countries will perhaps already have bought or produced enough inventory. In that case, will it really make sense to use tax-payers money on incurring exorbitant production costs to set up ventilator factories at home when their supply is already bolstered by sufficient purchase? Evidently, medical supply chains will change less than politicians currently promise!

But even after the shock evanesces, COVID-19 will heavily influence the decision-making process with regards to investment and relocation. Many argue that the crisis was an exemplary demonstration of increased risks associated with globalised supply-chains. A flip-side to the dispute is that in the quest to maximize profits and reduce the risk of localized disruption from the crisis, if anything, firms might only expand production lines across the world, creating employment more evenly, and promoting eventual global recovery. In fact, the renowned economist, Obstfeld, who served as IMF’s chief from late 2015 through 2018, said that “While global supply chains will undoubtedly change in a post-crisis economy, much of that change will be in the form of diversification, not on-shoring.”

While layoffs and increasing unemployment in a post-crisis recessive economy are inevitable, they will not mark the end of outsourcing. Turning to autarky-like economies will be too costly to be sustainable for countries world-over. There will be plenty of opportunities to employ people in jobs that demand highly skilled labour to meet the needs of the recovering economies. This will pave the way for Globalisation 3.0, described in Friedman’s book as individuals focusing on finding their foothold in the present global competition and making significant global collaborations. In fact, skill up-gradation of this form, to ensure relevance as demanded by the need of the hour, will push humans towards becoming antifragile, as recommended by Taleb.

However, “Outsourcing is just one dimension of a much more fundamental thing happening today in the world”, Friedman claims. Experts often view globalization from a one-dimensional perspective- physical goods and services crossing borders. But in fact, many intangibles- data, value, ideas, innovation frequently cross borders. In his book, Friedman emphasizes that “You don’t need to emigrate to innovate”. “Globalization in recent times has created a platform where intellectual work, intellectual capital, can be delivered from anywhere. It could be disaggregated, delivered, distributed, produced and put back together again — and this gave a whole new degree of freedom to the way work is done, especially work of an intellectual nature.” In light of this view of global integration, I believe that the world is going to get flatter. With workforces across nations getting training on Zoom video conferencing, to extensive sharing of knowledge in research on medical advances, the spillover of ideas and innovation is going to witness only an onward spur. The quantity and value of data transmitting between countries are increasing and with the high-value data processing replacing supply chains as the predominant channel of global economic exchange, I see this only increasing further.

So is the world after coronavirus tending to globalization or deglobalization? I think it depends on where you look. COVID can make it harder to ship Chelsea fan-club merchandise around the world, but no quarantine can contain cryptos from crossing borders!

Article by George Bangham ’17 (Economics of Public Policy)

In an article for the Resolution Foundation, George Bangham ’17 (Economics of Public Policy) looks at data on UK family finances in the period before the coronavirus pandemic and thinks about policy measures for those who may lose their primary source of income during the crisis.

Here is an excerpt:

We won’t know exactly how many people have lost their jobs due to coronavirus until at least the summer, when official statistics come out. But as well as monitoring the ongoing impact of the crisis, it’s equally important to consider the state of the country as the economic downturn hit home…

Amid the horror of the pandemic, and the legitimate fears of many families for their finances, it might seem frivolous to worry about statistics for the time being. But the lessons from the data are vital. They point us to new issues that the Government must fix. In a crisis, statistics can save livelihoods and save lives.

Charlie Thompson ’14 (ITFD) has built an RStats dashboard that tracks COVID-19 cases in the United States at the county level using the latest data from The New York Times.

Check it out to see how US communities are “flattening the curve”:

Opinion piece by Francesco Amodio ’10 (Economics) on Canada’s response to COVID-19 crisis

In a piece published on March 31 in the Montreal Gazette, Francesco Amodio ’10 (Economics) looks at measures taken by the Canadian government in response to the coronavirus pandemic.

Here’s an excerpt:

The measures taken by the Canadian government are in line with those taken in other countries, where governments are adopting either one or the combination of the following two approaches. In the first one, the government lets firms lay off workers, then pays out employment insurance benefits or other kind of income support transfers. The second approach focuses instead on “saving jobs,” with the government subsidizing wages in order to avoid layoffs.

Each approach has its pros and cons. In the short run, the size of wage subsidies and number of potential layoffs will determine which one is costlier. Perhaps more importantly, the two approaches differ in their medium- to long-run impacts.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.