Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Mental health outcomes significantly deteriorated in the United Kingdom as a result of the Covid-19 pandemic, particularly for younger individuals. This paper uses data from the Millennium Cohort Study to investigate the heterogeneity of mental health effects of the Covid-19 pandemic on adolescents by both personality types and personality traits. Using two-step cluster analysis we find three robust personality clusters: resilient, overcontrolled, and undercontrolled.

Conclusions

We surprisingly find that resilient individuals, who generally have better mental health, reported larger decreases in mental health during the pandemic than both undercontrollers and overcontrollers

The effect seems to be driven by the neuroticism trait, such that those with higher neuroticism scores fared better than those with lower scores during the pandemic

Our findings highlight that personality traits are important factors in identifying stress-prone individuals during a pandemic.

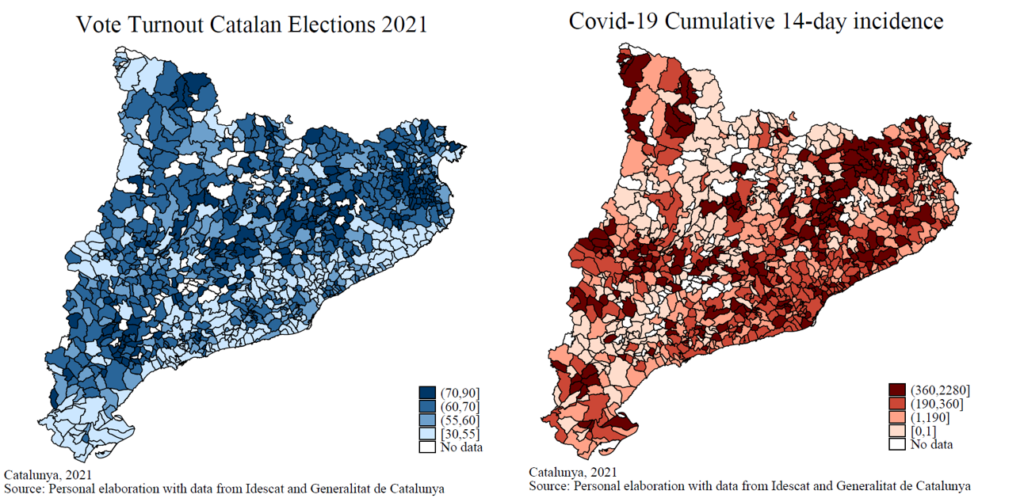

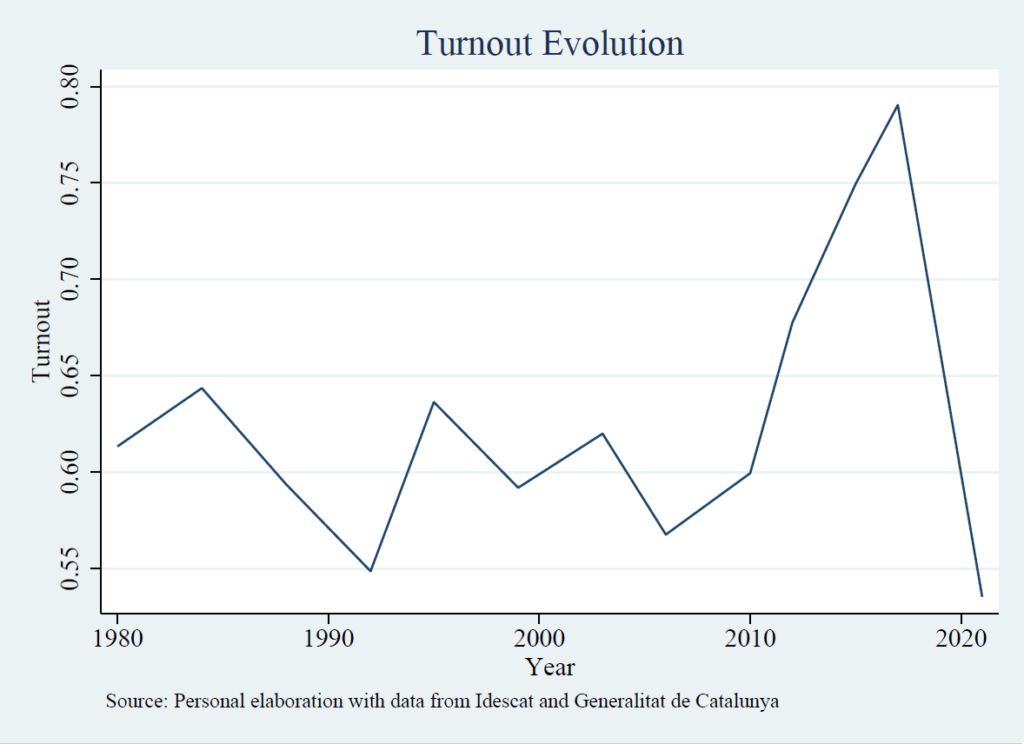

In the Catalan elections held on 14 February 2021, just a few weeks after the peak of the third wave of COVID-19, voter turnout was significantly lower than in 2017 (51.3% compared to 79.1%) and the lowest in history. Despite the political context being different compared to 2017, in the run-up to the election predicted turnout remained at similar levels until the emergence of Covid-19 – whereupon it dropped sharply. In these extraordinary elections, the vote share of the parties changed which shifted the Catalan political spectrum.

We study this relationship between Covid-19 and electoral results in Catalonia. To estimate the effect of the pandemic we explore the differences in cumulative Covid-19 incidence at the municipal level and compare it with electoral outcomes controlling for economic and demographic variables (population density, percentage of over-65 years old, share of foreign population and the unemployment rate).

The most widely used model of electoral participation, that of Riker and Ordeshook (1968), considers that the decision to participate is based on a cost-benefit trade-off between the expressed benefit of voting (feeling fulfilled, considering that civic duty is fulfilled, etc.) and the cost that individuals associate with participation. This cost rose sharply, because voting implied a higher risk of contracting the disease and the inconvenience caused by anti-covid measures. Therefore, higher costs would imply lower turnout as shown by several empirical studies, which find that with small increases in cost turnout drops significantly (eg. Aldrich, 1993). We assume that the increase in cost is the same for all (although there could be differences by age, and so we control for the most vulnerable group, the over-65s), which would imply a fall in participation, but could also induce changes in the outcome. This change may be due to differences in the “sentimental” benefit of voting between voters of different parties.

Economic theory also indicates who voters choose, conditional on voting. According to “retrospective” voting theory, voters support or punish parties in government in response to their performance in a crisis such as Key (1966). In contrast, according to “prospective” voting theory, the individual votes for the party that he believes will do better or, as Leininger and Schaub (2020) argue, seeks to match the party in regional and national government for more optimal crisis management.

Effect on participation

As seen in the maps above, the areas with the highest cumulative Covid incidence also have a lower percentage of participation, especially the Barcelona metropolitan area. Our analysis shows that an increase of 100 points in cumulative incidence in the last 14 days is related to a drop of 2.6 percentage points in turnout. To understand the magnitude, this is equivalent to one extra Covid case in a municipality of 1,000 inhabitants, so we estimate that the effect of the pandemic is quite high. To understand the impact of the second and third waves of Covid-19, we have conducted the analysis with cumulative incidence measures in the last month and in the last 4 months prior to the elections. However, as the period lengthens, the effect on turnout decreases (1.3 and 0.4 percentage points respectively).

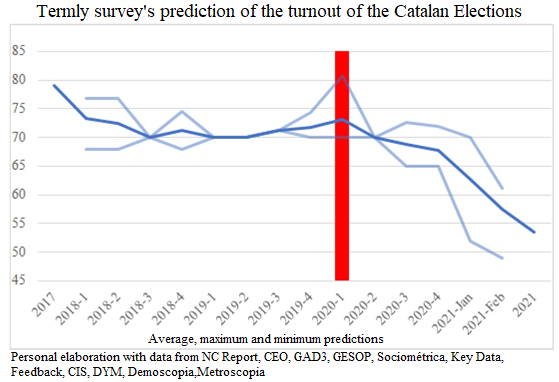

However, the political context also changed: while in 2017 the voting framework was centred on the independence process (which led to the historical record turnout); in 2021 it was the pandemic that defined the elections. However, the trigger for this change of context (and the neglect of the independence process) was the eruption of the virus. As can be seen in the graph below showing the predicted turnout for the elections to the Parliament of Catalonia. Since Covid-19 appears to be the only element of exogenous variation between municipalities when comparing the 2017 and 2021 elections, we can infer causality.

These results are in line with the theory of the myopic voter who takes into account episodes closer to the election when voting. In this case, the myopic voter is acting rationally, as they account for the actual risk at the time of the vote rather than the risk of the past few months.

Effect on results

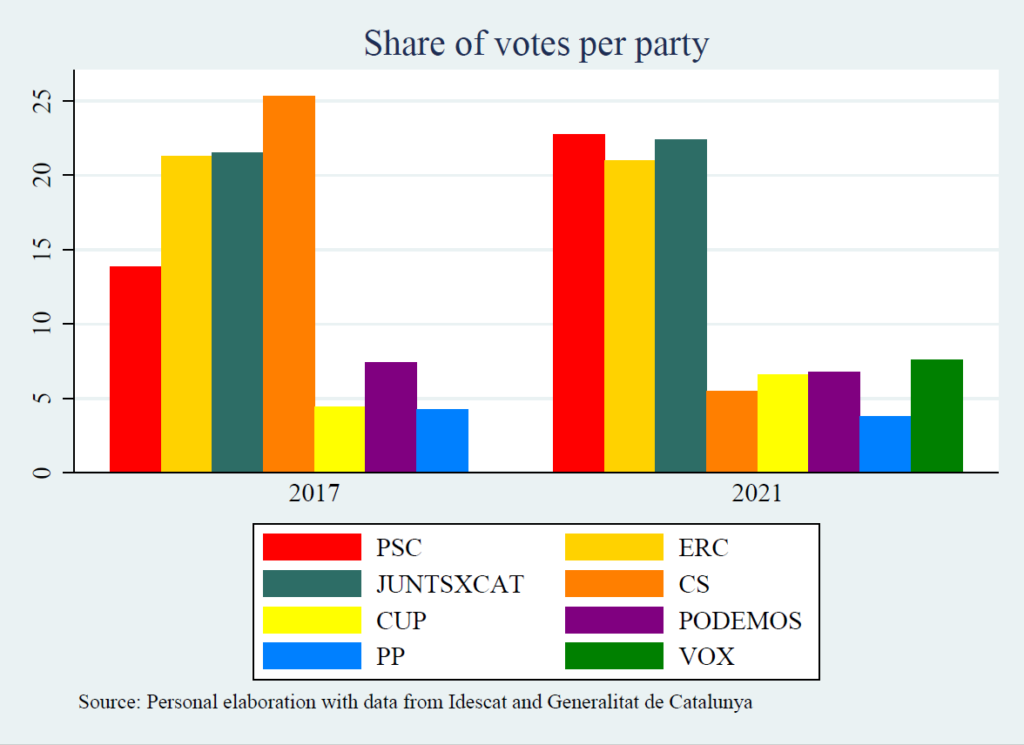

Secondly, the elections brought a major shift in the political spectrum, as can be seen in the bar charts above. For this reason, we have not been able to include other elections, as they were not comparable with each other. We have grouped the political parties into the following ideological and identity groups:

Pro-independence left: ERC and CUP.

Pro-independence right-wing: JUNTSXCAT and PDECAT

Non-independence left-wing: PSC and PODEMOS

Non-independence right: PP, Cs, and VOX

First, we respectively analyse the pro-independence and non-independence groups, the victors (the pro-independence coalition), and the opposition. The results show that the pandemic has a positive effect on the percentage of the vote of the pro-independence parties and a negative effect on the non-independence group. This effect can be seen as a retrospective vote, showing a certain approval by pro-independence voters of how the regional government has handled the pandemic.

On the other hand, in the analysis of the groups divided into identity and ideological groups, we find that the group with the highest positive coefficient is the non-independence left – the coalition in charge of the central government at the time of the elections. This behaviour is associated with the prospective vote. With the arrival of Salvador Illa (The Spanish Minister of Health during the pandemic) as the PSC candidate, the party was reinforced and ends up as the winner of the elections. This positive effect can be seen as an attempt to align the post-pandemic recovery strategy in Catalonia with that of the rest of Spain.

In conclusion, our results suggest that COVID-19 had a significant outcome in the Catalan elections that translated into a negative relationship between the virus and turnout. In contrast, the relationship is positive between cumulative incidence and the vote of pro-independence parties and the non-independence left-wing group. At the same time, the retrospective theory seems to hold true as there has been strong support for the government in office based on their management of the pandemic.

Connect with the authors

Iván Auciello Estévez ’21 is a student in the Barcelona GSE Master’s in Economics. After graduating he plans to work as a Research Assistant at Banco de España.

Pau Jovell Codina ’21 is a student in the Barcelona GSE Master’s in Economics. After graduating he plans to work as a Research Assistant at Banco de España.

Steffi gave an interview to CEPR’s Tim Phillips about the team’s research:

Policies to avoid zombification of the economy

In an accompanying VoxEU column, the authors discuss the risks that government responses to COVID-19 could “zombify” the economy.

“A representative consumer survey in five EU countries indicates that many consumers do not miss certain goods and services they have cut down on since the COVID-19 outbreak,” the authors explain in their column. “Fiscal policy must recognise that some firms will become obsolete in the altered post-COVID-19 environment. To achieve a swift recovery, these obsolete firms must be allowed to fail fast so that resources can be reallocated to more efficient uses. Instead, fiscal support should be laser-like in targeting those households who are particularly hard hit by the crisis. Such support should be oriented towards helping displaced workers retrain and find new jobs.”

Prospective economic developments depend on the behavior of consumer spending. A key question is whether private expenditures recover once social distancing restrictions are lifted or whether the COVID-19 crisis has a sustained impact on consumer confidence, preferences, and, hence, spending. Changes in consumer behavior may not be temporary, as they may reflect long-term changes in attitudes arising from the COVID-19 experience. This paper uses data from a representative consumer survey in five European countries conducted in summer 2020, after the release of the first wave’s lockdown restrictions. We document the underlying reasons for households’ reduction in consumption in five key sectors: tourism, hospitality, services, retail, and public transports. We identify a large confidence shock in the Southern European countries and a permanent shift in consumer preferences in the Northern European countries. Our results suggest that horizontal fiscal support to all firms risks creating zombie firms and would hinder necessary structural changes to the economy.

Alexander Hodbod ’12 (International Trade, Finance, and Development). Counsellor to ECB Representative to the Supervisory Board, European Central Bank (DGSGO-SO), Frankfurt, Germany.

Cars Hommes. Professor of Economic Dynamics at CeNDEF, Amsterdam School of Economics, University of Amsterdam, and research fellow of the Tinbergen Institute, Amsterdam, The Netherlands, Senior Research Director (Financial Markets Department), Bank of Canada.

Stefanie J. Huber ’10 (Economics). Assistant Professor at CeNDEF, Amsterdam School of Economics, University of Amsterdam, and research candidate fellow of the Tinbergen Institute, Amsterdam, The Netherlands.

Isabelle Salle. Principal Researcher at the Bank of Canada (Financial Markets Department), research fellow at the Amsterdam School of Economics, University of Amsterdam, and research fellow of the Tinbergen Institute, Amsterdam, The Netherlands.

Maximilian and Elliot connected through social media due to the Barcelona GSE connection and started working together on this piece due to shared research interests.

The COVID-19 pandemic is changing the way that we live our lives. As time passes it is becoming apparent that even once the lockdown policies have been eased and some level of normality has been resumed, the new world that we live in will be different to the one we knew before. This article focuses on emerging trends within the UK that have largely taken place as a result of COVID-19, or in some cases the pandemic has simply accelerated a trend that was already occurring. We then look to offer a range of public policy solutions for the recovery period where the overarching objective is to increase wellbeing in society in a sustainable way. These are focused towards the UK but several could be paralleled to other advanced economies.

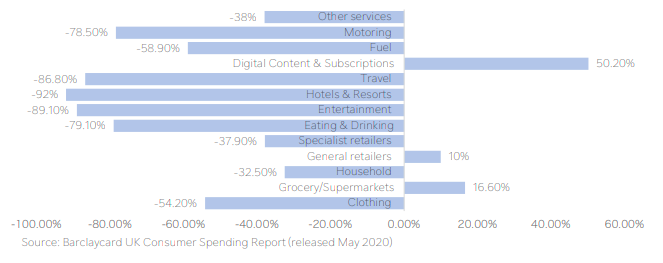

Chart 1. Consumer spending in April 2020 by category, % change year-on-year

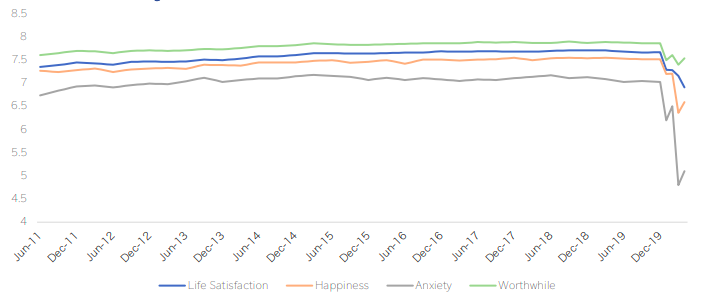

But first, before we get to the policy solutions, briefly, what have been the main economic and wellbeing effects that we have seen as a result of COVID-19? In 2020, it is expected that the fall in overall economic output is going to be larger than during the financial crisis in 2008. Much of this is due to the level of decline in economic activity as a result of the UK governments lockdown policy. This was a necessary decision in order to reduce the spread of the virus and ensure the health service still has capacity to treat those that have unfortunately caught the disease. However, it has led to a significant liquidity shock for both households and businesses. Large portions of the labour market are now out of work and levels of consumer spending have declined rapidly (Chart 1). Alongside sharp falls in measures of economic performance, measures of wellbeing have declined rapidly as well (Chart 2). Increases in measures of uncertainty have mirrored increases in anxiety. While, social distancing policies are having a large impact on measures of happiness.

Chart 2. ONS wellbeing measures (2011-2020)

Source: ONS. Notes: Each of these questions is answered on a scale of 0 to 10, where 0 is “not at all” and 10 is “completely”. Question: “Overall, how satisfied are you with your life nowadays?”, “Overall, to what extent do you feel that the things you do in your life are worthwhile?”, “Overall, how happy did you feel yesterday?”, “Overall, how anxious did you feel yesterday?”.

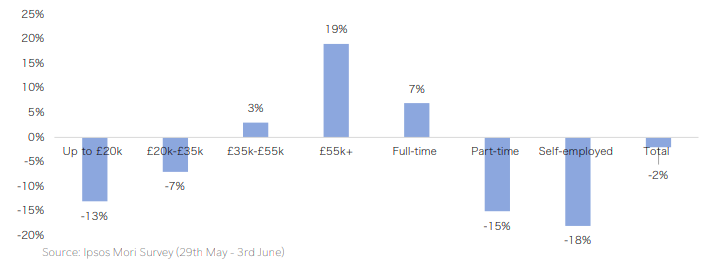

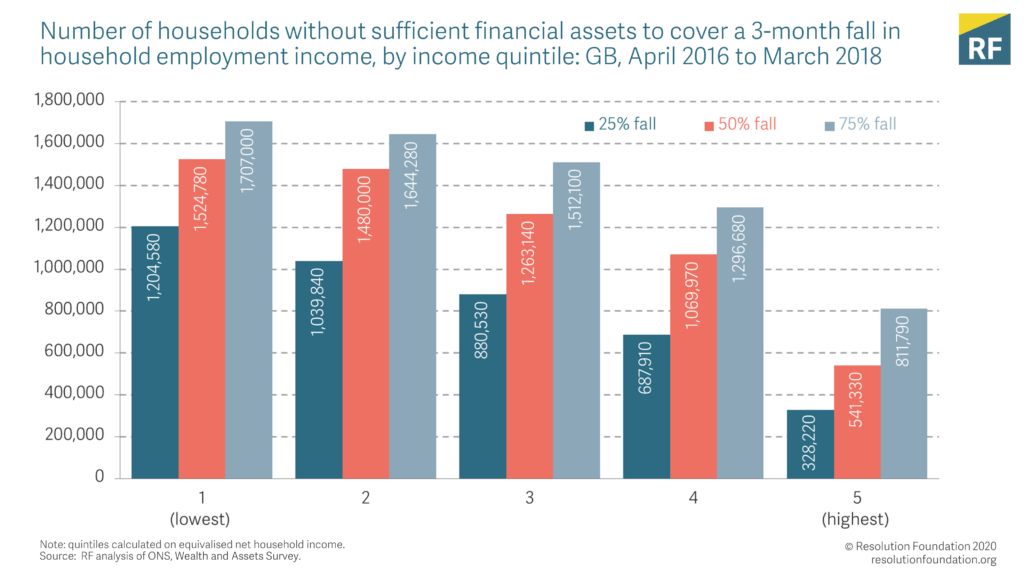

The UK government responded to the shock posed by COVID-19 with a range of policy interventions to provide funding to those that have been most impacted. At a macro level, the long-lasting effects of this crisis will be more pertinent if economic activity does not respond quickly after the government’s schemes have ended. Large portions of UK businesses have limited cash reserves to fall back on in a scenario where demand remains subdued for some time. However, even if the recovery period is strong there will still have been some clear winners and losers during this crisis. Younger workers, those on lower incomes and those with atypical work contracts are the ones that have been most heavily impacted (Chart 3). Whilst those on higher incomes, that are more likely to be able to work from home, have increased their household savings during this period, due to less opportunities to consume.

Chart 3. Impact of COVID-19 on household savings by income and employment type

The policy solutions outlined below aim to be complementary of one another and look to amplify observed trends that are positive for wellbeing and to provide intervention where trends have been negative for wellbeing:

Climate at the centre of the response: This is less a policy recommendation and more a theme for the response. However, our message here is that increased public spending projects, focused towards green initiatives should be combined with a coherent carbon tax policy which influences incentives and helps to support the UK’s transition to a low carbon economy.

Labour market reforms: The government should look to develop a centralised job retraining and job matching scheme that supports workers most impacted by COVID-19, helps to encourage structural transformation towards emerging industries and increases the amount of highly skilled workers in the UK workforce.

Tough decisions on business: Some businesses will require further assistance from the UK government in the form of equity funding, rather than the debt funding seen so far. This should be done on a conditional basis, requiring all these businesses to comply with the UK’s climate objectives and should only be provided to businesses in industries that are expanding or strategically important to the UK economy.

Modernising the regions on a cleaner, greener and higher level: Looking to build on the governments ‘levelling up the regions’ policy to reduce regional inequalities, our policy consists of government funded infrastructure policies that include green investments for regions outside of the UK’s capital.

Harbouring that rainbow effect: Building on the increased community spirit that has been observed during the pandemic, this policy solution looks to increase localised community funding to maintain social cohesion and support those with mental health issues.

Lastly, as the policy recommendations focus on expanding public investment to support the recovery, it is important to consider what this means for public debt sustainability in the UK. The conclusion is that as a result of the low interest rate environment, the most efficient way out of this recession is to borrow and spend on projects that will increase resilience to future shocks and support the UK’s transition to a low carbon economy.

Please click on the link below to read about this in more detail. Comments are welcome.

BIS Bulletin by Sebastian Doerr ’13 (Economics) and Leonardo Gambacorta

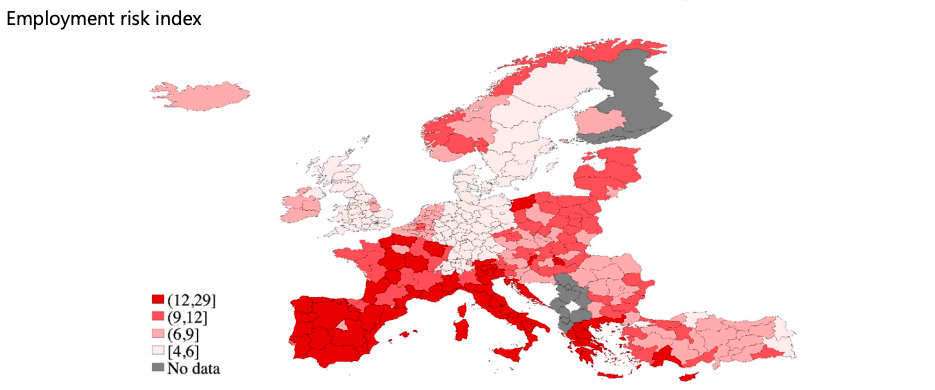

The outbreak of Covid-19 and the ensuing measures to contain the pandemic have brought Europe into a deep downturn. GDP is expected to drop by around 8% in the euro area this year (ECB (2020)), a significantly steeper decline than forecasted for the United States or Asia (IMF (2020)). One of the major reasons why the European economy is expected to be so hard-hit is its high share of small firms, especially in southern and eastern European countries. Small firms are financially more constrained and bank-dependent than larger firms. They also sell goods predominantly in local markets and with less diversified sources of revenue.

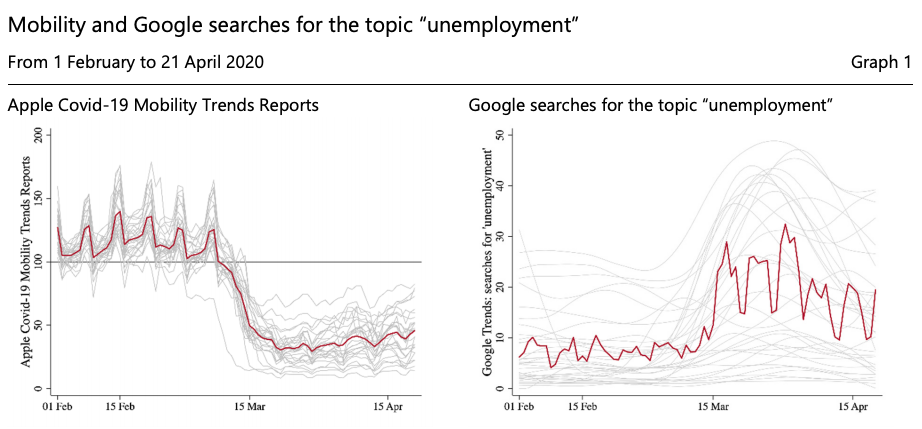

This Bulletin investigates which European regions face higher risks to employment from Covid-19. We first use data on local industry-level employment before the outbreak and construct a measure of local employment exposure to Covid-19, using the methodology developed in Doerr and Gambacorta (2020) for the US. We then extend the analysis by taking into account the share of employment among small firms in different regions. Specifically, we calculate an employment risk index based on the interaction of sectoral exposure and the share of small business employment. Our results show that while several European regions employ a high share of people in sectors particularly exposed to the economic consequences of the pandemic, the high share of small firms in southern Europe puts employment in those regions particularly at risk. We show that regions with a higher employment risk index, ie those with higher sectoral exposure and a higher share of small businesses, also exhibit a stronger increase in Google searches for unemployment, providing a cross-check of our measure of local employment risk.

The left-hand panel shows the evolution of Apple Covid-19 Mobility Trends Reports from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). The index is averaged across all subcategories. The Mobility Trends index reflects requests for directions in Apple Maps and is standardised to 100 on 13 January 2020. The right-hand panel shows the relative frequency of Google searches for the topic “unemployment” from 1 February to 21 April 2020 for individual European countries (grey lines) and the European average (red line). For illustration, country-specific lines are Hodrick Prescott-filtered trend components with a smoothing parameter of 500.

Sources: Apple Covid-19 Mobility Trends Reports; Google Trends; authors’ calculations.

Key takeaways

We construct employment risk indices for European regions that reflect the share of jobs under threat from Covid-19. The risk index is based on local employment in sectors that are more exposed to the pandemic and on the regional incidence of small firms.

Employment in regions in southern Europe and France is shown to have high risk indices, while regions in northern Europe have lower risk indices. Eastern and central European regions have intermediate risk indices.

Regions with a higher risk index have a bigger jump in Google searches for unemployment-related terms.

The challenge for the EU is to deliver a policy response that reduces, not exacerbates differences. This requires a level playing field (e.g. for state aids) and a high degree of coordination.

Help Economics alum Steffi Huber ’10 by participating this survey!

I’d like to invite Barcelona GSE students and alumni to participate in a survey I’m conducting with Isabelle Salle (Bank of Canada, research fellow at the University of Amsterdam) to help understanding households’ consumption and investment responses to the prolonged “dance” phase of the COVID-19 crisis.

As yet, policymakers and academics do not have good estimates for how people might behave in this crucial period. You can help to fill this gap, and in the process help to build a collective understanding of the economic consequences of the pre-vaccine crisis.

We’ve received around 1,000 responses to the survey so far, and we are using it as a trial survey which will be adjusted for a large grant application to run a representative survey in all major European countries.

Please read below to know more about what is involved.

Purpose of the research

This research survey aims to shed light on household responses to the COVID-crisis in two ways. First, we want to investigate how the crisis has already changed investment and consumption demands. Second, we want to understand the expected consumption and investment behavior of households when lockdown restrictions are progressively lifted but prior to an effective treatment or vaccine being available.

What taking part involves

There will be a series of questions about your current and planned consumption and investments. The survey requires no special knowledge for you to complete it. Your participation is voluntary, you do not have to answer all the questions if you do not want to, and you may withdraw from the study at any point.

Your data

The information provided by you in the survey will be held anonymously, so it will be impossible to trace this information back to you individually. The anonymous data itself will be held indefinitely and may be used to produce reports, presentations, and academic publications. If you have any questions or concerns about this research please feel free to contact any of the researchers involved in the project, using the contact details below.

The survey can be answered in 16 different languages. So, don’t hesitate to forward this email to all your international friends!

See this website for more info on the objectives of this project.

Stefanie J. Huber ’10 is Assistant Professor at the University of Amsterdam. She is an alum of the Barcelona GSE Master’s in Economics and GPEFM PhD Program (UPF and Barcelona GSE).

In my all-time favourite book ‘Antifragile’, Nassim Taleb divides the world into 3 categories- fragile, robust and antifragile. He refers to fragility as the state of being that involves avoiding disorder and disruption for fear of the mess that threatens to disrupt your life: you think you are keeping safe, but really you are making yourself vulnerable to the shock that will tear everything apart. Robustness is the ability to stand up to shocks without flinching, without changing who you are. But you are antifragile if shocks make you better able to adapt to each new challenge you face. You are antifragile if you can opportune from disruptions, to be stronger and more creative. Taleb thinks we should all try to be antifragile!

On March 11, 2020, declared a world pandemic, the COVID-19, is an epitome of the chaotic disruption Taleb was referring to. The onset of this crisis got me pondering whether populations, institutions, financial bodies, governments and policy-makers -i.e. the world as a whole will be able to be resilient in the face of the aftermath of this crisis? Do we have the acceptance, courage and strength besides the technical, innovative and problem-solving skills to start afresh and turn this disequilibrium around into the most memorable salvation story we have ever seen? Or will we succumb to this dooming, seemingly apocalyptic spiral, and lose everything we take for granted in our day-to-day lives? When the noise of this unprecedented shock dies, will we be left at the inception of a brand new system that will push us to rethink policies, and rewrite mandates that shape, govern and structure the world?

The outbreak of this global health crisis saw a strong backlash against globalization in the form of acceleration of trends underway. Before COVID-19 slammed the global economy earlier this year, China had adopted selective international exchange rates for political incentives. This had consequently led to US-China trade wars involving up to 25% tariff imposition on Chinese imports.

In March, COVID-19 contributed to this backdrop by declining the number of cargo ships setting off for the United States by 10%. The cost of shipping goods by air nearly doubled, restricting trade further. In order to contain the outbreak of the rapidly spreading virus, countries were forced to close their borders to foreign visitors which severely restricted the movement of people worldwide.

With no signs of the situation returning to normalcy, countries are desperately trying to be “self-sufficient” by ordering factories at home to produce ventilators, banning exports of face masks, and localizing pharmaceutical supply chains even at the cost of added expenses. The declaration of a potential suspension of immigration into the U.S by the President seemed like a final nail in the coffin for the era of globalization.

The world’s response to COVID comes across as ratifying Trump’s argument for protectionism and supply chain controls. This alludes to a pressing question in such uncertain times: Will the world remain flat after the curve flattens after all? Let’s first look at what does it mean for the “world to be flat”? In the book, ‘The world is flat’ by Thomas L. Friedman, the author endorses his view of the world as a level-playing field, wherein all players have equal opportunity and the world is a global market where historical and geographic boundaries are becoming increasingly irrelevant.

Globalization has persisted in different forms for decades. In my opinion, just like the dotcom bubble, 9/11 debacle, 2008 financial crisis, the COVID-19 pandemic too, is a temporary shock, which will perhaps change the face of globalization but not sink it. In the near future, we will likely either have a vaccine or much of the world will be infected by the virus. Either way, the current restrictions will neither be needed nor sustainable in the long run.

For instance, by the time the curve peaks, most countries will perhaps already have bought or produced enough inventory. In that case, will it really make sense to use tax-payers money on incurring exorbitant production costs to set up ventilator factories at home when their supply is already bolstered by sufficient purchase? Evidently, medical supply chains will change less than politicians currently promise!

But even after the shock evanesces, COVID-19 will heavily influence the decision-making process with regards to investment and relocation. Many argue that the crisis was an exemplary demonstration of increased risks associated with globalised supply-chains. A flip-side to the dispute is that in the quest to maximize profits and reduce the risk of localized disruption from the crisis, if anything, firms might only expand production lines across the world, creating employment more evenly, and promoting eventual global recovery. In fact, the renowned economist, Obstfeld, who served as IMF’s chief from late 2015 through 2018, said that “While global supply chains will undoubtedly change in a post-crisis economy, much of that change will be in the form of diversification, not on-shoring.”

While layoffs and increasing unemployment in a post-crisis recessive economy are inevitable, they will not mark the end of outsourcing. Turning to autarky-like economies will be too costly to be sustainable for countries world-over. There will be plenty of opportunities to employ people in jobs that demand highly skilled labour to meet the needs of the recovering economies. This will pave the way for Globalisation 3.0, described in Friedman’s book as individuals focusing on finding their foothold in the present global competition and making significant global collaborations. In fact, skill up-gradation of this form, to ensure relevance as demanded by the need of the hour, will push humans towards becoming antifragile, as recommended by Taleb.

However, “Outsourcing is just one dimension of a much more fundamental thing happening today in the world”, Friedman claims. Experts often view globalization from a one-dimensional perspective- physical goods and services crossing borders. But in fact, many intangibles- data, value, ideas, innovation frequently cross borders. In his book, Friedman emphasizes that “You don’t need to emigrate to innovate”. “Globalization in recent times has created a platform where intellectual work, intellectual capital, can be delivered from anywhere. It could be disaggregated, delivered, distributed, produced and put back together again — and this gave a whole new degree of freedom to the way work is done, especially work of an intellectual nature.” In light of this view of global integration, I believe that the world is going to get flatter. With workforces across nations getting training on Zoom video conferencing, to extensive sharing of knowledge in research on medical advances, the spillover of ideas and innovation is going to witness only an onward spur. The quantity and value of data transmitting between countries are increasing and with the high-value data processing replacing supply chains as the predominant channel of global economic exchange, I see this only increasing further.

So is the world after coronavirus tending to globalization or deglobalization? I think it depends on where you look. COVID can make it harder to ship Chelsea fan-club merchandise around the world, but no quarantine can contain cryptos from crossing borders!

Article by George Bangham ’17 (Economics of Public Policy)

In an article for the Resolution Foundation, George Bangham ’17 (Economics of Public Policy) looks at data on UK family finances in the period before the coronavirus pandemic and thinks about policy measures for those who may lose their primary source of income during the crisis.

Here is an excerpt:

We won’t know exactly how many people have lost their jobs due to coronavirus until at least the summer, when official statistics come out. But as well as monitoring the ongoing impact of the crisis, it’s equally important to consider the state of the country as the economic downturn hit home…

Amid the horror of the pandemic, and the legitimate fears of many families for their finances, it might seem frivolous to worry about statistics for the time being. But the lessons from the data are vital. They point us to new issues that the Government must fix. In a crisis, statistics can save livelihoods and save lives.

Charlie Thompson ’14 (ITFD) has built an RStats dashboard that tracks COVID-19 cases in the United States at the county level using the latest data from The New York Times.

Check it out to see how US communities are “flattening the curve”:

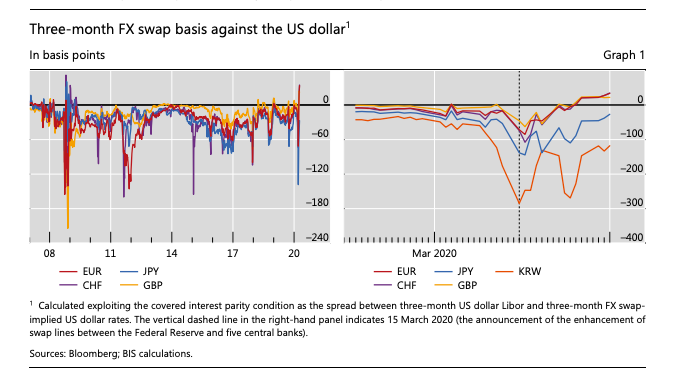

In this new publication for the Bank for International Settlements, Egemen Eren ’09 and co-authors Stefan Avdjiev and Patrick McGuire review recent events in FX swap markets in the context of the longer-term trends in the demand for dollars from institutional investors.

Key takeaways

Since the start of the Covid-19 pandemic, indicators of dollar funding costs in foreign exchange markets have risen sharply, reflecting both demand and supply factors.

The demand for dollar funding has grown in recent years, reflecting the currency hedging needs of corporates and portfolio investors outside the United States.

Against this backdrop, the financial turbulence of recent weeks has crimped the supply of dollar funding from financial intermediaries, sharply lifting indicators of dollar funding costs.

These costs have narrowed after central banks deployed dollar swap lines, but broader policy challenges remain in ensuring that dollar funding markets remain resilient and that central bank liquidity is channelled beyond the banking system.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.