Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

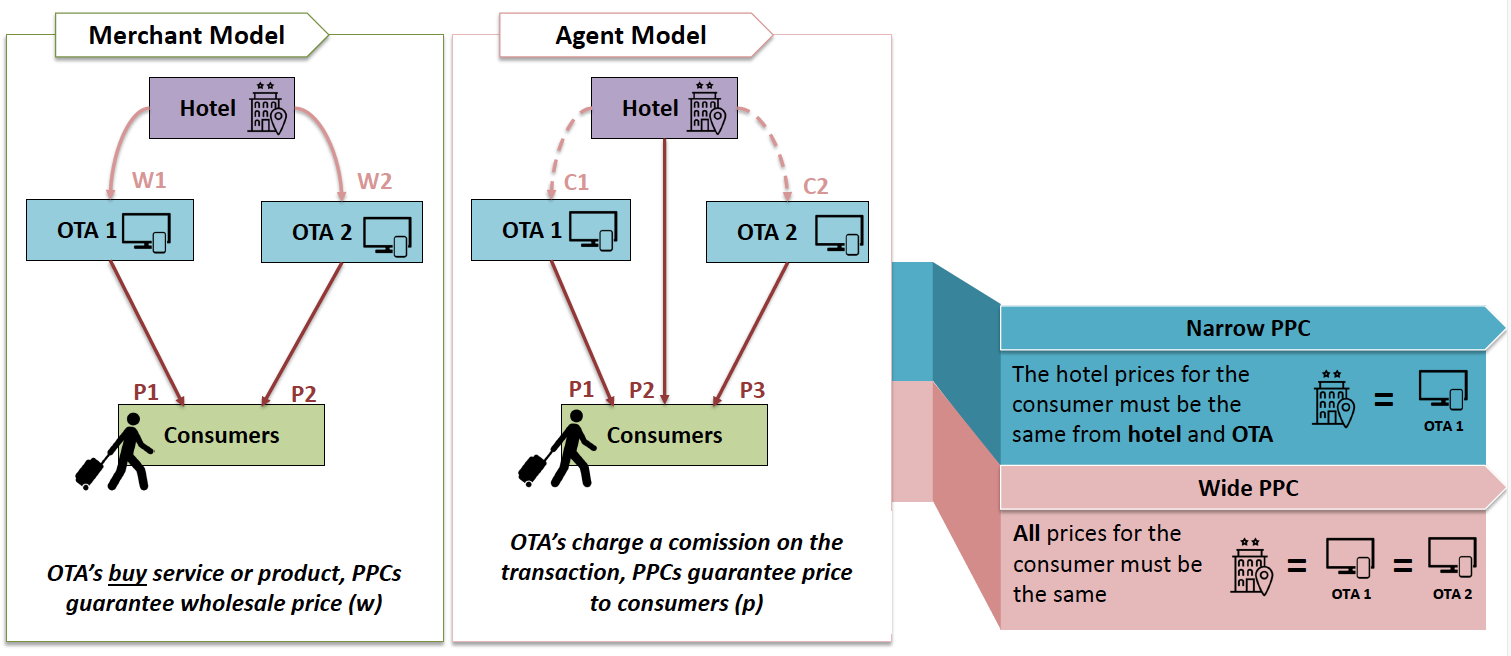

Under the context of digital platforms who act as an intermediary between consumers and sellers, Price Parity Clauses (PPCs) is a contractual restriction for the seller not to sell at a lower price through any other channel (the so-called wide PPCs), or only in its own channel (narrow PPCs). These clauses present a trade-off between efficiencies and anticompetitive effects. On one side, PPCs act as a committing device of the seller to solve the show-rooming effect suffered by platforms (a particular form of free- riding), at the same time that it ensures platforms viability and enhances its incentives to invest and innovate. On the other side, PPCs allow platforms to charge higher fees, and lead to foreclosure of the market. Currently, neither the EC nor NCAs have set a clear guidance on how to assess these clauses. The main contribution of this paper is to set a legal standard for both wide and narrow PPCs using the cost-error analysis. The conclusions we arrived to are that wide PPCs should be per se illegal; and narrow PPCs should be presumed legal unless proven otherwise, except if narrow PPCs are eliminating the competitive restraints of the platform, in which case the standard should be that of rebuttable presumption of illegality.

Conclusions:

Digital Economy will rise the use of Digital Platforms. Network externalities inherent to two-sided markets lead to high market power that make platforms an indispensable ally.

Digital Platforms use PPCs and this is capturing the interest of Competition Authorities. But there is no consensus with respect to the legal standard.

PPCs present a trade-off: On the one hand efficiencies results in reduction of search costs, prevents showrooming, incentives on investment and innovation. On the other hand, anti-competitive effects arise, creating high fees, foreclosure, collusion.

The results of our cost-error analysis are that Wide PPCs Min Type II error, therefore should be Per se illegal. Narrow PPCs Min Type I error: Rebuttable Presumption of Legality, except if (i) One-Stop Shop/Network; (ii) Brand Positioning; (iii) Switching costs: Min. Type II: Rebuttable Presumption of illegality

Master project by Jordi Gutiérrez, Domenic Kellner, Philip King, Simon Neumeyer, and Dorota Scibisz

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

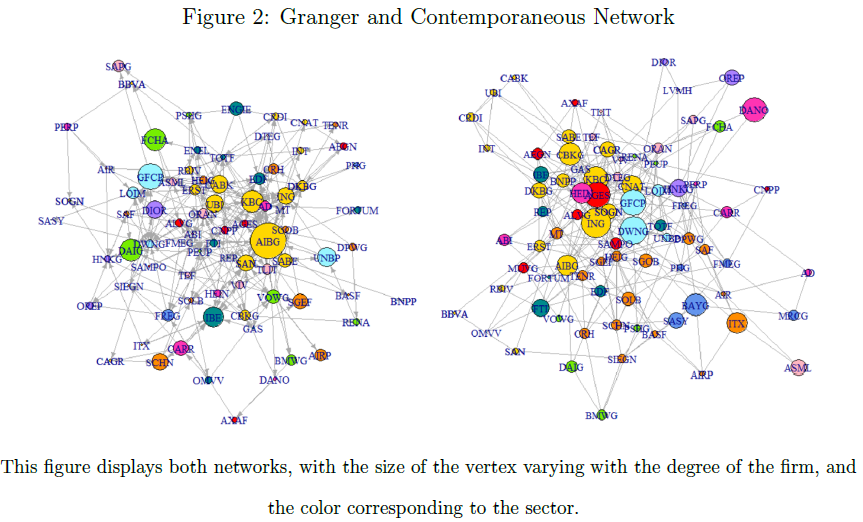

We identify contemporaneous and Granger-causal linkages between the 86 biggest companies, representing both the financial and real sectors, of the Eurozone economy that serve as paths of shock transmission. Network analysis lends itself very naturally to the study of systemic risk due to its preoccupation with interconnections and notions of centrality. We employ an estimation methodology introduced by Barigozzi and Brownlees (2018) using market data for daily volatilities from the Eurostoxx index. Our results are in line with the existing literature – the banking sector is found to be highly interconnected and responsible for most Granger-network spillovers. Moreover, only a small subset of firms appear to Granger-cause other residual volatilities, providing support for regulators’ targeting of Systemically Important Financial Institutions.

Conclusions:

Following the work of Barigozzi and Brownlees (2018), this paper applies the nets algorithm to study the interconnectedness of the 86 biggest firms in the Eurozone for a sample period spanning from May 2008 to April 2018. We have estimated two sparse networks of return volatilities that allow us to measure systemic risk and detect patterns of its transmission. Compared to the original study of the US economy, we have utilised a more detailed set of industries. What is more, country-specific volatilities were added as an extra factor in order to obtain more precise firm-specific residual volatilities, while still uncovering a large number of connections.

At the contemporaneous level almost all industries exhibit high connectedness, a pattern which became immediately apparent on the initial heatmaps of residual correlations. Even when controlling for sectoral and country volatilities we find clusters of firms reacting strongly with other firms within the same business area. These co-movements are especially remarkable within the banking, industrial, and technological sectors.

However, it is a small subset of companies, mostly financial firms, that displays high interconnectedness at the Granger-causal level. Consequently, we conclude that banks are particularly important risk transmitters in the Eurozone network. The subset of banks is especially susceptible to volatilities stemming from other sectors. This makes intuitive sense as we can think of banks being highly leveraged when compared with other entities (Freixas et al., 2015). Moreover, banks amplify and transmit shocks to all the other sectors, which reflects their unique economic role as financial intermediaries. Altogether, this provides empirical support for the regulatory targeting of certain Systemically Important Financial Institutions.

Master project by Deepshikha Deb, Nils Handler, Vladimir Peciar, Ksenia Proka, Juliane Stolle

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2018. The project is a required component of every master program.

This paper analyzes whether access to imported intermediate goods can raise export performance of Russian firms. We employ an instrumental variable strategy which exploits variation in firm-specific input tariffs to identify the effect of imported intermediates on firm exports during the period 2007-2013, utilizing a unique firm-level database on firm characteristics and customs declarations. We find that input tariff reductions can raise firm exports significantly, as can other measures aimed at increasing imports of intermediate goods of exporting firms in Russia. Import promotion targeted at exporting firms in high-tech sectors can be up to three times more effective. Better access to imports can also help increase the currently low share of exporting firms within the Russian enterprise landscape. Our results suggest that with the rising globalization and fragmentation of production processes, countries interested in raising exports need to think strategically of promoting imports as well. We propose and discuss several policy measures for Russia in the areas of tariff regulation, non- tariff measures, trade facilitation and trade integration.

Conclusions:

Using a comprehensive firm-level dataset which combines information on Russian company characteristics, involvement in trade and input tariff rates, we reveal a strong positive impact of intermediate imports on firm exports in the manufacturing sector. These results imply that improved access to intermediate goods at the international market can serve as a means to raise Russia’s currently weak export performance outside the natural resource sector. Import promotion policies targeted at intermediate goods imported by firms in high-tech sectors can be especially effective and raise exports by up to three times more than in other sectors. Better access to imports can also help increase the currently low share of exporting firms within the Russian enterprise landscape.

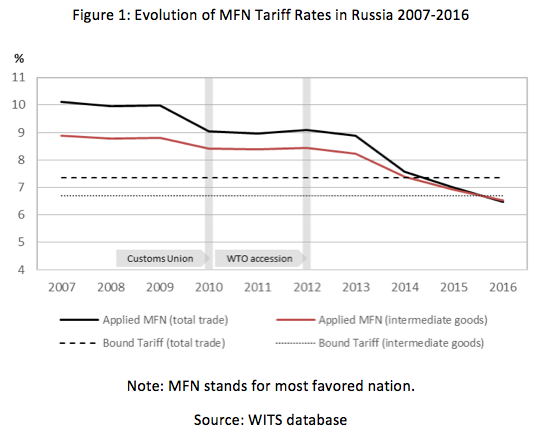

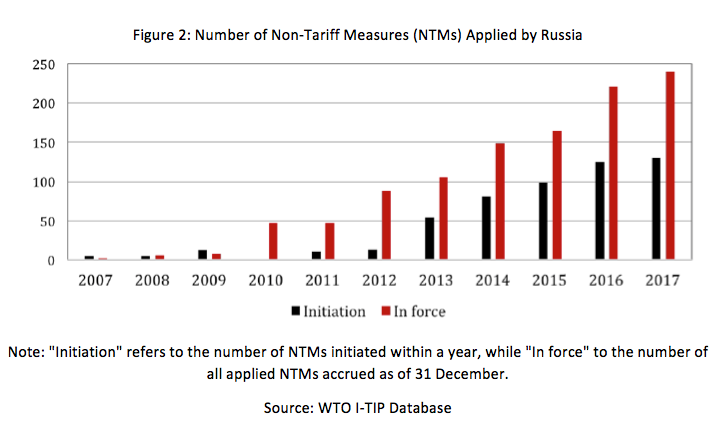

Our estimation results indicate that a one percentage point decrease in input tariffs would raise firm exports by approximately one percent. Even though tariffs have been significantly decreased over the past decade in the context of regional integration and Russia’s WTO accession (see figure 1), there is still ample room to lower input tariffs in order to promote exports. More than 40 percent of intermediate goods imported by Russian exporting manufacturing firms and more than 30 percent of goods imported by exporting firms in high-tech manufacturing sectors still entered the customs union at a tariff rate above 5 percent in 2015. Besides tariff reductions, Russia could consider lowering non-tariff measures (NTMs) and enhancing trade facilitation, which can also contribute to better access to intermediate goods of exporting firms, as suggested by our IV results. As can be seen from figure 2, NTMs have increased sharply since Russia joined the WTO in 2012. It should be pointed out, however, that trade policies aimed at promoting imports of intermediate goods alone will not be sufficient to boost non-oil export growth and export competitiveness of Russian firms. To bring the desired success, they need to be combined with a range of other important policies, including improving access of Russian exporters to foreign markets and simplifying the existing export regulation, as well as comprehensive structural reforms and measures to improve the business environment.

Economics master project by Marc de la Barrera, Juraj Falath, Dorian Henricot and Jean-Alexandre Vaglio (Class of 2017)

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Marc de la Barrera, Juraj Falath, Dorian Henricot and Jean-Alexandre Vaglio

Master’s Program:

Economics

Paper Abstract:

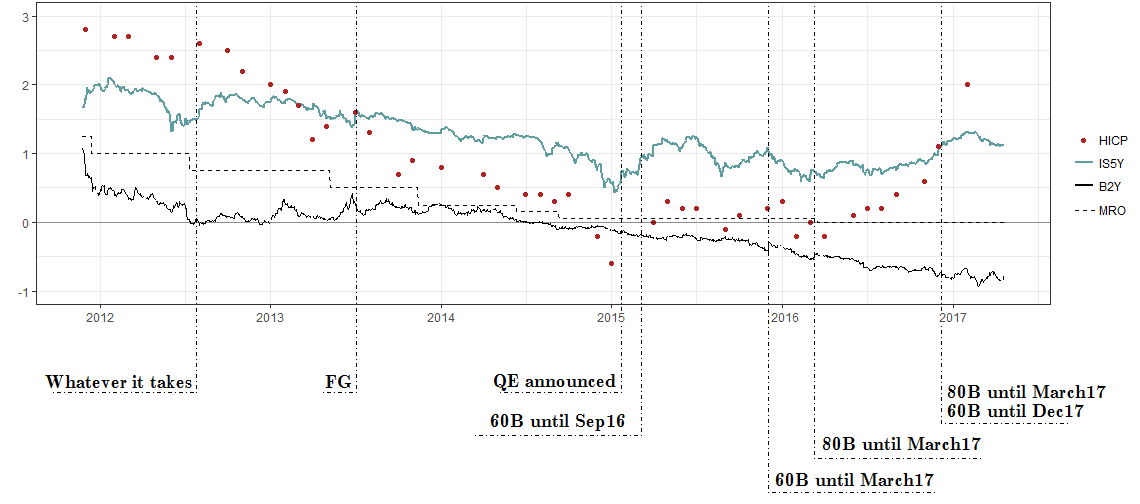

Our paper empirically investigates the impact of forward guidance announcements on inflation expectations in the Eurozone. The ECB first resorted to forward guidance on July 4, 2013 thereby expanding its array of unconventional policy instruments in the vicinity of the zero-lower bound. We use an ARCH model and identify forward guidance shocks as changes in the 2-year nominal ECB yield on specific announcement days to measure changes in daily inflation swaps of different maturities. In the process, we also separately identify the effect of quantitative easing and interest rate change announcement shocks. We find that forward guidance was successful in reviving inflation expectations in the medium to long term. Analyzing the transmission channels of forward guidance, we find evidence that both a reanchoring channel and a portfolio effect might have been at play.

Sources: authors’ calculations and Thomson Reuters Datastream

Conclusions:

Forward guidance shocks have a strong impact on inflation expectations with a one point decrease in 2-year nominal ECB yields pushing inflation expectations 37bps upwards five years ahead with high significance. Normalizing, a negative shock of one standard deviation in ECB yields had a 11bps positive impact. In Campbell’s terminology (Campbell et al. (2012)), market participants’ interpretation was Odyssean. Thereby, we broadly match the results found by Hubert & Labondance (2016) for the Eurozone. Since the impact persists at all horizons, albeit with decreasing amplitude, we suggest that a reanchoring channel à la Andrade et al. (2015) explains the bulk of the transmission. ECB forward guidance announcements have thus been effective in reducing the growing gap between agents’ beliefs in future monetary policy and ECB’s targets. Our results are also consistent with a portfolio effect à la Hanson & Stein (2015). We also document that QE announcements were more effective in amplitude than forward guidance announcements, probably through a reduction in the term premium.

In contrast, studies run by Nakamura & Steinsson (2013) or Campbell et al. (2012) suggested a larger Delphic channel was at play in the US. More precisely however, they found that their results were lower than those predicted by a New Keynesian model with sticky prices. Thus, a natural extension of this paper would be to explore how our results would compare to the predictions of a New Keynesian model. Another approach would be to build a counter-factual for inflation expectations in the absence of forward guidance. In any case, given that the ECB implemented forward guidance at a time of heightened uncertainty and while long-term inflation expectations were dropping, there are reasons to believe it could have been more efficient in the Eurozone than in the US.

On the theoretical side, it is important to understand the transmission mechanisms of forward guidance within a structural model. This would allow to understand the potential gap to empirical outcomes. A number of authors have already striven to embed forward guidance within New Keynesian models and it is still an active area of research. The objective is then to derive an optimal policy function for further times of monetary policy management under the ZLB constraint.

To complete the policy recommendation, one needs to weigh out the benefits of forward guidance against its undesirable side-effects. Poloz (2014) suggested that successful forward guidance could results in increased future volatility when restoring conventional communication. Campbell et al. (2012) highlighted that central bank commitment could have a cost in terms of inflation or credibility. It would then be interesting to assess the negative externalities of forward guidance.

References:

Andrade, P., Breckenfelder, J., De Fiore, F., Karadi, P. & Tristani, O. (2015), ‘The ECB’s asset purchase programme: an early assessment’, ECB Working Paper (1956).

Campbell, J., Evans, C., Fisher, J. & Justiniano, A. (2012), ‘Macroeconomic Effects of Federal Reserve Forward Guidance’, Brookings Papers on Economic Activity 43(1), 1–80.

Hanson, S. & Stein, J. (2015), ‘Monetary policy and long-term real rates’, Journal of Financial Economics 115(3), 429–448.

Hubert, P. & Labondance, F. (2016), ‘The effect of ECB Forward Guidance on Policy Expectations’, Sciences Po publications (30).

Nakamura, E. & Steinsson, J. (2013), ‘High frequency identification of monetary non-neutrality: The information effect’, NBER Working Paper (w19260).

Poloz, S. (2014), ‘Integrating uncertainty and monetary policy-making: A practitioner’s perspective’, Bank of Canada Discussion Paper (2014-6).

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Alfredo Andonie, Andrea Greppi, Ece Yagman, Lorenzo Pisati and Moritz Degler

Master’s Program:

Economics

Paper Abstract:

We investigate the effects of intellectual property products capital in the evolution of the labor share for five European countries. Using post-revision national accounts data, we construct a benchmark labor share with the contribution of both, traditional and IPP capital, against which we measure a counterfactual LS which isolates the effects of IPP. We report that the labor share in Austria, France, Germany, and Spain has been consistently declining, with high variation across countries. Our results show that part of this decline is explained by the inclusion and growing importance of IPP capital in the economy. A closer look at France reveals that the main channels through which IPP has an impact on the labor share are a higher depreciation rate and investment flow relative to traditional capital.

Conclusions:

Our analysis of IPP capital and its impact on the LS reveals three main findings. First, we observe a decline in the LS of Austria, France, Germany and Spain, part of which is explained by the impact of IPP capital on aggregate income. Second, a cross-country comparison discloses great variation in both the magnitude at which the LS is falling in these countries and the extent up to which IPP capital can account for such a decline. Finally, a deeper analysis for France, in which we study the dynamics and composition of its aggregate capital, allows us to identify the higher depreciation rate and investment flow of IPP capital as the main channels driving the change in the trend of the LS.

We conclude that, to an extent, the behavior of the LS attests to the transition into more IPP capital-intensive economies. Since the inclusion of intangible capital in the revised European national accounts (ESA 2010), the growing importance of IPP relative to traditional capital has altered essential properties of aggregate capital, such as the depreciation rate. In particular, these changes have translated into new dynamics and ways in which factors are allocated in the economy.

In using revised data, our analysis presents novel evidence for LS dynamics in Europe and its relation with the composition of capital in the economy. From a measurement point of view, it highlights the way in which we have begun to think differently of developments and aggregate indicators. From a theoretical point of view, it compels us to reformulate models that can accommodate these new measurements and their implications for the rest of the economy.

As a final remark, we have not attempted to establish a connection between the LS and inequality. However, the relation between the compensation to labor and the concentration of IPP capital poses interesting challenges for future research. Particularly relevant to this study are the potential ways in which a decline in the LS propelled by an increase in IPP capital maps onto the evolution of inequality.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Mattia Bongini

Master’s Program:

Finance

Paper Abstract:

We present a tradeoff model of capital structure to investigate the sources of adjustment costs and study how firms’ financing decisions determine partial adjustment toward target leverage ratios. The presence of market imperfections, like taxes and collateral constraints, is shown to play a decisive role in the behavior of the policy function of capital and leverage. By means of a contraction argument, we are able to show the existence of a target leverage towards which optimal leverage converges with a speed of adjustment that depends on a firm marginal productivity of capital. Our predictions are consistent with the empirical literature regarding both the magnitude of the speed of adjustment and the relationship between leverage ratios and the business cycle.

Conclusions:

In this work we showed how financial and economic frictions are able to generate a partial adjustment dynamics in leverage policy functions. In the model we studied, the key factors of this phenomenon are collateral constraints (which strike a balance between tax benefits of debt and distress costs) and firm productivity of capital. The latter, in particular, determines the speed of adjustment towards the (state-dependent) target leverage ratio.

Our model fits well several stylized facts of leverage dynamics established by the empirical literature: an example is given by the magnitude of the speed of adjustment, which falls into the confidence intervals estimated by several authors. Another one, is the countercyclical behavior of leverage dynamics with respect to the business cycle, which is due to the fact that in recessions it is easier for the collateral constraint to be binding.

Future work should first address the translation of the hypotheses of Theorem 5.4 on the Lagrange multiplier into assumptions on the components of the model (the production function and the various market frictions). The next step would then be to extend the model to a full general equilibrium model to study thoroughly the effects of preference and monetary shocks on leverage dynamics. Pairing consumers’ utility maximization with firms’ financing problem would also allow to study the interaction between expected returns and partial adjustment: in such framework, the collateral constraint should probably be replaced by several credit rating inequalities determining both firm specific discount rates and target leverage ratios.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Saga Gudmundsdottir, Olafur Heidar Helgason, Moritz Leitner, Clíona McDonnell and Alexander Schramm

Master’s Program:

Master in Economics and Finance

Paper Abstract:

This paper investigates whether and how geographical distance matters for bank lending within and between countries in the European Union. We estimate gravity-type regressions in various specifications, incorporating novel econometric insights which have thus far not been applied in the context of bank lending. Using recently published, disaggregated data on banks’ credit exposures from the European Banking Authority, we find the elasticity of lending with respect to distance to be -1.42 in our main specification. Controlling for various factors, the negative relationship remains persistent. We argue that this relationship is largely attributable to information costs, though cultural and historical ties between countries, capital requirements, local competition and cross-border trade also play a role. The analysis highlights the enduring influence of factors which prevent full European financial integration.

Conclusions:

The broad narrative that emerges from our analysis is that a combination of deeply-entrenched and policy-based factors determine international bank lending. Firstly, issues that have historically either hindered or facilitated lending – the prohibiting effect of distance in gathering information about potential or current borrowers, and the ties between societies brought about by cultural closeness, trade or direct investment – remain significant predictors of banks’ current stocks of outstanding loans within the EU. Secondly, some of the issues that have recently been under close scrutiny by European policymakers – capital requirements and market competition – also impact lending decisions.

Our analysis has important implications. Although we have not tested directly for the current state of financial integration in the banking sector in the EU, our results imply that a borderless single market for bank loans has not yet been achieved. Despite the progression of financial market integration across the EU, distance continues to be a deterrent to international bank lending on the European level. While some of the underlying mechanisms, particularly cultural and historical ties, are difficult to address politically, others provide scope for intervention by policymakers seeking to further progress the European integration project.

Although technological advancements may have improved transparency and eased the procurement of information and communication between bank and client, it seems they have not yet eliminated information costs in banking. There is room for new technologies that would further reduce the cost of verifying and monitoring clients to allow banks to underwrite more loans internationally. Although it is beyond the scope of this paper to provide a normative analysis of optimal EU policy, we have shown that both government ownership of competing banks and differences in national capital requirements act as deterrents to lending. The key areas we have identified could be targeted to advance the goal of further financial integration in bank lending across the EU.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Lukas Grimm, Jonathan Haynes and Daniel Schmitt

Master’s Program:

Finance

Paper Abstract:

This Project evaluates the forecasting performance of a Brownian Semi-Stationary (BSS) process in modelling the volatility of 21 equity indices. We implement a sophisticated Hybrid Scheme to simulate BSS processes with high efficiency and precision. These simulations are useful to price derivatives, accounting for rough volatility. Then we calibrate the BSS parameters for the realised kernel of 21 equity indices, using data from the Oxford-Man Institute. We conduct one- and ten-step ahead forecasts on six indices and find that the BSS outperforms our benchmarks, including a Log-HAR specification, in the majority of cases.

Conclusions:

This project confirms the findings of Gatheral et al. (2014) and Bennedsen et al. (2016) that volatility is indeed both rough and persistent across a wide range of equity indices. We have explored the advantage of using a Brownian Semi-Stationary (BSS) process to model volatility enabling the user to calibrate both stylised facts in contrast to previous generations of fractal processes, like Fractional Brownian Motion. We have successfully implemented simulation methods so that a BSS process can be incorporated within a continuous time asset pricing equation to price options and other exotic derivatives. We then calibrated the parameters for the BSS model using the realised kernel of 21 equity indices. Our parameter estimates confirm the expected roughness and persistence in the series. The parameter for roughness, α, was quite stable across the cross-section of indices, but fluctuated over time. α averaged -0.37 and ranged from −0.33 to −0.42, implying much more roughness than the α = 0 implied by Standard Brownian Motion. Estimates of the long memory parameter, λ, were less stable, ranging from 0.0041 to 0.0230. We identify an issue when using MoM estimation that suggests MoM may be sub-optimal for BSS-Gamma forecasting. We forecast with six indices that cover a broad geographical spread and have stable lambda estimates. For the one-step ahead forecast we find that the BSS model outperformed two of our three benchmarks consistently under both MSE and QL loss functions. The BSS beat the Log-HAR benchmark in the case of the index with the longest memory, while it was slightly worse for the other five indices. For the ten-step ahead forecast, under the MSE loss function, the BSS model outperformed all benchmarks consistently for five out of six indices. Under the QL loss function the BSS outperforms all benchmarks, and this outperformance is always statistically significant.

Areas for further research would include investigating the forecasting accuracy of the BSS Power Kernel using a wider range of asset class, such as commodities, real estate funds and foreign exchange rates. Further robustness checks could test the performance of BSS against the family of fractional volatility models. It would also be interesting to further explore the relationship of ξ and its link with the variance swap curve.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2017. The project is a required component of every master program.

Authors:

Ignatius Barnardt, Golschan Khun Jush, Thies Wollesen, Samuel Hayden and Eva Sotosek

Master’s Program:

Economics and Finance

Paper Abstract:

We investigate a possible gender gap in returns to education using data from the World Bank’ STEP program for seven developing and emerging countries. We control for cognitive skills, non-cognitive skills and parental education – previously unobserved due to unavailability of data – to investigate how this heterogeneity is playing a role in estimating the gender differential in educational returns. We also model selection using the Heckman two-step estimation procedure to examine whether selection may be driving this phenomenon. Our findings suggest that gender gaps in returns to education are not as prominent in the countries in our sample as previously suggested. We also find that controlling for unobserved heterogeneity on the one hand, and selection on the other, has different effects in different countries, highlighting the importance of understanding individual countries’ labour markets in detail before drawing conclusions regarding the existence of a gender gap in returns to education.

Conclusions:

This paper explores gender gaps in returns to education for seven developing and emerging countries. First, we investigate the existence of such a gap in a standard Mincerian framework. We find a significant returns gap in only two countries, namely Ukraine and Ghana, while the estimates for the other countries are centred relatively tightly around statistically insignificant point estimates close to zero. Using quantile regressions to dig deeper does not materially affect our findings, although it does allow us to specify that the returns gaps estimated for Ghana and Ukraine are significant at two out of three quartiles of the wage distribution, and that in Vietnam there is a small but significant returns gap at the upper two quartiles of the distribution. These findings are important in providing context for the existing literature, showing that returns premiums in favour of females are not universally prevalent in developing countries for urban wage workers. This suggests that where large, significant returns gaps have been found in the literature, this seems to be driven to a large extent by other segments of the labour market.

Second, we use our novel dataset to analyse the extent to which controlling for previously unobserved heterogeneity, namely cognitive skills, personality traits and family background, affect OLS estimates of the returns gap. We find that controlling for these STEP variables does not materially affect our baseline estimates for Bolivia, Colombia, Georgia, Kenya and Vietnam (where the estimated gap remains insignificant and close to zero), or for Ukraine, where the estimated gap is of similar magnitude and remains significant. Only in Ghana we find that adding the STEP controls has a material effect, reducing the point estimate of the gap substantially and rendering it insignificant. The results of the quantile regressions qualify this finding somewhat, showing that controlling for the STEP variables does make a difference for estimates of the gap at certain quantiles of the distribution in Ukraine and Vietnam. Overall, our finding regarding the importance of these sources of previously unobserved heterogeneity is cautiously negative: although they do appear to make a small difference for the level estimates and have an important effect in Ghana, they do not appear to be universal sources of endogeneity in estimating the returns gap for urban wage workers.

Third, we examine the importance of controlling for selection in estimating the returns differential using the Heckman two-step procedure, dropping Kenya from our sample due to missing data. Here we find that after controlling for selection, our point estimates of the returns gap remain insignificant in Ghana, Georgia and Vietnam, albeit with a relatively high point estimate in Georgia. Similarly, our estimate of the returns gap in Ukraine does not change considerably and remains significant. In contrast, we obtain higher and significant point estimates of the returns gap in Bolivia and Colombia. As explained above, this somewhat counterintuitive result is due to positive selection of females into employment in Bolivia and Colombia, and the positive relationship between education levels and probability of employment. Interestingly, in the two countries where selection appears to be important, we found earlier that controlling for the STEP variables did not have an observable effect. Our findings therefore suggest that it is likely to be important to control for selection when estimating returns gaps in developing countries, even if only to exclude the possibility of selection bias. In addition, our approach suggests that selection is likely to operate through channels other than cognitive or non-cognitive abilities, or parental background.

Taken together, our findings show that, at least for urban wage workers in the countries in our sample, a returns premium for females may not be as prevalent as previously suggested. We also find that controlling for potential sources of endogeneity, such as unobserved heterogeneity and selection, substantially changes the estimates of the gender returns gap in three out of seven of the countries in our sample. This highlights the importance of considering these channels to avoid the risk of biased estimation. This paper therefore represents a starting point for more detailed research, which could zoom in on the existence and drivers of returns differentials in individual countries, and overcome some of the limitations of this paper by extending it to rural areas and using samples with a larger number of clusters. These findings are also relevant to policy makers, since they demonstrate the importance of understanding the characteristics and dynamics of each country’s individual labour market prior to making policy proposals.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2016. The project is a required component of every master program.

Measles is currently one of the leading causes of death for young children worldwide. We analyze the impact of measles prevention on later-life human capital outcomes by taking advantage of a measles eradication campaign implemented in 1967 in the United States. We provide evidence with a difference-in-differences design from the 2000 US census micro-sample for the following statistically significant results: the campaign increased completed years of schooling by two weeks, the probability of completing high school by 0.32 per cent and decreased the probability of being unemployed by 4.26 per cent. Due to the exogenous timing of the eradication campaign, we argue that these results can be interpreted causally. To the best of our knowledge our paper is the first one to document adult human capital impacts of early-life measles exposure using a natural experiment.

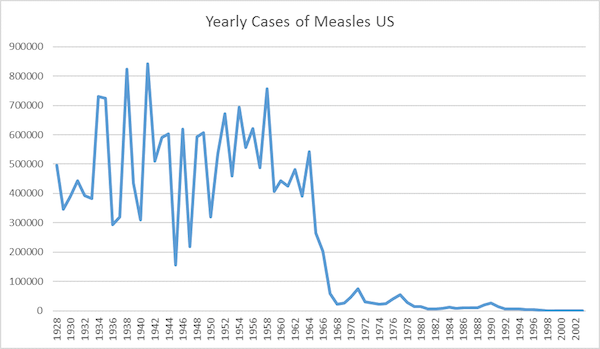

Figure 1: Yearly Cases of Measles in the United States

Empirical strategy:

The 1967 measles eradication campaign led to an unprecedented drop in reported measles exposure in the US, as depicted in figure 1.

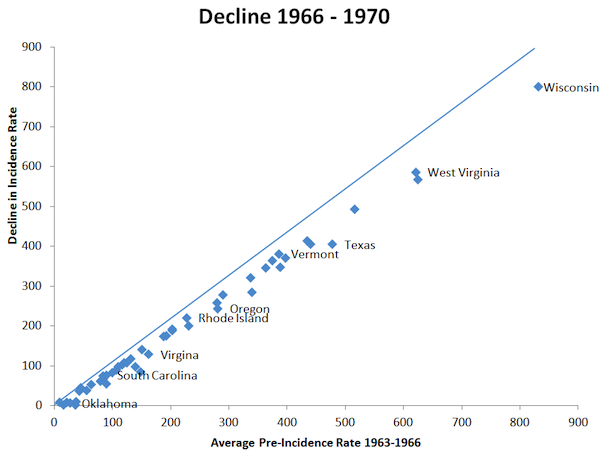

Our empirical strategy uses the fact that there is variation in measles exposure between states prior to the eradication campaign: the decrease in incidence is highest in those states with the highest incidence rates, as depicted in the first stage relationship in figure 2. This allows for a difference-in-differences design, exploring whether the states that had higher prior exposure to the disease gained more in human capital outcomes than the states with less exposure, controlling for pre-existing state-level linear time trends and state fixed-effects among other controls.

Figure 2: Decline 1966-1970

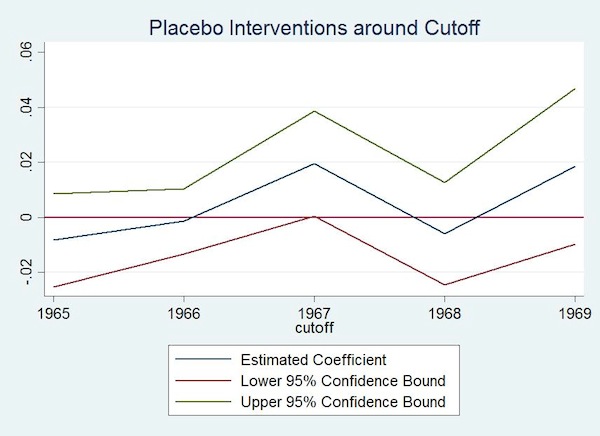

We also perform placebo interventions to test the robustness of our results. As depicted in figure 3, the only positive and statistically significant impacts are found for 1967, the actual intervention year. This lends more support to the causal interpretation of our results.

Figure 3: Placebo Interventions Around Cutoff

Conclusion:

In this paper we show suggestive evidence that exposure to a previously common childhood disease can have negative impacts on educational attainment in adulthood, although the effect sizes are not large. This finding strengthens the literature on the early-life origins of human capital.

Our results are for the most part relevant for developing countries, many of which have not yet achieved the vaccination levels required for herd immunity.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.