On November 11, 2020 the first day of the ECB Forum on Central Banking began with three exciting talks on how shifts in the global economy have changed the game for central banks worldwide. Among the distinguished guest speakers at the Forum was UPF, CREi, and Barcelona Graduate School of Economics Research Professor, Jordi Galí. While the ECB had him slated to speak on the “Inflation Objective, Structural Forces, and Central Bank Communication,” Professor Galí spent his presentation focusing predominantly on inflation targeting at central banks and whether it should be revised going forward.

Watch the ECB Forum panel discussion with Jordi Galí, Volker Wieland, and Annette Vissing-Jørgensen, chaired by Philip Lane on YouTube

His presentation spoke directly to an ongoing debate amongst academics and financial-market watchers, as there have been structural changes in the economy since the last update of the ECB’s policy in 2003. Structural changes are a normal function of an economy as it progresses along with society, though it has some troublesome side effects. Most concerningly, they reduce the effectiveness of policy in alleviating economic downturns by influencing the transmission mechanisms of monetary policy. This raises the challenge for policymakers in picking the best policy.

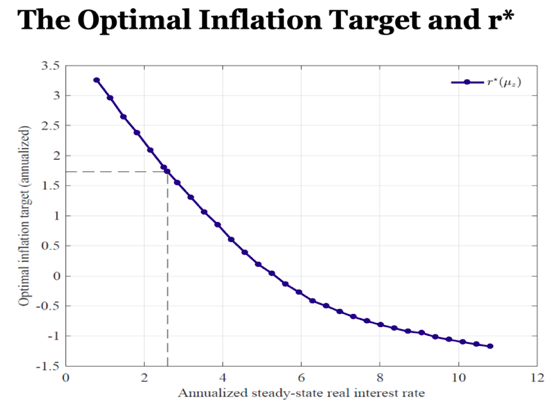

These structural changes ultimately centre around one crucial variable that is influenceable by central banks. The Steady-State Real Interest Rate, colloquially known as R*. Central banks will be constrained by this rate and hit the zero lower bound sooner if they withhold from changing the inflation target – as argued by Jordi Galí in his presentation. A lower R*, as is being observed, necessitates a higher inflation target so that monetary policy (done through a changing of the interest rate) will have less incidence of the zero lower bound and thus reducing the chance of ineffectiveness.

This is obviously an urgent issue faced by policymakers worldwide during the ongoing COVID-19 crisis from the forefront of monetary economics research, yet what Professor Galí was able to do was bring it back to the basics of economics. He emphasised how the models are built on assumptions, and if assumptions change – as the data indicate they have – then the framework for thinking about these issues need to be updated.

In this spirit, Professor Galí proposed three potential policy changes for central bankers to consider in light of the ECB strategic review: he proposed more countercyclical fiscal support; changing to average inflation targeting; or a higher inflation target from its current position of “below or at 2%”. He acknowledged the challenges and potential pitfalls of all these policies, while also speaking to their potential improvement upon the current policy.

It was great to see a Barcelona GSE professor invited to speak at such a prominent and interesting event held annually and frequented by policymakers and academics working on some of the most challenging issues in central banking. It highlights the quality of research that is being done at Barcelona GSE and the quality of the professors conducting that research being sought after by policymakers.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

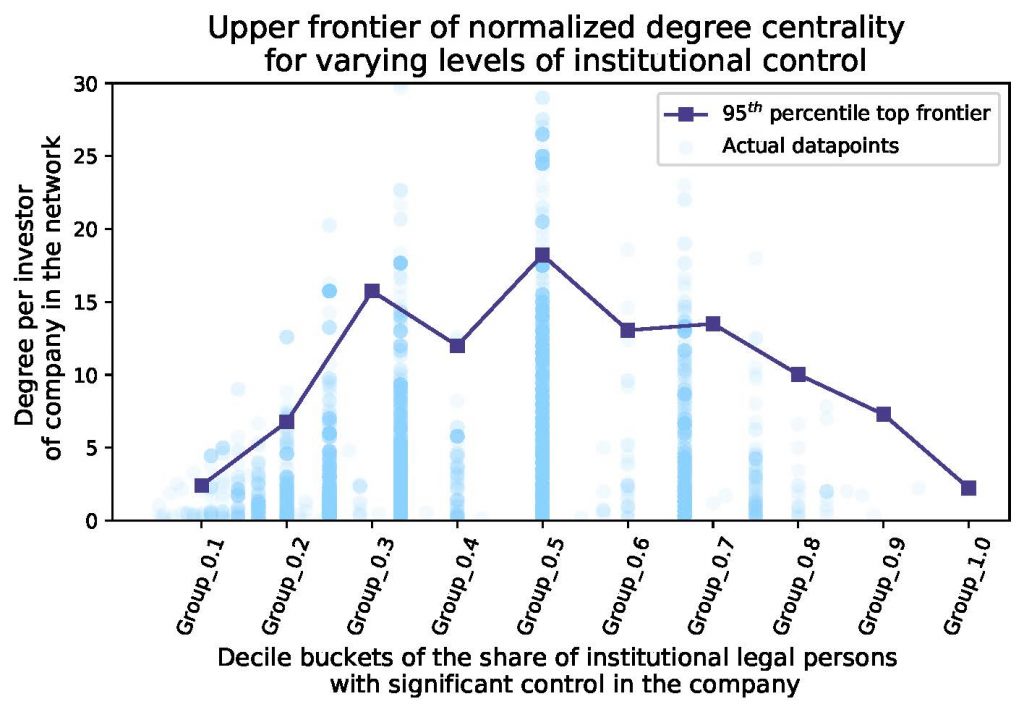

In this thesis project I analyse labour flow networks, considering both undirected and directed configurations, and company control networks in the UK. I observe that these networks exhibit characteristics that are typical of empirical networks, such as heavy-tailed degree distribution, strong, naturally emerging communities with geo-industrial clustering and high assortativity. I also document that distinguishing between the type of investors of firms can help to better understand their degree centrality in the company control network and that large institutional entities having significant and exclusive control in a firm seem to be responsible for emerging hubs in this network. I also devise a simple network formation model to study the underlying causal processes in this company control network.

Conclusion and future research

Intriguing empirical patterns and a new stylized fact are documented during the study of the company control network, since there is suggestive evidence that the types and number of investors are strongly associated with how “interconnected” a firm is in the company control network. Based on the empirical data it also seems that the largest institutional investors mainly seek opportunities where they can have significant control without sharing it with other dominant players. Thus the most “interconnected”/central firms in the company control network are the ones who can maintain this power balance in their owner structure.

The devised network formation model helps to better understand the potential underlying mechanisms for the empirically observed stylized facts about the company control network. I carry out numerical simulations, sensitivity analysis and also calibrate parameters of the model using Bayesian optimization techniques to match the empirical results. However, these results could be “fine-tuned” at different stages further, in order to have a better empirical fit. First, the network formation model could be enhanced to represent more complex agent interactions and decisions. But also, the model calibration method could be extended to include more parameters and a larger valid search space for each of those parameters.

This project could also benefit from improvements to the utilised data. For example more granular data on the geographical regions could help to understand the different parts of London more and to have a more detailed view of economic hubs in the UK. Moreover, the current data source provides a static snapshot of the ownership and control structure of firms. Panel data on this front could enhance the analysis of the company control network, numerous experiments related to temporal dynamics could be carried out, for example link prediction or testing whether investors follow some kind of “preferential attachment” rules when acquiring significant control in firms.

The relationship between institutions and development is a long-standing topic in economic research. However, economists have tended to only evaluate formal institutions (such as laws and property rights), neglecting the informal (like conventions and norms). This overspecialisation precludes the analysis of ideas and ideologies. Without considering these abstract drivers of development, the space for ethically and politically dangerous explanations of success appears (such as for genetic reasons).

Contrary to recent literature, I argue that informal constraints are actually the basis of institutions and therefore the real generators of growth and development. I show this by examining revolutions – the cauldrons where new systems, ideas, and conventions begin, and old ones end.

The illusion of separation

Scholars of comparative development have noted the increasing divergence between developed and developing countries: the gap between Northern and Southern Europe and the underdevelopment of the Middle East and sub-Saharan Africa being major examples. Several theories attempt to explain this divergence, considering possible factors such as geographical characteristics and institutional differences. Notably, comparative development has even been attributed to levels of genetic diversity (Ashraf & Galor, 2013).

In particular, the crucial historical link between institutions and development is well known. Famous examples include the advantage of limited royal power (Acemoglu, 2005); reformed constitutional arrangements and strengthened property rights (North & Weingast, 1989); and the balance of power between merchants and princes (De Long, 1993). Yet, these studies put their emphasis on formal rules, neglecting the norms, ideas and ideologies that underwrite them.

The latter are fundamental elements of institutions as they influence formal rules. In a seminal contribution to institutional economics, North (1994) distinguishes between two forms of institutions: formal rules (constitutions, laws, property rights etc.) and informal constraints (norms of behaviour, conventions, self-imposed codes of conduct etc.). In a later work, he argued that institutions evolve incrementally and successively over time (North, 1991). When those two forms are approached as two separated sources of institutions, the role of informal constraints in institutional evolution will be missed, throwing a veil over a core aspect of institutions and leading us to fallacious conclusions about the key determinants of growth and development.

Similarly, Karl Popper (1945) distinguishes an open society from a closed society based on whether a distinction exists between normative laws and natural laws. Where there is none – what Popper calls a closed “tribal society”– taboos and conventions act as if they were natural law. This gives them a powerful role in society and a fundamental role in development. By creating formal laws, societies recognise the distinction between norms and natural laws, weakening the effect of conventions (although, as we will see, they still act through both formal and informal laws).

Both North and Popper agree on this chronological development of institutions meaning a better understanding of causation is needed. Myrdal (1978) convincingly argues that the mechanisms of social systems are determined by an endogenous cycle of causation that affects the distribution of power in a society and economic, social and political stratification). This means that a change in informal constraints will alter formal rules, which will then return to affect the former. Therefore the scaffolding of institutions consists of norms of behaviour, conventions and self-imposed codes of conduct.

The revolutionary crevasse

Just as a crevasse provides a glimpse deep into the ice, revolutions open a window to the creation and destruction of social systems. Revolutions are beloved by social scientists (especially in institutional economics) as they provide natural experiments to investigate causal effects. They can shed some light on the importance of norms and convention, as well as their relationship with ideas, ideologies and leaders.

In the literature, for example, Acemoglu et al. (2008) and North & Weingast (1989) have respectively examined the impact of the French Revolution on development and the Glorious Revolution on institutional structure. However, these types of studies have focused only on the secondary changes (in laws and property rights) instead of the initial causes of change (norms and conventions). In this regard, a re-evaluation of revolutions and their characteristics is necessary to observe the initial changes.

Let us first consider which elements prepare amenable conditions for the emergence of revolutions. Gottschalk (1944) identifies three broad factors:

demand for change stemming from (a) personal discontent and (b) social dissatisfaction

hopefulness derived from (a) popular programs of reform and (b) a leader

weakness of the conservative forces – perhaps the most important.

Demand comes from widespread provocations (corruption, taxation, poor infrastructure etc.) which generate social dissatisfaction. Yet, demand by itself is not sufficient for the revolution. Some hope of success is also needed. This comes from programs of reform, as provided by the Voltaires and Rousseaus, the Lockes and Ademses, and the Marxes and Kropotkins (Gottschalk, 1994). However, tuneless emphasis on widespread provocations that are based on the formal rules underestimates the phycological mechanisms that are mainly based on informal constraints.

Personal discontent (arising for idiosyncratic reasons) only appears at the individual level yet plays an essential role in generating the leaders of revolutions. These leaders then support the new-born ideas and ideologies based on the program of reform which has a multiplier effect by coherently spreading revolutionary sentiment. This is crucial once we think of revolutions as risky events over which individuals have varying valuations of the possible outcomes. Gneezy et al. (2006) show that individuals, faced with a complex choice, may choose to stay in the old system if they value the risky benefits of revolution less than the worst outcomes of rebelling. However, once the revolutionary “lottery” is based on intellectuals’ programs of reforms and explained by leaders it becomes easier to code.

In this way, agents facing complex task (in this case revolution), might act following the leader through many of the channels identified by behavioural economics such as Tversky and Kahneman’s simple heuristics, Walker and Wooldridge’s conventions and Shiller’s narratives. These share common features which affect the majority’s decision-making processes – especially when tasks are complex.

This process is essential to notice the importance of informal constraints and how they become formal rules since leaders are the symbol of ideologies and ideas. As Axelrod indicates norms precede laws and laws strengthen norms. After the success of the revolution laws strengthen the norms through formalization. And after social conventions are entrenched, they become thoughtlessly accepted by individuals (Epstein, 2001).

As with the example of revolutions, before a change in the formal rules, an ideological revolution has occurred when intellectuals provide the programs of reforms. The ideas become conventions during the revolution, changing societal expectations. Notions of equality and liberty – in the case of the French Revolution – became the convention as the system was upended. The relationships between ideas, ideologies, norms and leaders encourage us to take them into account when evaluating growth and development.

Conclusion

I have argued that ideas, norms and ideologies are the initial drivers of development and have had an immense effect on our civilizations. However, traditional political economy’s overemphasis of formal rules fails to capture this. The insularity of this approach is highlighted by examining Revolutions, which provide evidence in favour of more inclusive definitions of institutions and the importance of ideas, ideologies and leaders in creating social systems. Therefore, I contend that a more holistic approach to analysing development is required otherwise alternative and ill-founded explanations of growth with remain.

References

Acemoglu, D., Cantoni, D., Johnson, S., & Robinson, J. A. (2008). From ancien regime to capitalism: the French Revolution as a natural experiment. Natural Experiments…, op. cit, 221-256.

Acemoglu, D., Johnson, S., & Robinson, J. A. (2005). The rise of Europe: Atlantic trade, institutional change, and economic growth. American Economic Review, 95(3), 546-579.

Ashraf, Q., & Galor, O. (2013). The ‘Out of Africa’ hypothesis, human genetic diversity, and comparative economic development. American Economic Review, 103(1), 1-46.

Axelrod, R. (1986). An evolutionary approach to norms. The American Political Science Review, 1095-1111.

De Long, J. B., & Shleifer, A. (1993). Princes and merchants: European city growth before the industrial revolution. The Journal of Law and Economics, 36(2), 671-702.

Epstein, J. M. (2001). Learning to be thoughtless: Social norms and individual computation. Computational economics, 18(1), 9-24.

North, D. C. (1991). Institutions. Journal of Economic Perspectives, 5(1), 97-112.

North, D. C. (1994). Economic performance through time. The American Economic Review, 84(3), 359-368.

North, D. C., & Weingast, B. R. (1989). Constitutions and commitment: the evolution of institutions governing public choice in seventeenth-century England. The Journal of Economic History,49(4), 803-832.

Popper, K. R. (1945). The open society and its enemies. Routledge, London.

Myrdal, G. (1978). Institutional economics. Journal of Economic Issues, 12(4), 771-783.

Gottschalk, L. (1944). Causes of revolution. American Journal of Sociology, 50(1), 1-8.

Competition and Market Regulation master project by Silvia Brumana and Roger Medina ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Asymmetric pricing in the retail fuel market describes the situation in which retail prices are adjusted quickly in case of positive shocks in the wholesale costs, whereas the adjustment is much slower in case of negative ones. This asymmetry in the reaction of retail operators is captured by the well-known expression rockets and feathers. By relying on a reduced version of a database used in Moral and Gonzalez (2019) containing the series of diesel prices in Spain and Brent prices for the period 08/2014-06/2015, we address the following research question: how did the fuel prices of the retail gas stations in a subset of Spanish provinces react in this period to changes in the price of Brent? In order to answer this question, we construct a pricing equation that takes into account all the possible factors that can affect pricing with the aim of isolating the effect of negative shocks and the effect of positive shocks in the price of Brent on the price of gasoline of the various Spanish operators. Then, we check whether the difference between these two effects is statistically significant to see whether there were asymmetric reactions. Furthermore, since the common rocket and feathers phenomenon could be considered as a collusive device, and since in the period covered by the database a cartel was active among the main fuel companies in Spain, we also investigate the relation between asymmetric pricing and competition.

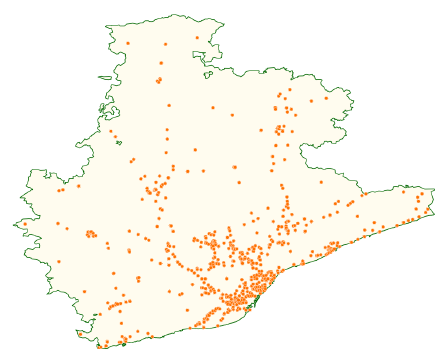

Figure 1. Spatial distribution of gas stations in Barcelona

Conclusions

The aim of our project was to capture the presence of asymmetric pricing in nine Spanish provinces between 2014 and 2015 by taking into account the fact that during the period considered the CNMC fined five of the largest oil companies in Spain for collusion. To do this, we estimated an Error Correction Model for each province by accounting for both panel heterogeneity and cross-sectional dependence to capture both the short-run and the long-run relation between the retail diesel prices and the Brent price.

Our results show that there exists a correction mechanism that pushes the retail prices back to the long-run equilibrium relation with the Brent in case of shocks, even if the magnitude of the correction may be overestimated potentially because of the pattern of the retail fuel price in the period before the fine of the CNMC became public.

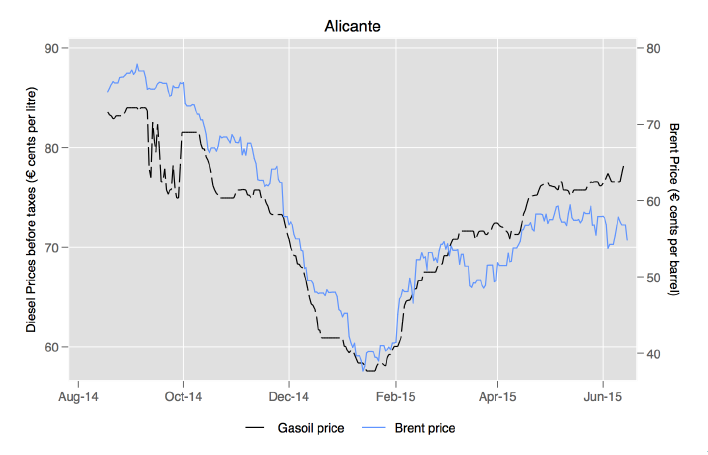

Figure 2. Evolution of the Brent price and the average retail fuel price in Alicante in the period considered. Note that the CNMC fined the major oil companies in Spain in February 2015.

As far as the short-term adjustments are concerned, the results are less clear because of the lack of significance of most of the coefficients; this is potentially due both to the presence of imperfect collinearity arising from issues with the lag selection in each province as well as to the already mentioned patterns of the diesel prices. Furthermore, as to what concerns the effect of the fine of the CNMC, the results show that in many provinces there is some variability in the pricing of the gas stations after February 2015 that is not accounted for in the rest of the model. We may not confidently state that this is entirely due to the fine of the CNMC: in fact, the related coefficient may capture some variability due to the attempts of firms of recovering the losses incurred before the fine was issued. Consequently, we suggested that we may need to first solve the issue of the lag selection and then, if the effect of the fine is still significant, we may eventually add some control for the profitability of the firms, even if this would imply expanding the database because of the absence of variables capturing the evolution of profits of the firms observed.

To conclude, although our analysis may still need some refinement especially in the lag selection procedure, we suggest that the relation between asymmetric pricing and competition is worth exploring. In addition, it would be also interesting to understand whether aggregating the data in the database we used at a weekly level, for instance, would lead to different estimates and insights or would simply lead to biased findings as suggested in the literature.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

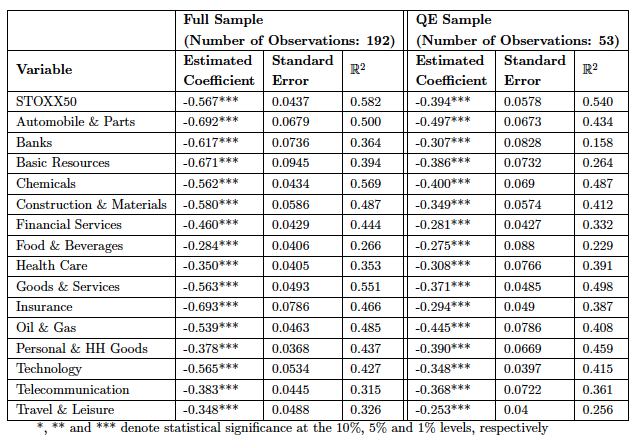

The Global Financial Crisis prompted central banks to adopt unconventional monetary policies such as the asset purchase programs. In our thesis, we analyze whether securities purchases carried out by the ECB have had an impact on stock prices and whether these effects vary across sectors. We decompose the central bank announcement surprises into two opposing effects, a pure monetary policy shock and an information shock. We find that the pure monetary policy shock has indeed significant effects on stock prices across all sectors, suggesting that controlling for the information shock is important when analyzing the effects of central bank announcements.

Conclusions

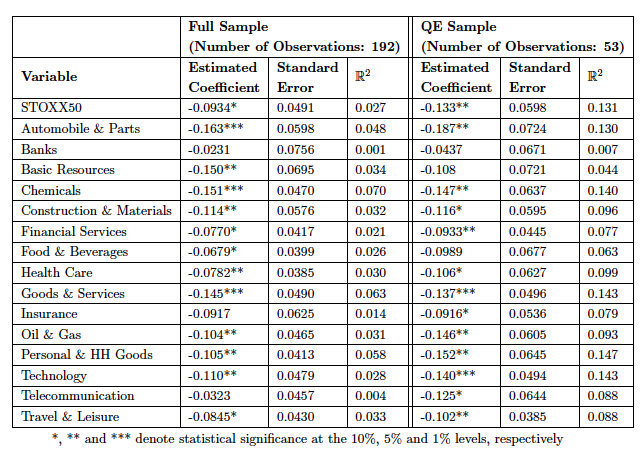

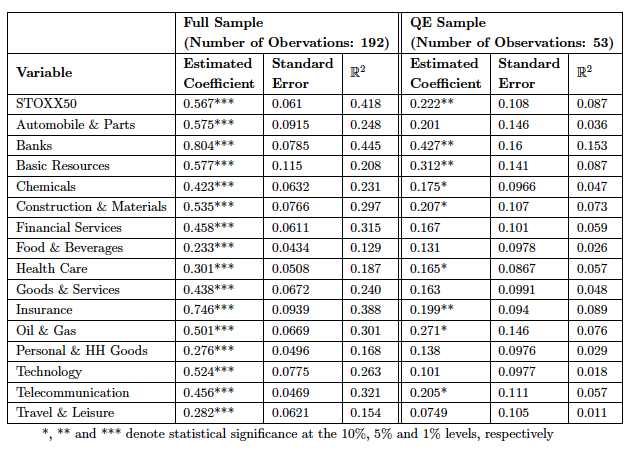

In our paper, we analyzed the effects of Quantitative Easing on stock prices in the Euro Area. Adding to previous literature, we not only analyzed the effect on the benchmark index but considered sectoral indices as well in order to allow for heterogeneous responses across different industries. Using the methodology of Altavilla et al. (2019), we first extracted the QE factor from each ECB press conference, starting from 2002. In a first exercise, we used the QE factor as a regressor to explain stock price changes on the press conference days. In line with asset pricing theory, we find negative effects of the QE shock on all sectoral stock price indices, yet, significance differs.

Overall QE Shock

In a second step, we decomposed the shock into two components, using sign restrictions. The two shocks are referred to as information shock and pure monetary policy shock and are characterized by positive co-movement and negative co-movement of interest rates and stock prices, respectively.

Information Shock

Pure Policy Shock

We looked at these two components separately in order to assess whether insignificant results obtained in the overall regression may be due to the two components off-setting each other, a presumption which was confirmed. Furthermore, we find that the pure monetary policy shock has significant effects on stock prices across all sectors, while the information shock appears to be more important on specific sectors, which are more related to financial markets. A more in-depth analysis of the reasons for this heterogeneity could provide further insight into the effects of QE on stock prices. Moreover, repeating this exercise with a larger sample and intraday stock price data might yield improved results. Other extensions could be the analysis of specific sectors for various countries.

A newsletter about supply and demand by Brian Albrecht ’14 (Economics of Public Policy)

Economic Forces is a new weekly newsletter by Brian Albrecht ’14 (Assistant Professor of Economics, Kennesaw State University) and Josh Hendrickson (Associate Professor of Economics, University of Mississippi).

“We are both professors of economics with a passion for what used to be called price theory. This newsletter is our attempt to work through and clarify points in price theory,” the authors explain in the newsletter’s introduction.

“You’ll have to pry supply and demand from my cold, dead hands.”

That’s the title of Brian’s first post to the newsletter. In it, he gives an overview of the Economic Forces project and and “a simple defense of (the increasingly scoffed at by the loudest voices online) supply and demand. “It seems silly to need to defend supply and demand within economics circles,” Brian says, “But it is 2020…”

Economics master project by Pierre Coster, Pia Ennuschat, Raquel Lorenzo, Giacomo Stazi, and Robert Wojciechowski ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

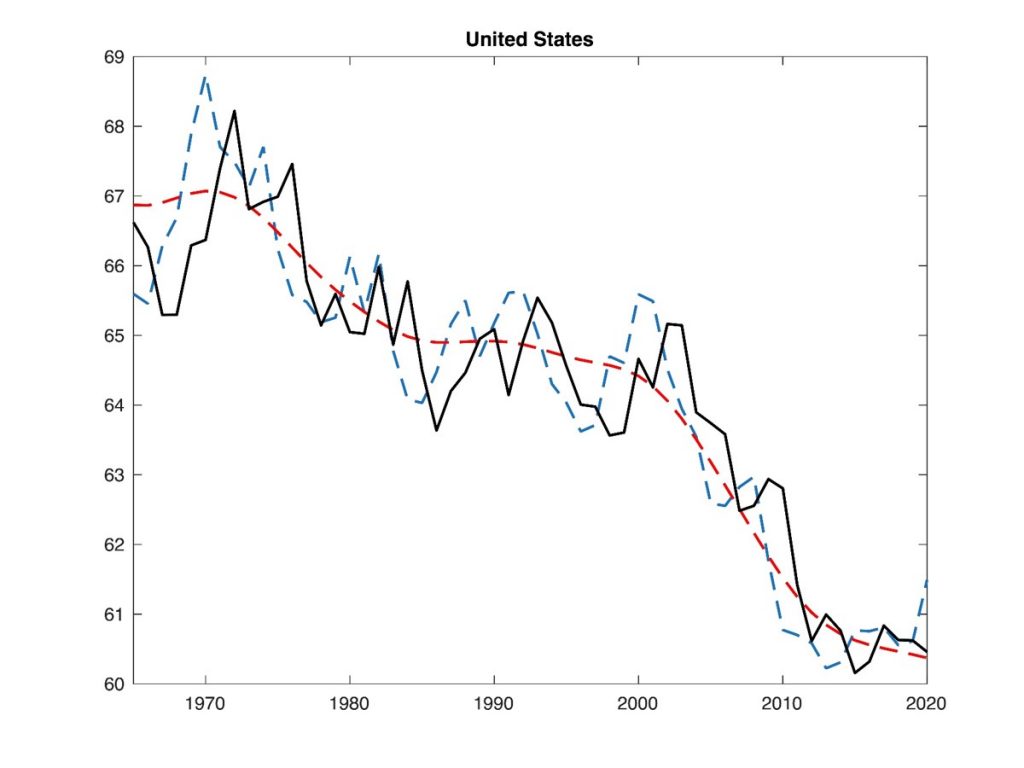

Labor share, once thought to be a constant, has experienced a secular decline in many developed economies. We investigate whether adjustment costs to intangible capital can be used to explain this trend. We develop a simple partial equilibrium model with a profit maximizing firm that produces using a three factor CES production function and faces convex adjustment costs to intangible capital. We find an intuitive expression for the steady state labor share as a function of parameters and the steady state level of investment in intangible capital.

We then run simulations to better understand the behaviour of the labor share in our model. Somewhat surprisingly, we find that adjustment costs do not affect the steady state labor share for any given elasticity of substitution. However, their presence creates a strong relationship between the labor share and the elasticity of substitution. We also find a number of short-run dynamics that are affected by the level of adjustment costs.

Labor share trends over the last 60 years in the United States. Source: AMECO

Conclusions

We find that our model with adjustment costs leads to a very clear relationship between the elasticity of substitution and the labor share. Therefore, one could use it to explain the secular decline in the labor share as a result of a falling elasticity of substitution in presence of convex adjustment costs to intangible capital. However, in our simple model there does not appear to be a meaningful relationship between the level of convex adjustment and the steady state labor share. Moreover, adjustment costs affect a number of interesting short-run dynamics. The level of adjustment costs changes the responsiveness of the labor share to variations in the price of inputs. Lastly in our simple model the volatility of the price process does not alter the steady state labor share, even though it does matter for short-run dynamics.

We see room for further research in the following directions. Our analysis assumes perfectly competitive markets. A model of monopolistic competition in the goods market could lead to long-run effects of the level of adjustment costs on the labor share. Karabarbounis and Neiman, 2013 showed that in such a model price decreases can explain part of the decrease in the labor share. Therefore, analysing the effect of adjustment costs in the context of monopolistic competition seems promising. Another potential avenue is the generalization of the analysis to a general equilibrium setting.

Understanding endogenous changes in wages that were set to be fixed throughout our analysis, could be important in explaining the changes in the labor share.

Vicky Fouka ’10 (Economics) is an editor of this new meeting point for HPE researchers

A map shows the original location of the Broad Street Pump

About the project

Broadstreet is a blog dedicated to the study of historical political economy (HPE). Its goal is to foster conversations across disciplines in the social sciences, namely economics and political science, but also history, sociology, quantitative methods, and public policy. Correspondingly, its editors (and guest contributors) are drawn from these respective disciplines.

Given the boundaries that typically exist across academic disciplines, scholars who work on similar subjects – like HPE – rarely talk to one another or read each other’s work. Our hope in starting Broadstreet is to break down some of these artificial boundaries, generate true cross-disciplinary dialogues, and produce better and more wide-ranging HPE research.

The blog’s name, Broadstreet, is a nod to the legendary John Snow and his study of the 1854 cholera outbreak in London. Snow found convincing evidence for a previously unproven water-born theory of cholera transmission, with a rigorous yet interdisciplinary approach — using detailed socio-economic data, ethnography, historical patterns of disease transmission, and early techniques of causal inference. The Broad Street water pump in London’s Soho district was not only a meeting place for the diverse residents of the neighborhood, but served as the focal point for Snow’s interdisciplinary breakthrough. While the Broad Street pump is no more, the legacy of this innovative research lives on. We hope that Broadstreet will be go-to location for all those with interests in HPE.

Vicky Fouka ’10 (Economics) is Assistant Professor of Political Science at Stanford University. She is an alum of the Barcelona GSE Master’s in Economics and earned her PhD in Economics at GPEFM (UPF and Barcelona GSE).

ITFD master project by Emma Howard, Kean Murphy, Wouter Nientker, Karim El-Ouaghlidi, and Harry Schmidt ’20

Photo: CNN

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Overview

Using a dynamic panel fixed effects model, we find that increases of ODA of above 2% of GDP have significant effects on the economic growth of African countries in the immediate aftermath of severe natural disasters. This is a surprising result because we do not find that ODA in times of relative stability has a significant effect on GDP. This suggests that debt relief, at least through the channel of significant increases in ODA, is an effective instrument in promoting post-disaster recovery, even though its effectiveness in raising economic growth more generally is limited. Since increases in ODA inflows of above 2% of GDP only occurred after 1/3 of the disasters we studied, we recommend that international financial institutions concentrate ODA flows on countries that had been afflicted by severe disasters.

Introduction

One of the biggest challenges facing developing Sub-Saharan African economies is their vulnerability to severe natural disasters such as droughts and floods. Not only do they face on average over 50 disasters a year, but their economies’ over-reliance on agricultural production and weak institutional capacity cause them to experience the effects of these disasters particularly acutely. Worryingly, this vulnerability is likely to rise in the coming years, as the earth warms and climate change increases the number and severity of extreme climatic events.

While it is difficult for countries to prevent natural disasters, since they tend to arise from exogenous climate conditions, they can take steps to mitigate these adverse consequences through post-disaster rehabilitation. To do so, governments require sufficient fiscal space so that they can borrow and spend without jeopardising budgetary sustainability. However, many African countries suffer from persistently high levels of debt, with 33 of the 39 countries in the Heavily Indebted Poor Countries scheme located on the continent. This constrains government spending on humanitarian relief and reconstruction, which can leave countries unable to recover from the devastation.

In view of these twin trends – African economies’ vulnerability to natural disasters and their crippling levels of debt – any channel that reduces a country’s debt burden and hence increases its fiscal space should theoretically encourage faster economic recovery. This suggests that debt relief can be a vital policy instrument in mitigating the negative effects of natural disasters. However, corruption and inefficient resource allocation mean that its effectiveness may be constrained in practice. To explore the role of debt relief further, we employ a dynamic panel fixed effects model across the most severe 25 floods and 68 droughts in Africa from 1978 to 2013. As a robustness check, we also include an Anderson-Hsiao style GMM estimation procedure. We define debt relief as any policy that reduces the need for governments to issue new debt or repay existing debt, particularly in the aftermath of a natural disaster. In the context of this paper, this includes debt forgiveness, debt rescheduling and/or increased official development assistance (ODA). Furthermore, we run two different specifications of debt relief: first, using a dummy variable which indicates any instance of the aforementioned forms of debt relief; and second, using a continuous variable for ODA inflows alone.

Main findings

Surprisingly, when we run our first specification, we find that debt relief in general does not have a statistically significant impact on economic growth. Additionally, ODA inflows in times of relative stability do not have significant effects on economic growth. Instead, they only reduce debt-to-GDP growth, suggesting that they are merely used by governments to pay off existing debt. This is in line with previous research by both Mejia (2014) and Raddatz (2009), who found at most weak evidence that either debt relief in the aftermath of disasters or ODA in general is effective in boosting economic growth.

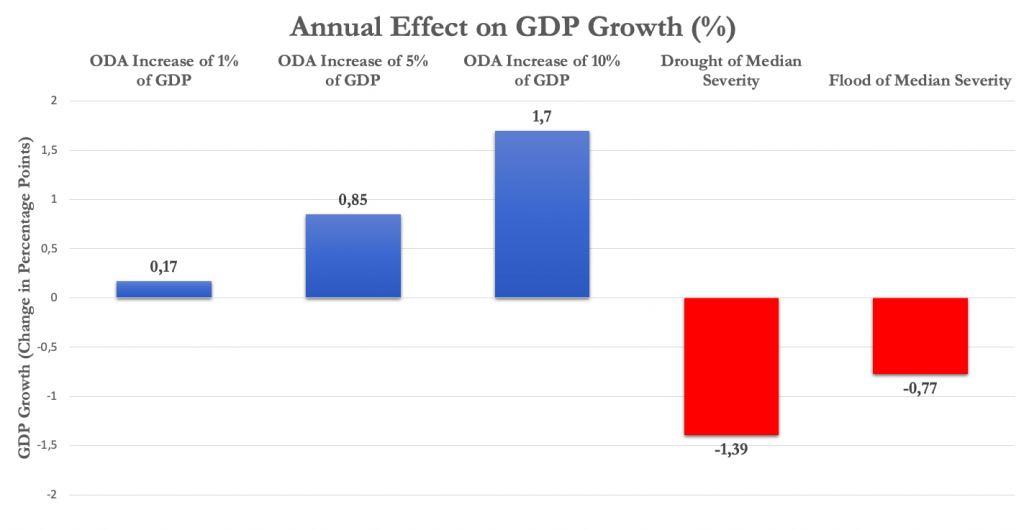

In contrast, we find that increases in inflows of ODA of above 2% of a country’s annual GDP, when provided in the year of or immediately after severe disasters, do have statistically significant positive effects on economic growth (see Figure 1). These findings are similarly observed when we interact our ODA variable with the continuous measure of disaster severity. For a given level of ODA, the effectiveness of post-disaster ODA increases in the severity of the underlying disasters. Furthermore, ODA inflows no longer have statistically significant effects on debt-to-GDP growth. This suggests that, unlike in regular times, ODA flows are used fruitfully by governments after disasters to bolster economic recovery rather than to pay off existing debt.

Figure 1

This is a notable result because it suggests that debt relief, at least through the channel of ODA, is an effective instrument to promote post-disaster recovery. This result differs from that found by previous research because we focus on ODA increases that a) were larger than 2% of GDP and b) occurred in the aftermath of severe natural disasters. This helps us isolate the specific role of ODA in promoting post-disaster recovery from its general effectiveness as a form of economic stimulus to boost growth.

Policy implications

Our findings suggest that policymakers in international financial institutions such as the OECD or IMF should step up efforts to increase ODA inflows to developing countries when severe natural disasters hit. This not only has the direct effect of reducing the loss of lives, but is also vital for poverty reduction by ensuring that these countries return rapidly to their existing balanced growth path. Otherwise, countries risk experiencing persistent economic slowdown and skyrocketing debt due to the disasters, which would in turn lead to a vicious cycle of mounting debt and stagnant growth. Instead, increased ODA flows can substitute for the domestic shortfall in resources available to countries to rehabilitate the economy by providing emergency relief to citizens and rebuilding damaged infrastructure.

Current attempts at mitigating such disasters are relatively limited: in our sample of 92 severe disasters in Africa between 1978 and 2013, large increases of ODA greater than 2% of GDP only occurred after 32 of these disasters. This is surprisingly infrequent, especially considering that we focus only on the largest of disasters which should have ample international media coverage. As highlighted above, larger increases in ODA have greater cumulative effects on the economy, especially for more severe disasters. As this effect is not observed when we study ODA inflows in times of stability or inflows below 2% of GDP, we recommend that existing ODA programmes prioritise large flows to countries which have just suffered from severe natural disasters. This is because the marginal benefit of these targeted flows in promoting development is likely higher than general flows to countries that are relatively stable.

Finally, although our paper focuses on floods and droughts in Africa, we believe that our results can be generalized to other types of disasters. Although further research is needed to fully establish the causal mechanism by which debt relief improves post-disaster outcomes, it is likely that it will have a similar positive impact in rehabilitating economies that face disasters which leave them with high levels of debt and significantly lower budgetary revenue. Most notably, it suggests that significant increases in ODA flows can play a vital role in helping developing economies devastated by the COVID-19 pandemic by allowing them to mitigate its adverse effects.

Mejia, S. A. (2014, July). Debt, Growth and Natural Disasters A Caribbean Trilogy (IMF Working Papers No. 14/125). International Monetary Fund. Retrieved from https://ideas.repec.org/p/imf/imfwpa/ 14-125.html

Publication in PNAS by Katharina Janezic ’16 (Economics) and Aina Gallego (IBEI and IPEG)

Honesty is one of the most valued traits in politicians. Yet, because lies often remain undiscovered, it is difficult to study if some politicians are more honest than others. This paper examines which individual characteristics are correlated with truth-telling in a controlled setting in a large sample of politicians. We designed and embedded a game that incentivizes lying with a non-monetary method in a survey answered by 816 Spanish mayors. Mayors were first asked how interested they were in obtaining a detailed report about the survey results, and at the end of the survey, they had to flip a coin to find out whether they would be sent the report. Because the probability of heads is known, we can estimate the proportion of mayors who lied to obtain the report.

We find that a large and statistically significant proportion of mayors lied. Mayors that are members of the two major political parties lied significantly more. We further find that women and men were equally likely to lie. Finally, we find a negative relationship between truth-telling and reelection in the next municipal elections, which suggests that dishonesty might help politicians survive in office.

Connect with the authors

Katharina Janezic ’16 (Economics) is a PhD candidate in Economics at UPF and Barcelona GSE.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.