In this new publication for the Bank for International Settlements, Egemen Eren ’09 and co-authors Stefan Avdjiev and Patrick McGuire review recent events in FX swap markets in the context of the longer-term trends in the demand for dollars from institutional investors.

Key takeaways

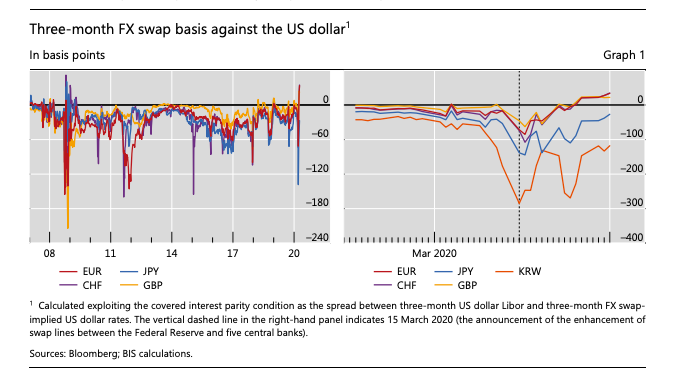

Since the start of the Covid-19 pandemic, indicators of dollar funding costs in foreign exchange markets have risen sharply, reflecting both demand and supply factors.

The demand for dollar funding has grown in recent years, reflecting the currency hedging needs of corporates and portfolio investors outside the United States.

Against this backdrop, the financial turbulence of recent weeks has crimped the supply of dollar funding from financial intermediaries, sharply lifting indicators of dollar funding costs.

These costs have narrowed after central banks deployed dollar swap lines, but broader policy challenges remain in ensuring that dollar funding markets remain resilient and that central bank liquidity is channelled beyond the banking system.

Finance master project by Daniel A. Landau and Gabriel L. Ramos ’19

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

In this paper, we characterize a variety of international financial markets as partially correlated networks of stock returns via the implementation of the joint sparse regression estimation techniques of Peng et al. (2009). We explore a number of mean-variance portfolios, with the aim of enhancing out-of-sample portfolio performance by uncovering the hidden network dynamics of optimal portfolio allocation. We find that Markowitz portfolios generally dissuade the inclusion of central stocks in the network, yet the interaction of a stock’s individual and systemic performance is more complex. This motivates us to explore the time-varying correlation of these topological features, which we find are highly market dependent. Building on the work of Peralta & Zareei (2016), we implement a number of investment strategies aimed at simplifying the portfolio selection process by allocating wealth to a targeted subset of stocks, contingent on the time-varying network dynamics. We find that applying mean-variance allocation to a restricted sample of stocks with daily portfolio re-balancing can statistically significantly enhance out-of-sample portfolio performance in comparison to a market benchmark. We also find evidence that such portfolios are more resilient during periods of major macroeconomic instability, with the results applicable to both developed and emerging markets.

Conclusion and Future Research

In our work, we represent 4 international exchanges as individual networks of partially correlated stock returns. To do so, we build a Graph, comprised of a set of Vertices and Edges, via the implementation of the joint sparse regression estimation techniques of Peng et. al (2009). This approach allows us to uncover some of the hidden topological features of a series of Markowitz tangency portfolios. We generally find that investing according to MPT dissuades the inclusion of highly central stocks in an optimally designed portfolio, hence keeping portfolio variances under control. We find that this result is market-dependent and more prevalent for certain countries than for others. From this cross-sectional network analysis, we learn that the interaction between a stock’s individual performance (Sharpe ratio) and systemic performance (eigenvector centrality) can be complex. This motivates us to explore the time-varying correlation ρ between Sharpe ratio and eigencentrality.

Optimal Weights for Tangency Portfolio Strategy.

Overall, we show that in considering the time-varying nature of partially correlated networks, we can enhance out-of-sample performance by simplifying the portfolio selection process and investing in a targeted subset of stocks. We also find that our work proposes a number of future research questions. Although we implement short-sale constraints, it would also be wise to introduce limits on the amount of wealth that can go into purchasing stocks, as this would help to avoid large portfolio variances. Furthermore, our work paves the way for future research into the ability of ρ-dependent investment strategies to enhance portfolio performance in times of macroeconomic distress and major financial crises.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2014. The project is a required component of every master program.

Realized Volatility Estimation

Authors:

Miquel Masoliver, Guillem Roig, Shikhar Singla

Master Program:

Finance

Paper Abstract:

The main purpose of this study is to try to find the optimal volatility estimator in a non-parametric framework. In particular, this study focuses on the estimation of the daily integrated variance-covariance matrix of stock returns using simulated and high-frequency data in the presence of market microstructure noise, jumps, and non-synchronous trading. This work is structured in three building blocks: (i) price processes are simulated in the presence of jumps and market microstructure noise. This allows us to obtain some insight about the estimators’ performance. (ii) The aforementioned realized volatility estimators are applied to high-frequency data of the S&P 100 stocks of October 27th 2010 using 5-second, 10-second, 30-second, 1-minute and 2-minute time intervals. (iii) We use the estimated covariance matrices to construct the global minimum variance portfolio for each sampling frequency. These global minimum variance portfolios are used to build 30 day ex-post portfolio’s returns and we use the variance of these returns to compare between the performance of the estimators.

Editor’s note: This post is part of a series showcasing Barcelona GSE master projects by students in the Class of 2014. The project is a required component of every master program.

Interest rates after the credit crunch crisis: single versus multiple curve approach

Authors:

Oleksandr Dmytriiev, Yining Geng, and Cem Sinan Ozturk

Master Program:

Finance

Paper Abstract:

For interest rate derivative pricing, 2007 crisis was a turning point. Prior to the crisis, market interest rates showed consistencies that allowed the use of a single curve for both forwarding and discounting. After the crisis, the inconsistencies in the market interest rates led to development of a new method of the pricing interest rate derivatives, which is called Multi-Curve Framework. We studied the influence of the multi-curve approach on the interest rate derivative pricing. We calculated and compared the price of a simple swap in both multi-curve and single curve approaches. We suggested the generalization of the lattice approach, which is usually used to approximate the short interest rate models, for milti-curve framework. This is a novel result, which have not been developed in the scientific literature. As an example, we showed how to use the Black-Derman-Toy interest rate model on binomial lattice in multi-curve framework and calculated the price of the 2-8 period swaption in a single (LIBOR) curve and two-curve (OIS+LIBOR) approaches. This technique can be used for pricing any interest rate instrument.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.