Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

The purpose of this paper is to examine aggregate and cross-sector allocations of foreign aid flows in the aftermath of epidemics and to determine whether latent effects can be observed in the following year.

Using data from the Organization for Economic Cooperation and Development (OECD) on Bilateral commitments of Official Development Assistance (ODA) from 2005-2019, we employ an Ordinary Least Squares (OLS) model based on the structural gravity framework to account for spatial interactions between donor and recipient countries.

Our results show that epidemics have a positive and significant effect on bilateral foreign aid across all sectors and that aid to the Humanitarian sector is less conditional on pre-existing relationships than others. Results for latent effects on aid vary by sector.

We further find that isolating epidemics in our analysis suggests that certain diseases prompt a different aid response wherein aid to non-health sectors falls.

Conclusions

We find that epidemics do indeed engender changes in foreign aid behavior.

To be specific, epidemics have a positive and significant effect on foreign aid commitments to all sectors. Our results are unable to shed light on the hypothesis of reallocation between sectors. However, they do illustrate that aid to both health-related and non-health-related sectors increases.

Aid in this context is also persistent. That is, our results, robust to numerous checks, show that the positive effects of epidemics may be observed not only in the year of the outbreak but also in the following year.

By analyzing each disease independently, we further find that certain diseases prompt a different aid response and may suggest the presence of a foreign-aid reallocation due to epidemics.

However, our study does not measure the effectiveness of aid which is necessary for the design of productive policy measures that could save countless lives. Naturally, this presents new opportunities for research and raises important questions regarding the optimal allocation of aid given shocks to global health. That is, does increasing aid to all sectors serve as an effective one-size-fits-all solution? Or would a more efficient policy consist of donors reallocating aid across sectors to account for short and long-term changes in the demand for healthcare caused by an epidemic?

Best paper award for Inês Xavier (Economics ’15, UPF PhD ’21)

Congratulations to @Ines_MXavier for winning the @ITAXjournal Best PhD student paper award for her paper "Wealth Inequality in the US: The Role of Heterogenous Returns".

— International Tax and Public Finance (@ITAXjournal) August 26, 2021

Paper abstract

Why is wealth so concentrated in the United States? In this paper, I investigate the role of return heterogeneity as a source of wealth inequality. Using household-level data from the Survey of Consumer Finances (1989-2019), I provide new empirical evidence on returns to wealth in the United States, and find that wealthier households earn, on average, higher returns: moving from the 20th to the 99th percentile of the wealth distribution raises the average yearly return from 3.6% to 8.3%. To understand how these return differences shape the distribution of wealth, I introduce realistic return heterogeneity in a partial equilibrium model of household saving behavior. This exercise suggests that considering both earnings and return heterogeneity can fully account for the top 10% wealth share observed in the data (76%), which cannot be explained by earnings differences alone.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Vector autoregression (VAR) models are a popular choice for forecasting of macroeconomic time series data. Due to their simplicity and success at modelling the monetary economic indicators VARs have become a standard tool for central bankers to construct economic forecasts. Impulse response functions can be readily retrieved and are used extensively to investigate the monetary transmission mechanism. In light of the recent advancements in computational power and the development of advanced machine learning and deep learning algorithms we propose a simple way to integrate these tools into the VAR framework.

This paper aims to contribute to the time series literature by introducing a ground-breaking methodology which we refer to as DeepVector Autoregression (Deep VAR). By fitting each equation of the VAR system with a deep neural network, the Deep VAR outperforms the VAR in terms of in-sample fit, out-of-sample fit and point forecasting accuracy. In particular, we find that the Deep VAR is able to better capture the structural economic changes during periods of uncertainty and recession.

Conclusions

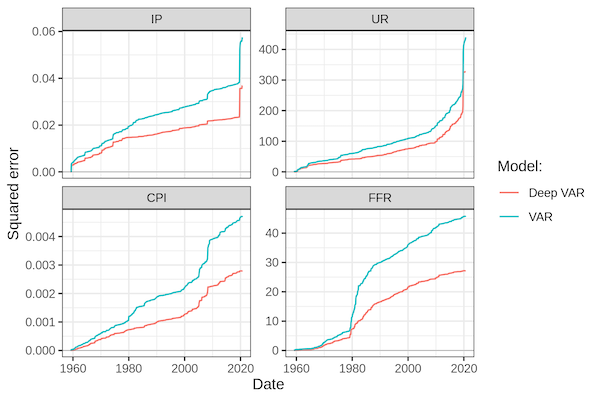

To assess the modelling performance of Deep VARs compared to linear VARs we investigate a sample of monthly US economic data in the period 1959-2021. In particular, we look at variables typically analysed in the context of the monetary transmission mechanism including output, inflation, interest rates and unemployment.

Our empirical findings show a consistent and significant improvement in modelling performance associated with Deep VARs. Specifically, our proposed Deep VAR produces much lower cumulative loss measures than the VAR over the entire period and for all of the analysed time series. The improvements in modelling performance are particularly striking during subsample periods of economic downturn and uncertainty. This appears to confirm or initial hypothesis that by modelling time series through Deep VARs it is possible to capture complex, non-linear dependencies that seem to characterize periods of structural economic change.

Credit: the authors

When it comes to the out-of-sample performance, a priori it may seem that the Deep VAR is prone to overfitting, since it is much less parsimonious that the conventional VAR. On the contrary, we find that by using default hyperparameters the Deep VAR clearly dominates the conventional VAR in terms of out-of-sample prediction and forecast errors. An exercise in hyperparameter tuning shows that its out-of-sample performance can be further improved by appropriate regularization through adequate dropout rates and appropriate choices for the width and depth of the neural. Interestingly, we also find that the Deep VAR actually benefits from very high lag order choices at which the conventional VAR is prone to overfitting.

In summary, we provide solid evidence that the introduction of deep learning into the VAR framework can be expected to lead to a significant boost in overall modelling performance. We therefore conclude that time series econometrics as an academic discipline can draw substantial benefits from further work on introducing machine learning and deep learning into its tool kit.

We also point out a number of shortcomings of our paper and proposed Deep VAR framework, which we believe can be alleviated through future research. Firstly, policy-makers are typically concerned with uncertainty quantification, inference and overall model interpretability. Future research on Deep VARs should therefore address the estimation of confidence intervals, impulse response functions as well as variance decompositions typically analysed in the context of VAR models. We point to a number of possible avenues, most notably Monte Carlo dropout and a Bayesian approach to modelling deep neural networks. Secondly, in our initial paper we benchmarked the Deep VAR only against the conventional VAR. In future work we will introduce other non-linear approaches to allow for a fairer comparison.

Code

To facilitate further research on Deep VAR, we also contribute a companion R package deepvars that can be installed from GitHub. We aim to continue working on the package as we develop our research further and want to ultimately move it onto CRAN. For any package related questions feel free to contact Patrick, who authored and maintains the package. The is also a paper specific GitHub repository that uses the deepvars package.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

In recent years, large platforms have raised concerns that they may engage in anti-competitive practices that affect market competition. Therefore, analyzing the competition structure inside platforms is a relevant issue that has not been treated in much empirical research.

This study analyzes how a platform’s owner could affect the degree of competition among members of one group in the platform through biasing search results using rating classifications. In this paper, we perform an application to Airbnb‘s market in Barcelona given the particularity of rating is an unavailable searching filter to guests.

We found evidence that listing’s rating classification represents an important market segmentation in the Airbnb’s market in Barcelona that could imply a possible practice of biasing search results. Moreover, we found that the intensity of competition is differentiated by the rating-related segments, which means that these segments are concentrating competition.

Conclusions

We found an inelastic demand for Airbnb’s listings in Barcelona in a market that is divided by rating classification. In particular, our empirical results show the following two points:

First, the majority of hosts face an inelastic demand. These results are consistent under the two main models we used. From the nested logit model under rating segmentation, we found that when there is a 10% increase in price of available nights, there is an expected decrease in booked nights of 4.5%. These results imply that there is room to increase the price without reducing the revenues of the hosts.

Second, even though the rating is not available as a filter in the Airbnb web page, it creates an important market segmentation. This means that the competition between two listings that belong to the same segment is different from the competition faced by two listings that belong to different rating classifications. Moreover, we found differences in intensity of competition faced by listings that belong to different segments.

Finally, these results show that the existence of segmentation suggests that Airbnb is performing a rating-based market division. Yet the rating segmentation does not show a clear pattern of competition intensity in each group.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

We construct a theoretical Overlapping Generations (OLG) model to describe how sovereign debt crises can propagate in the economy under certain financial constraints.

In the model, households work when young and deposit their savings in exchange for a dividend, banks invest deposits in assets and government bonds. Banks, subject to legal and market requirements, invest a fixed fraction of deposits and own equity in assets. When prices of bonds fall due to perceived sovereign debt risks, banks can invest less on capital goods directly affecting the business cycle. This paper simulates the deviations from steady-state produced by a shock to government securities and provides insights into macro-prudential policy implications.

We find that a sovereign debt crisis affects young and old generations differently, with the latter facing higher fluctuations in consumption. We also find that the macro-prudential policy can be effective only at very high levels on the old, but ineffective for the younger generation.

Conclusions

This paper draws three main conclusions about the impact of a sovereign debt crisis on the business cycle within the proposed OLG theoretical framework:

A decline in government bond prices leads to lower output, wages and dividend negatively affecting present and future consumption. However, this effect is different for young and old generations. In particular, the old seem to face more sudden changes and higher deviations from steady-state values when a sovereign debt crisis takes place.

The proposed macro-prudential policy does not seem to offset the impact of a fall in government bonds prices on the business cycle. In fact, almost all the macroeconomic variables of interest in our theoretical model do not change significantly, relative to their steady-state values, when the supervising authority modifies the capital requirements for banks.

A very aggressive policy on capital requirements (i.e. x=0.9 for the whole period) can compensate for the negative shock bonds prices have on dividends and, therefore, consumption for the old.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Mental health outcomes significantly deteriorated in the United Kingdom as a result of the Covid-19 pandemic, particularly for younger individuals. This paper uses data from the Millennium Cohort Study to investigate the heterogeneity of mental health effects of the Covid-19 pandemic on adolescents by both personality types and personality traits. Using two-step cluster analysis we find three robust personality clusters: resilient, overcontrolled, and undercontrolled.

Conclusions

We surprisingly find that resilient individuals, who generally have better mental health, reported larger decreases in mental health during the pandemic than both undercontrollers and overcontrollers

The effect seems to be driven by the neuroticism trait, such that those with higher neuroticism scores fared better than those with lower scores during the pandemic

Our findings highlight that personality traits are important factors in identifying stress-prone individuals during a pandemic.

Finance master project by Lapo Bini and Daniel Mueck ’21

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

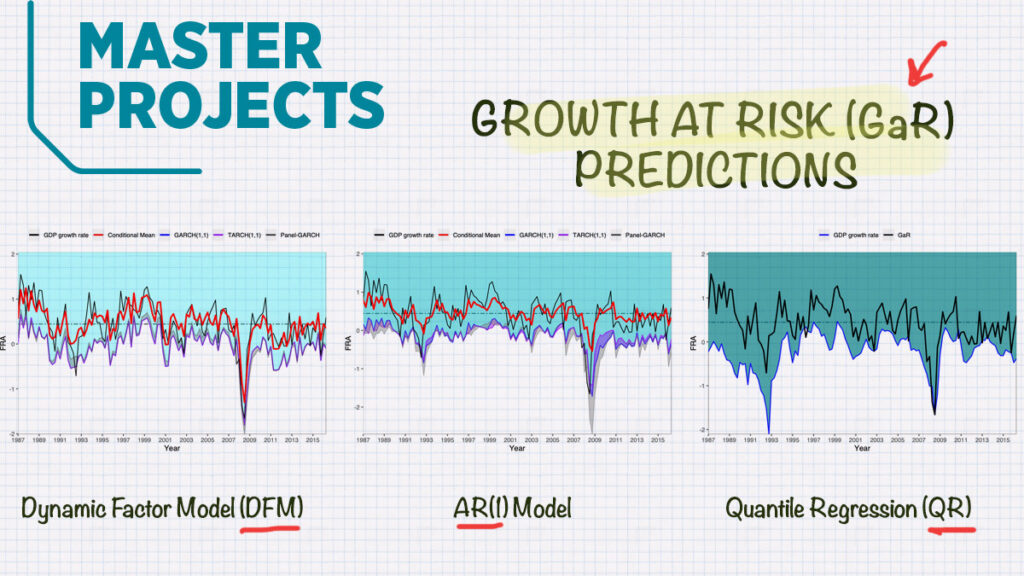

In order to analyse whether financial conditions are relevant downside risk predictors for the 5% Growth at Risk conditional quantile, we propose a Dynamic Factor- GARCH Model, comparing it to the two most relevant approaches in the literature. We conduct an out-of sample forecasting analysis on the whole sample, as well as focusing on a period of increased European integration after the 2000s. Always, including the national financial conditions index, term structure and housing prices for 17 European countries and the United States, as down side risk predictors. We find evidence of significant predicting power of financial conditions, which, if exploited correctly, becomes more relevant in times of extraordinary financial distress.

Conclusions

We propose a Dynamic Factor-GARCH model which computes the conditional distribution of the GDP growth rates non-parametrically, exploiting the dimensions of a panel of national financial conditions and compare it to the models of Adrian, Boyarchenko, and Giannone (2016 )and Brownlees and Souza (2021) out-of-sample.

Contrasting to our in-sample results, the out-of sample results exhibit a higher degree of heterogeneity across countries. While our model performs at least as good or better as the AR(1)-GARCH(1,1) specification of Brownlees and Souza (2021) in the long run, it produces unsatisfactory results for the one-step forecast horizon.

However, by focusing our out-of-sample analysis on a smaller sample around the period of the Great Recession, we not only outperform the other two models analysed, but also obtain strong indication of increased importance and predictive power of financial conditions.

We provide evidence that by correctly modelling financial conditions, they not only exhibit predictive ability for GDP downside risk, but also improve in-sample GaR predictions. Further, we show that they are relevant out-of-sample predictors in the long run. Finally, when focusing on periods of extraordinary financial distress, like the Great Recession, financial conditions become even more relevant. However, the right model needs to be applied in order to exploit that predictive power.

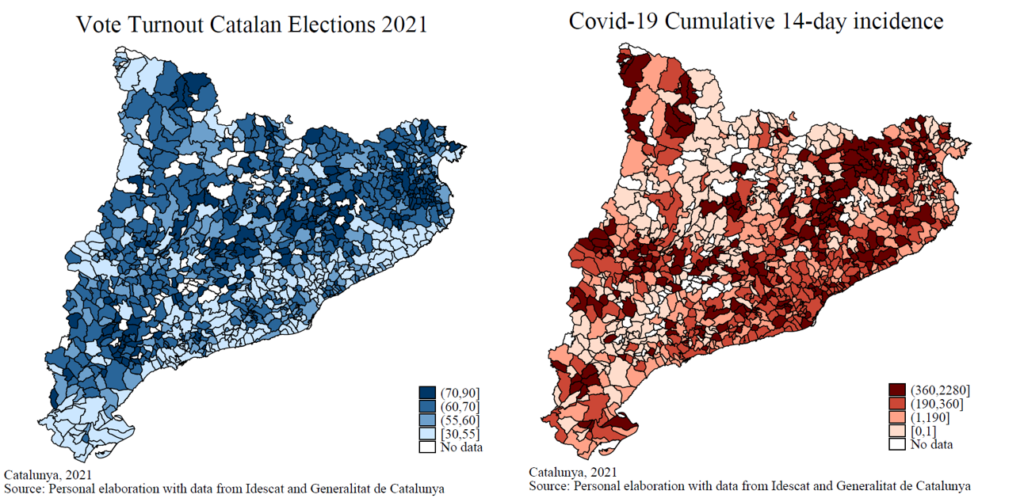

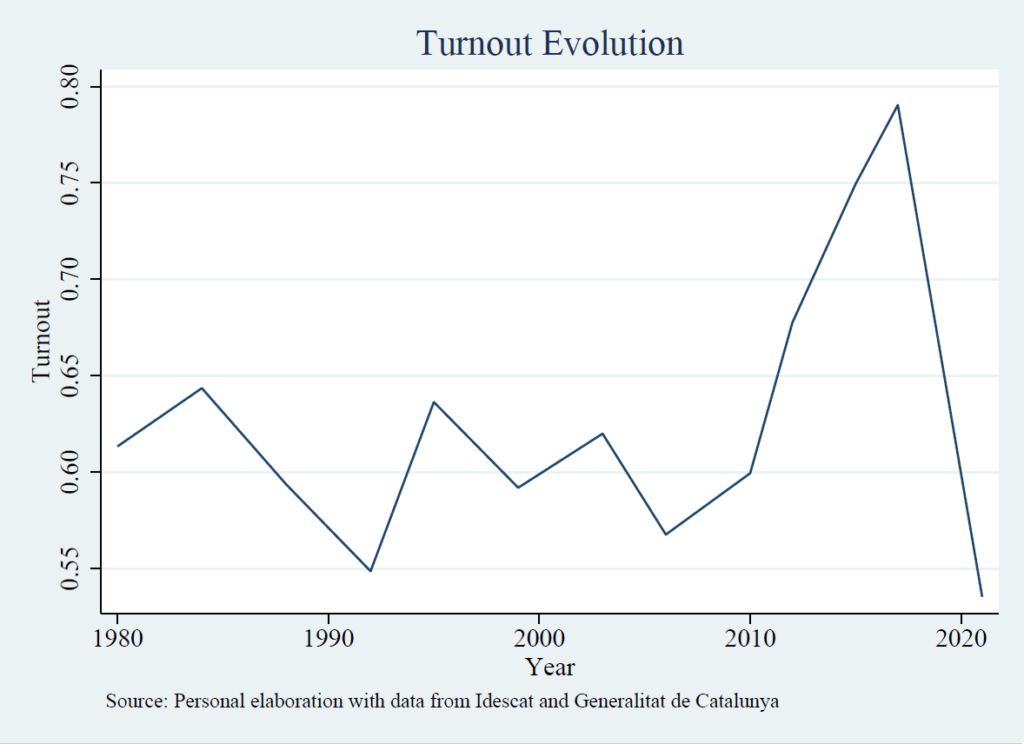

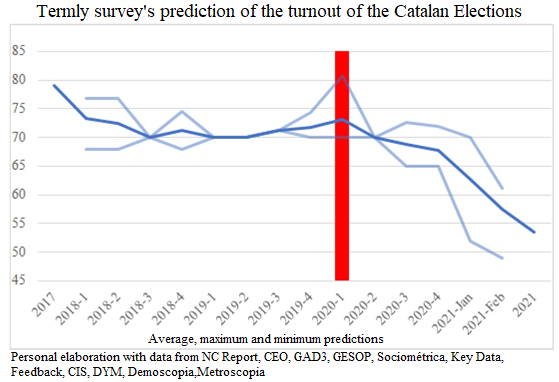

In the Catalan elections held on 14 February 2021, just a few weeks after the peak of the third wave of COVID-19, voter turnout was significantly lower than in 2017 (51.3% compared to 79.1%) and the lowest in history. Despite the political context being different compared to 2017, in the run-up to the election predicted turnout remained at similar levels until the emergence of Covid-19 – whereupon it dropped sharply. In these extraordinary elections, the vote share of the parties changed which shifted the Catalan political spectrum.

We study this relationship between Covid-19 and electoral results in Catalonia. To estimate the effect of the pandemic we explore the differences in cumulative Covid-19 incidence at the municipal level and compare it with electoral outcomes controlling for economic and demographic variables (population density, percentage of over-65 years old, share of foreign population and the unemployment rate).

The most widely used model of electoral participation, that of Riker and Ordeshook (1968), considers that the decision to participate is based on a cost-benefit trade-off between the expressed benefit of voting (feeling fulfilled, considering that civic duty is fulfilled, etc.) and the cost that individuals associate with participation. This cost rose sharply, because voting implied a higher risk of contracting the disease and the inconvenience caused by anti-covid measures. Therefore, higher costs would imply lower turnout as shown by several empirical studies, which find that with small increases in cost turnout drops significantly (eg. Aldrich, 1993). We assume that the increase in cost is the same for all (although there could be differences by age, and so we control for the most vulnerable group, the over-65s), which would imply a fall in participation, but could also induce changes in the outcome. This change may be due to differences in the “sentimental” benefit of voting between voters of different parties.

Economic theory also indicates who voters choose, conditional on voting. According to “retrospective” voting theory, voters support or punish parties in government in response to their performance in a crisis such as Key (1966). In contrast, according to “prospective” voting theory, the individual votes for the party that he believes will do better or, as Leininger and Schaub (2020) argue, seeks to match the party in regional and national government for more optimal crisis management.

Effect on participation

As seen in the maps above, the areas with the highest cumulative Covid incidence also have a lower percentage of participation, especially the Barcelona metropolitan area. Our analysis shows that an increase of 100 points in cumulative incidence in the last 14 days is related to a drop of 2.6 percentage points in turnout. To understand the magnitude, this is equivalent to one extra Covid case in a municipality of 1,000 inhabitants, so we estimate that the effect of the pandemic is quite high. To understand the impact of the second and third waves of Covid-19, we have conducted the analysis with cumulative incidence measures in the last month and in the last 4 months prior to the elections. However, as the period lengthens, the effect on turnout decreases (1.3 and 0.4 percentage points respectively).

However, the political context also changed: while in 2017 the voting framework was centred on the independence process (which led to the historical record turnout); in 2021 it was the pandemic that defined the elections. However, the trigger for this change of context (and the neglect of the independence process) was the eruption of the virus. As can be seen in the graph below showing the predicted turnout for the elections to the Parliament of Catalonia. Since Covid-19 appears to be the only element of exogenous variation between municipalities when comparing the 2017 and 2021 elections, we can infer causality.

These results are in line with the theory of the myopic voter who takes into account episodes closer to the election when voting. In this case, the myopic voter is acting rationally, as they account for the actual risk at the time of the vote rather than the risk of the past few months.

Effect on results

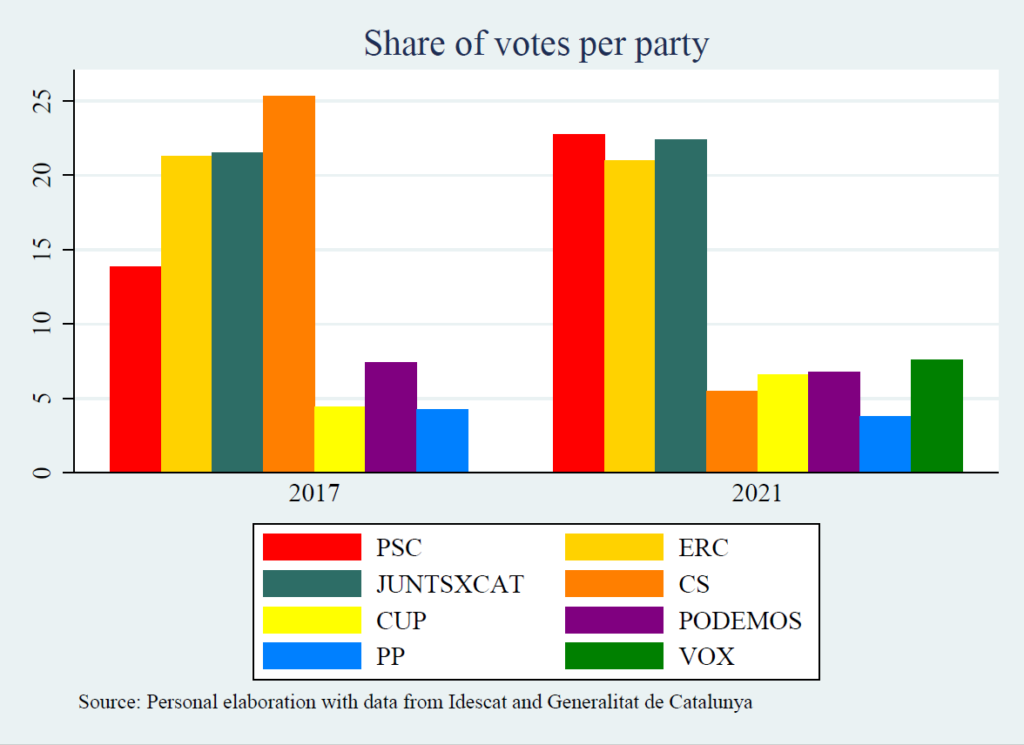

Secondly, the elections brought a major shift in the political spectrum, as can be seen in the bar charts above. For this reason, we have not been able to include other elections, as they were not comparable with each other. We have grouped the political parties into the following ideological and identity groups:

Pro-independence left: ERC and CUP.

Pro-independence right-wing: JUNTSXCAT and PDECAT

Non-independence left-wing: PSC and PODEMOS

Non-independence right: PP, Cs, and VOX

First, we respectively analyse the pro-independence and non-independence groups, the victors (the pro-independence coalition), and the opposition. The results show that the pandemic has a positive effect on the percentage of the vote of the pro-independence parties and a negative effect on the non-independence group. This effect can be seen as a retrospective vote, showing a certain approval by pro-independence voters of how the regional government has handled the pandemic.

On the other hand, in the analysis of the groups divided into identity and ideological groups, we find that the group with the highest positive coefficient is the non-independence left – the coalition in charge of the central government at the time of the elections. This behaviour is associated with the prospective vote. With the arrival of Salvador Illa (The Spanish Minister of Health during the pandemic) as the PSC candidate, the party was reinforced and ends up as the winner of the elections. This positive effect can be seen as an attempt to align the post-pandemic recovery strategy in Catalonia with that of the rest of Spain.

In conclusion, our results suggest that COVID-19 had a significant outcome in the Catalan elections that translated into a negative relationship between the virus and turnout. In contrast, the relationship is positive between cumulative incidence and the vote of pro-independence parties and the non-independence left-wing group. At the same time, the retrospective theory seems to hold true as there has been strong support for the government in office based on their management of the pandemic.

Connect with the authors

Iván Auciello Estévez ’21 is a student in the Barcelona GSE Master’s in Economics. After graduating he plans to work as a Research Assistant at Banco de España.

Pau Jovell Codina ’21 is a student in the Barcelona GSE Master’s in Economics. After graduating he plans to work as a Research Assistant at Banco de España.

Gradual institutional change analyses have allowed drawing a more flexible line between stability and transformation when examining how institutions evolve over time, particularly in the absence of major critical junctures or exogenous shocks. Yet, the explanatory power of the theory has been undermined by a lack of attention to the overlapping boundaries of the modes of gradual institutional change, a relatively static model of agency, and conceptual confusion regarding what the modes of change exactly are.

In our recent article “Discursive Strategies and Sequenced Institutional Change: The Case of Marriage Equality in the United States” published in Political Studies, Tània Verge and I argue that addressing these shortcomings requires investigating the agent-based dynamics underpinning gradual institutional change and bringing to the fore the role of ideas. Indeed, ideas and discourses can have a constitutive impact in the creation, maintenance and reform of institutions, and actors strategically reframe problems and redirect solutions to influence both the process and the outcome of policy reforms.

Employing marriage equality in the United States as a case study, we show that the modes of gradual institutional change can be studied simultaneously as processes that unfold over time, often in a sequential fashion, as outcomes of these processes, and as strategies pursued by actors to steer, impede or undermine policy change.

Our results reveal that proponents and opponents of marriage equality have deployed discursive frames to legitimize institutional change to take off sequentially in a progressive direction — through the modes of “layering“ and “displacement“ — and in a regressive direction — through the mode of “conversion“.

Throughout this sequenced process, opposing actors have not only adjusted their discursive strategies to both their rivals and the targeted institutional venues, but have also shifted roles as change and status quo agents. Indeed, our study shows that the actors contesting the institutional status quo in one stage may become the actors defending it in a subsequent phase of the institutional change process, and vice versa. Thus, we argue that traditional, static conceptualizations of agency should be problematized and, rather than as resistance to gender-friendly reforms, opposition to marriage equality should be understood as a proactive mobilization to transform existing institutions.

The recent US Supreme Court decision in Fulton v. City of Philadelphia (2021) in favor of a Catholic foster care agency that refuses to work with same-sex couples, should then be understood as a victory of the years-long conservative strategy to undermine LGBT couples’ newly recognized right to marry.

Lastly, our study highlights the role of private actors as ideational entrepreneurs in the adoption and implementation of “morality policies,“ such as marriage equality. While morality policy scholars have so far predominantly examined how governmental actors shape policymaking, we show that the discursive strategies deployed by LGBT advocates, religious-conservative organizations and other private actors, such as foster care agencies, florists, and bakers, created new opportunities to influence policy debates and tip the scales to their preferred policy outcome.

Since the 2007 implementation of the “Dependency Act”, people with functional limitations in Spain can request Long-Term Care (LTC) benefits. The Act’s main objective is to improve the care and quality of life of people who have lost their autonomy. Fourteen years later, evidence on the impact of the Dependency Act in Spain on its beneficiaries remains scarce. This is partly because we need data on the quality of life of this population in order to fully evaluate its impact and we still don’t gather a suitable indicator. However, we can assess the impact of benefits by utilising data on the use of healthcare services as a proxy to estimate quality of life and health, and that is the approach we have taken in our research.

The relationship between LTC benefits and healthcare use

The effect of LTC benefits on healthcare use is not trivial and may have implications not just for the quality of life of recipients, but also for the management of healthcare services.

If access to LTC improves the health status of dependent people (for example through better treatment management, better nutrition or avoiding domestic accidents), investments in the LTC system could save healthcare providers money in the future. On the other hand, LTC benefits might increase the demand for healthcare, for example through greater health-monitoring by caregivers.

Using data on the type of healthcare service, type of admission and diagnoses, we can better understand the relationship between benefits and healthcare use, and therefore increase the efficiency in the allocation of social care and healthcare resources to design a better integrated care system.

The data

To study the effects of LTC benefits on healthcare use, we needed to gain access to data from social services and healthcare providers and then link it. As others have shown, this was not easy, but fortunately, the interest of the institutions involved in this research —CatSalut, AQuAS, the Departament de Treball, Afers socials i Famílies de la Generalitat de Catalunya (DTASF) (Labour, Family and Social services department) and CRES (UPF) — helped to facilitate this process.

Even with access to the data, measuring the effect of LTC benefits on the health system is not straightforward. Those who qualify for benefits will by definition have worse health and, regardless of the new policy, will probably make greater use of the healthcare system than those who don’t qualify for benefits. Therefore, simply comparing those applicants who receive LTC benefits with those who don’t would not help us to identify the effects of the Dependency Act.

To deal with this, we use an instrumental variable technique based on the “leniency” of the evaluators. The idea is as follows. When there is an evaluation guided by objective criteria such as when grading an exam, imposing a judicial sentence or assigning the severity of a medical case, there is always a degree of subjectivity from the person performing the assessment. It is common in research literature to consider this as a source of exogenous variation, because there is no predictable basis by which assessors should differ. This allows us to use traditional statistical methods that can identify any consequences associated with new policies. In our context, despite the fact that the assessment is based on the Dependency Assessment Scale, each examiner has a small margin of subjective interpretation. Thus, there are examiners who, on average, tend to provide slightly higher scores, so that their applicants qualify for greater LTC benefits. Since the applicant cannot choose his/her examiner, being assessed by one examiner or another affects the probability of receiving a benefit which is exogenous to the assessment process.

The results

In the two graphs below, we summarize the most important results from our research.

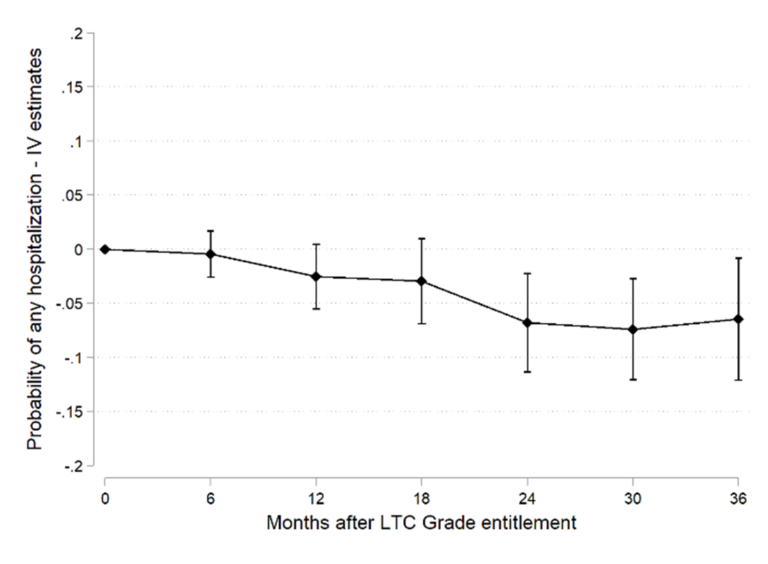

Figure 1 shows that access to LTC benefits decreases by 7 percentage points the probability of a group of hospitalizations considered by the medical literature as avoidable with continuous care for the elderly (such as hospitalizations for injuries, ulcers and nutritional deficiencies). This represents a 60% reduction in this type of hospitalization.

Figure 1. Effect of LTC benefits on the probability of avoidable hospitalizations

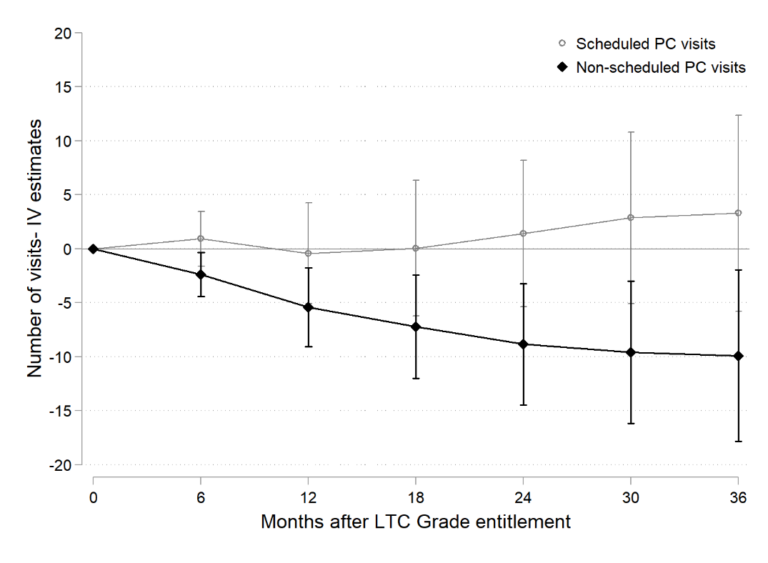

Figure 2 shows that unscheduled visits to primary care decrease by almost 10 visits two years after receiving LTC benefits, a 50% reduction with respect to the mean. Our analysis by diagnosis indicates that this reduction is explained by a sharp drop in visits caused by the economic and family situation of the individual.

Figure 2. Effect of LTC benefits on visits to primary care. Scheduled vs Unscheduled

Conclusions

Our results show that LTC benefits can mitigate the use of healthcare services, in line with the conclusions of previous research. Additionally, our data allows us to go one step further, identifying in detail the types of services which are the most affected.

Particularly interesting are the results relating to primary care, where LTC benefits strongly reduce visits not strictly related to health causes. It seems that reinforcing the LTC system will not only improve the quality of life of dependents and caregivers, but may also reduce the pressure on the healthcare system.

Undoubtedly, these results are important given the chronic under-financing of the LTC system, especially in a context where COVID-19 has highlighted a need for real integration between social and health care. This is just one example of how access to, and analysis of administrative data can contribute to the evaluation of public policies, facilitating better informed decision making.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.