EPP master project by Charley Lamb, Jana Eir Víglundsdóttir and Alessandro Zicchieri ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Our paper examines the wages and career prospects of employees in flexible work arrangements (FWAs). Using the British Household Panel Survey, we analyse the effect of being in a FWA on hourly wages and the likelihood of promotion. We use the occupational share of employees in FWAs before and after the introduction of “Right to Request” (R2R) legislation as an instrument to control for sample selection. Applying our instrument in pooled OLS and linear regression models, we find that flexible workers, particularly women, may receive higher wages than their non-flexible counterparts. This supports theoretical arguments that FWAs could increase labour productivity.

Conclusions

Our findings imply that there may be no penalty associated with workers adopting flexible working practices. Our instrumental variables wage model implies there could in fact be a reverse effect: coefficients changed from negative. In particular, the effect of FWAs was significant and large for women, leading to an approximately 9 percent increase in their wages. Those in FWAs have higher wages than those in conventional working arrangements, controlling for variables such as occupational choice, hours worked, and personal circumstances (including number of children and educational background). Similarly, we cannot reject the hypothesis that FWA has no impact on career progression, when modelling promotions as a 10 percent pay rise versus the previous year.

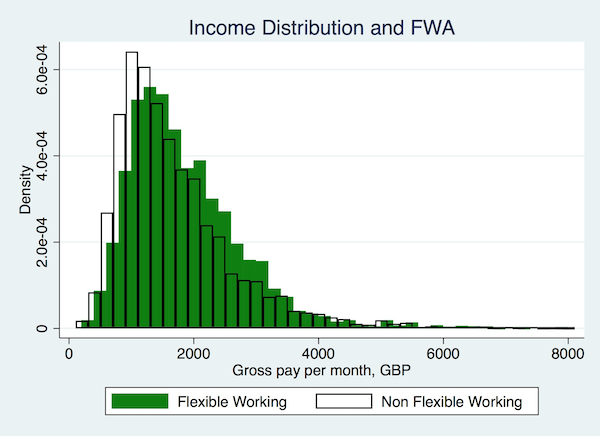

Income Distribution and FWA

We do find some evidence that working flexibly decreases the difference in wage outcomes between men and women. The approximately 9 percent increase in wages associated with our FWA variable in our women-only specification compares to a 5 percent increase in our men-only specification. We cannot reject the hypothesis that FWAs have no effect on men’s wages. We find evidence women in FWAs are paid significantly more than their non-flexible counterparts.

This begs the question: why do those in FWAs appear to achieve better labour market outcomes than those not in FWAs? This appears to contradict some findings of economic theory on compensating wage differentials and the effects of similar working arrangements, such as part-time work. Further, the fact that our wage findings were highly significant for women (and not for men) appears to go against the gendered difference in how men and women use flexible working; men are more likely to use FWAs to improve their career outcomes, whilst women use FWAs to accommodate care needs.

First, we could have captured a range of productivity benefits that often come alongside flexible working practices. The increase in schedule control may improve worker satisfaction and hence productivity in itself, but is also often associated with better workplace practices such as improved management (Bloom et al, 2010). The increase in flexible working seen across many sectors (such as services) following the R2R reforms may have disproportionately benefited them ahead of other, less “flexible” sectors. The UK, with more than two-thirds of its labour force in the service sector, may have seen a productivity rise associated with more employees having greater scheduling control. Increases in productivity may then have been passed on to flexible-working employees in the form of pay rises above the mean.

Second, our model may neglect important social trends. The R2R legislation may have accompanied shifting attitudes towards flexible working, which spurred an increase in the compensation afforded to flexible workers. Future research examining historical trends in the remuneration of employees in FWAs could provide more detail on this.

Economics master project by Marc Agustí, Magnus Asmundsson, Christof Bischofberger, Pablo de Llanos, Alberto Font, and Lucía Kazarian ’20

Source: Airbnb

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Peer-to-peer home-sharing platforms such as Airbnb are a new phenomenon which many researchers consider to be responsible for significant disruptions in the housing market. Prior to the introduction of these platforms into the rental market, hotels were the primary supplier of short-term rentals, while residential properties almost exclusively operated on the long-term rental market. The introduction of short-term rental platforms like Airbnb, allows homeowners to choose either to supply on the short-term or the long-term rental markets. As a result, when residential properties are moved to the short-term rental market, the quantity of housing supplied on the long-term rental market decreases, inducing an upward pressure on long-term rents.

In our paper, we offer a novel approach to investigate the extent to which the expansion of the sharing economy is responsible for increases in long-term rents and prices on the housing market. To this end, we construct a theoretical framework for the housing market that allows for spillover effects between neighborhoods, and other local externalities caused by tourism. The model allows for the short-term housing market devoted to tourism to impact both long-term rental rates and housing prices. Using a panel of quarterly data on newly signed rental contracts and transaction prices in Barcelona from 2015-Q2 to 2018-Q4, we implement a fixed-effects spatial 2SLS method allowing for endogeneity in the variable which measures the presence of Airbnb.

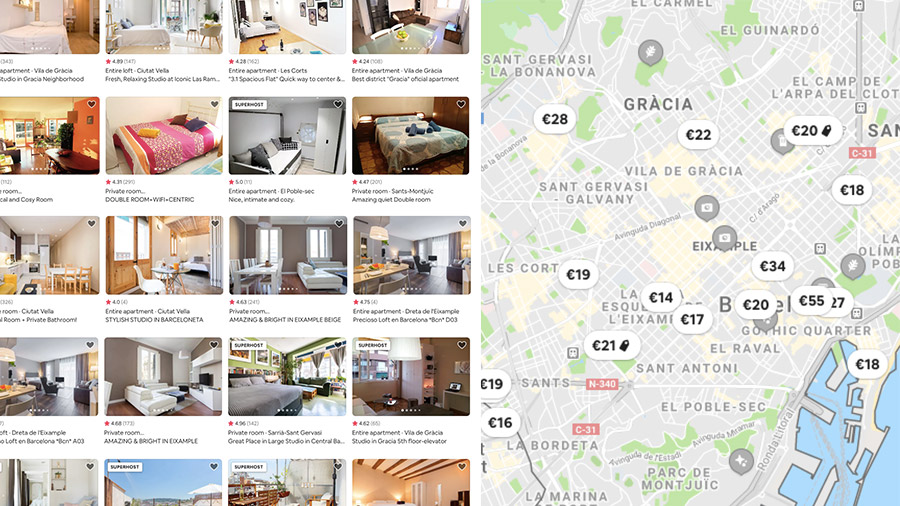

Airbnb listings in Barcelona (2018-Q2)

Barcelona, which hosts the sixth largest concentration of Airbnb listings in the world, serves as a prime case study to investigate these effects because our dataset covers growth rates in contractual rental rates, transaction prices and the number of active Airbnb listings of 27.42%, 27.41% and 29.38%, respectively.

Key results

The theoretical model predicts that a change in the level of Airbnb activity might affect both long-term rents and housing prices. In fact, if negative externalities generated by tourists are sufficiently small, Airbnb leads to increases in long-term rental prices. Yet, these effects ultimately depend on the values of parameters such as the size of the stock of housing units and the level of externalities emerging from tourism. In addition, the model bears upon the effects of Airbnb on gentrification and displacement: we find that for a positive increase in the negative externalities generated by tourism, the proportion of homeowners renting in the short-term market will increase. As the degree to which residents are harmed by negative externalities increases, more of them will decide to abandon their neighborhood, reducing the local demand for long-term housing. As a result, rents will suffer a downward pressure, increasing the relative profitability of the short-term rental market for homeowners. Besides, this effect will be aggravated if the degree of inter-neighborhood dependence generated by externalities is high. Residents will be prone to move to other neighborhoods in which not only the presence of Airbnb is low, but also in which the penetration of this marketplace is low in the surrounding areas.

We refer to this process as Airbnb-induced gentrification. Similarly, if the profitability of renting a property on Airbnb increases, a similar process as the one we have just described above would arise, which would also lead to gentrification.

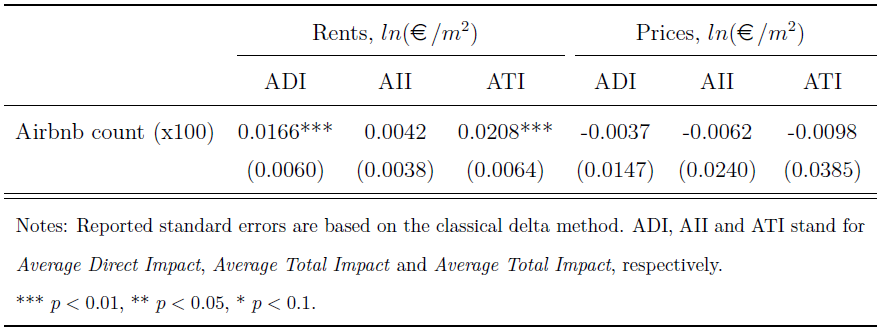

For another thing, our main empirical results show that Airbnb positively and significantly affects rents, even when accounting for spatial dependence and inter-neighborhood spillovers. In a given neighborhood (as classified in this paper), for every additional 100 Airbnb listings, rents increase by an average of 2.1% when indirect spillovers coming from adjacent neighborhoods are included. In particular, the direct effect of Airbnb within a given neighborhood accounts for much of this effect: the own-neighborhood effect is to induce a 1.7% increase in rents. The maximum average indirect effect found in the sample data accounts for 35% of the total effect. The implications of these findings are far reaching and suggest that spillover effects can indeed explain a large portion of rent increases. Likewise, we identify a potential bias in the previous literature in that the total effect is falsely interpreted as the direct effect, thereby misinterpreting the direct effect of Airbnb on long-term rents.

Empirical Results: Main Impact Measures

In contrast, our empirical results show that Airbnb has had no significant effect on transaction prices. The most plausible explanation for the non-significant results for prices is that homeowners do not believe that Airbnb is sustainable in the long-run, and therefore they do not adjust their predicted future cash flows when valuing their properties.

Finally, we believe that future research could delve into more detailed theoretical models, especially with respect to the price setting by homeowners in light of the establishment of Airbnb. Additionally, we think that making a distinction between direct and indirect neighborhood effects is vital in order to truly understand the dynamics of the housing markets, especially in the growing metropoles. Accordingly, we encourage scholars to further apply and develop spatial econometric methods that measure indirect spillover effects in studies related to housing markets.

Working Paper by Nicolò Maffei Faccioli (Macro ’15 and IDEA) and Eugenia Vella (Sheffield)

What is the macroeconomic impact of migration in the second-largest destination for migrants after the United States?

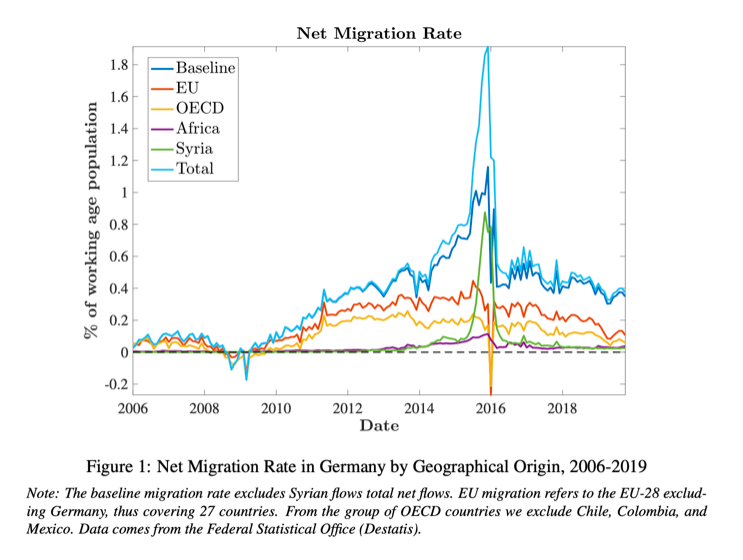

In this paper, we uncover new evidence on the macroeconomic effects of net migration shocks in Germany using monthly data from 2006 to 2019 and a variety of identification strategies in a structural vector autoregression (SVAR). In addition, we use quarterly data in a mixed-frequency SVAR.

While a large literature has analyzed the impact of immigration on employment and wages using disaggregate data, the migration literature in the context of macroeconometric models is still limited due to a lack of data at high frequency. Interestingly, such data is available for Germany. The Federal Statistical Office (Destatis) has been collecting monthly data on the arrivals of foreigners by country of origin on the basis of population registers at the municipal level since 2006. The figure below shows the net migration rate by origin.

Key takeaways

Migration shocks are persistently expansionary, increasing industrial production, per capita GDP, investment, net exports and tax revenue.

Our analysis disentangles the positive effect on inflation of job-related migration from OECD countries from the negative effect of migration (including refugees) from less advanced economies. In the former case, a demand effect seems prevalent while in the latter case, where migration is predominantly low-skilled and often political in nature (including refugees), a supply effect prevails.

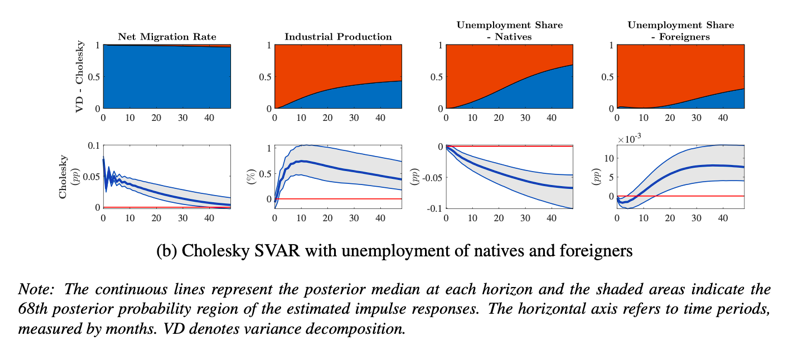

In the labor market, migration shocks boost job openings and hourly wages. Unemployment falls for natives, driving a decline in total unemployment, while it rises for foreigners (see figure below). Interestingly, migration shocks (blue area in the first row) play a relevant role in explaining fluctuations in industrial production and unemployment of both natives and foreigners, despite the bulk of these being explained by other shocks (red area in the first row), like business cycle and domestic labor supply.

We also shed light on the employment and participation responses for natives and foreigners. Taken together, our results highlight a job-creation effect for natives and a job-competition effect for foreigners.

Conclusion

The COVID-19 recession may trigger an increase in migration flows and exacerbate xenophobic sentiments around the world. This paper contributes to a better understanding of the migration effects in the labor market and the macroeconomy, which is crucial for migration policy design and to curb the rise in xenophobic movements.

Niccolò Maffei-Faccioli ’15 (Macroeconomic Policy and Financial Markets) is a PhD candidate in Economics at Universitat Autònoma de Barcelona and Barcelona GSE (IDEA).

Finance master project by Güneykan Özkaya and Yaping Wang ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Introduction

Historically, there have been many strategies implemented to solve the portfolio choice problem. An accurate estimation of optimal portfolio allocation is challenging due to the non-deterministic complexities of financial markets. Due to this complexity, investors tend to resort to the mean-variance framework. If we consider the mean-variance framework, there are several drawbacks to this approach. The most pivotal one could be normality assumption on returns so that we could depict the behavior of returns only by mean and variance. However, it is well known that returns possess a heavy-tailed and skewed distribution, which results in underestimated risk or overestimated returns.

In this paper, we rely on a distribution of different metrics other than returns to optimize our portfolio. In simple terms, we combine several parametric and non-parametric bandit algorithms with our prior knowledge that we obtain from historical data. This framework gives us a decision function in which we can choose portfolios to include in our final portfolio. Once we have our candidate portfolio weights, we apply the first-order condition over portfolio variances to distribute our wealth between 2 candidate set of portfolio weights such that it minimizes the variance of the final portfolio.

Our results show that if contextual bandit algorithms applied to portfolio choice problem, given enough context information about the financial environment, they can consistently obtain higher Sharpe ratios compared to classical methodologies, which translates to a fully automated portfolio allocation framework.

Key results

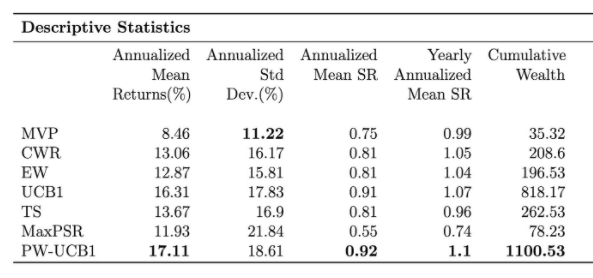

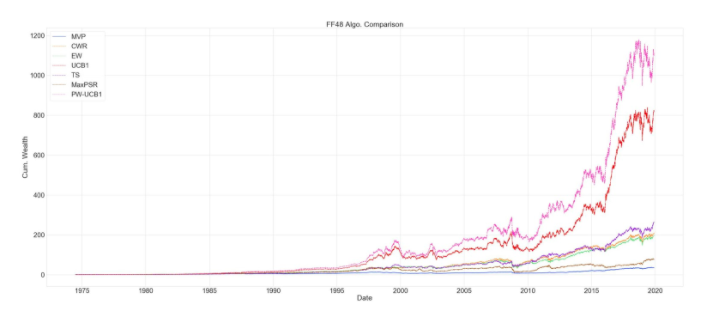

We conduct the experiments on 48 US value-weighted industry portfolios and consider the time range 1974-02 to 2019-12; The table below reports extensive evaluation criteria of following strategies by order; Minimum Variance Portfolio (MVP), Constant Weight Rebalance portfolio (CWR), Equal Weight portfolio (EW), Upper Confidence Bound 1 (UCB1), Thompson Sampling (TS), Maximum Probabilistic Sharpe ratio (MaxPSR), Probability Weighted UCB1 (PW-UCB1). Below the table, one can observe the evaluation of cumulative wealth through the whole investment period.

Table 1. Evaluation Metrics

One thing to observe here, even UCB1 and PW-UCB yield the highest Sharpe ratios. They also have the highest standard deviation, which implies bandit portfolios tend to take more risk than methodologies that aim to minimize variance, but this was already expected due to the exploration component. Our purpose was to see if the bandit strategy can increase the return such that it offsets the increase in standard deviation. Thompson sampling yields a lower standard deviation because TS also consists of portfolio strategies that aim to minimize variance in its action set.

Figure 1. Algorithm Comparison

We also include the evaluation of cumulative wealth throughout the whole period and in 10 year time intervals. One interesting thing to notice is that bandit algorithms’ performance diminishes during periods of high momentum followed by turmoil. The drop in the bandit algorithms’ cumulative wealth is more severe compared to classic allocation strategies such as EW or MVP. Especially PW-UCB1, this also can be seen from standard deviation of the returns. This is due to using the rolling window to estimate moments of the return distribution. Since we are weighing UCB1 with the Sharpe ratio probability, and since this probability reflects the 120-day window, algorithm puts more weights on industries that gain more during high momentum periods, such as technology portfolio. During the dot.com bubble (1995-2002) period, UCB1 and PW-UCB1 gain a lot by putting more weight on technology portfolio, but they suffer the most, during the turmoil that followed high momentum period. One can solve this issue by using more sophisticated prediction model to estimate returns and the covariance matrix.

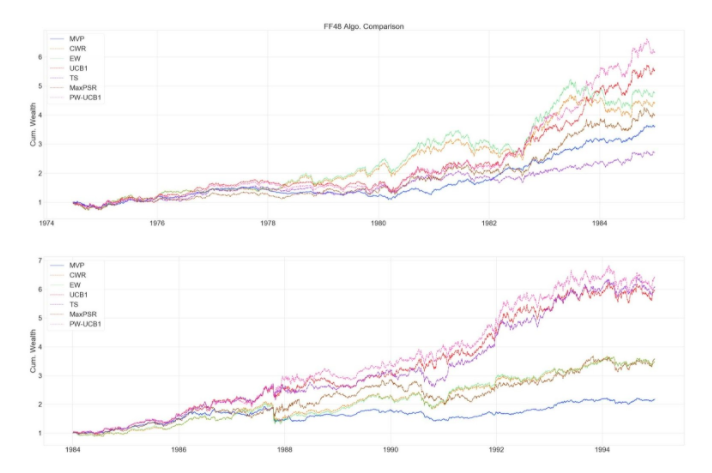

Figure 2. 1974-1994 Algorithm Comparison

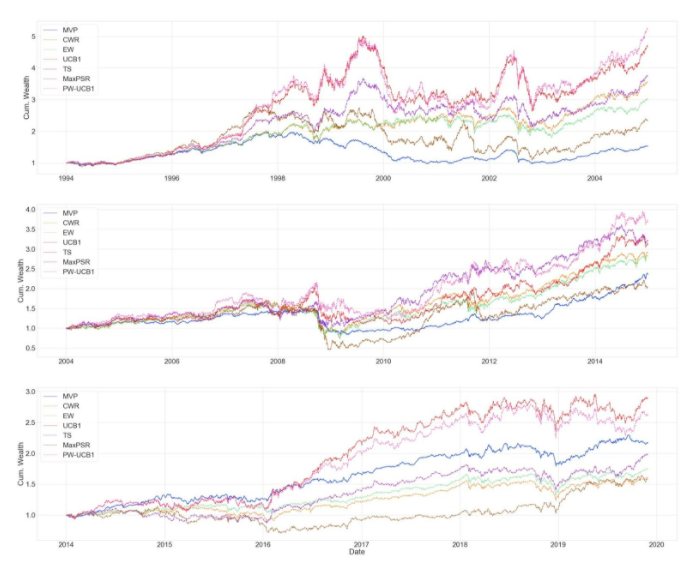

Figure 3. 1994-2020 Algorithm Comparison

To conclude, our algorithm allows dynamic asset allocation with the relaxation of strict normality assumption on returns and incorporates Sharpe ratio probability to better evaluate performances. Our algorithm could appropriately balance the benefits and risks well and achieve higher returns by controlling risk when the market is stable.

Data Science master project by Maximilian Müller ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

Crossed random effects models are additive models that relate a response variable (e.g. a rating) to categorical predictors (e.g. customers and products). They can for example be used in the famous Netflix problem, where movie ratings of users should be predicted based on previous ratings. In order to apply statistical learning in this setup it is necessary to efficiently compute the Cholesky factor L of the models precision matrix. In this paper we show that for the case of 2 factors the crucial point to this end is not only the overall sparsity of L, but also the arrangement of non-zero entries with respect to each other. In particular, we express the number of flops required for the calculation of L by the number of 3-cycles in the corresponding graph. We then introduce specific designs of 2-factor crossed random effects models for which we can prove sparsity and density of the Cholesky factor, respectively. We confirm our results by numerical studies with the R-packages Spam and Matrix and find hints that approximations of the Cholesky factor could be an interesting approach for further decrease of the cost of computing L.

Key findings

The number of 3-cycles in the fill graph of the model are an appropriate measure of the computational complexity of the Cholesky decomposition.

For the introduced Markovian and Problematic Design we can prove sparsity and density of the Cholesky Factor, respectively.

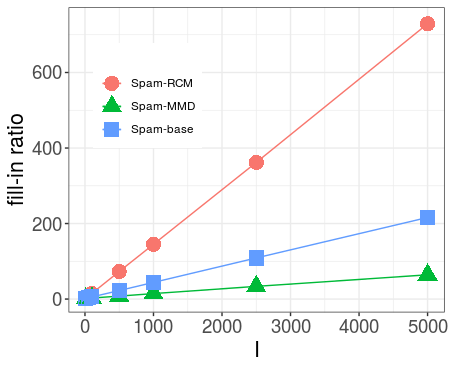

For precision matrices created according to a random Erdös-Renyi-scheme the Spam algorithms could not find an ordering that would be significantly fill-reducing. This indicates that it might be hard or even impossible to find a general ordering rule that leads to sparse Cholesky factors.

For all observed cases, many of the non-zero entries in the Cholesky factor are either very small or exactly zero. Neglecting these small or zero values could spare computational cost without changing the Cholesky factor ‘too much’. Approximate Cholesky methods should therefore be included in further research.

Fill-in-ratio (a measure of relative density of the Cholesky factor) vs. matrix size I for the random Erdös-Renyi scheme. For all permutation algorithms the fill-in-ratio grows linearly in I indicating that in general it might be hard to find a good, fill-reducing permutation.

EPP master project by Antonio Biondi, Zacharias Kountoupis, Joan Rabascall, and Marco Solera ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

This paper explores the role of soft skills in the U.S. labour market. According to the previous literature, these skills – also called non-cognitive- are crucial as they allow firms to lower coordination costs by trading job tasks more efficiently. We look at both sides of the labour market.

On the demand side, we collect 4,980 job ads from U.S. job portals through a web scraping technique, finding that larger firms require more job tasks and soft skills in their ads than the small and the medium ones.

On the supply side, we match the skills from the O*NET dictionary with the Survey of Income and Program Participation (SIPP) of the United States from 2013 to 2016, estimating return to soft skills around 15% of hourly wage. Moreover, we find statistically significant soft skills wage premium in the big firms around 2.5%, up to 3.5% for highly educated workers.

To the best of our knowledge, this is the first paper that finds a firm size wage premium for soft skills. These pieces of evidence suggest that larger enterprises are willing to pay more soft skills as they face higher coordination costs.

Conclusions

An increasing literature is focusing on the role of “soft skills” as the critical driver for labour market outcomes. A growing body of empirical evidence documents a reversal in demand for cognitive and soft skills: stagnating or even decreasing the first one, sharply increasing the second one.

A possible explanation is given by the fact that soft skills are associated to job tasks that are harder to replace by the automation, as they are mainly composed of tacit knowledge that is tough to encode (Autor, 2015). In this paper we analyse the role of soft skills in the U.S. labour market and their impact on wage.

As regards the supply side, we use the factor analysis to collect skills and abilities, finding a return to soft skills around 15% on U.S. hourly wage, that is almost four times higher than the return to cognitive abilities (4%). Moreover, we found a statistically significant soft skills wage premium in larger firms around 2.5% of hourly wage, up to 3.5% for those highly educated. We also document a strong complementarity between the firm size wage premium and level of education, especially for women: for this latter, the premium starts from 3% and increases to 4,5% when considering only those with more than 12 years of schooling. Results are consistent with our hypothesis, according to which soft skills are more valuable when increasing the size of firms as they are supposed to face higher coordination costs, compare to small enterprises.

The demand side analysis supports our results. After collecting job ads from U.S. job portals, we found that larger firms require more soft skills than the small ones. Finally, we report an excess of demand for soft skills in comparison to their occupational needs.

ITFD master project by Maria Dale, Giacomo Gattorno, Andre Osorio, Rebeca Peers, and Kerenny Torres ’20

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Abstract

How does a sudden migrant crisis affect criminal activity, and through which mechanisms does this effect take place? We approach this topic by studying the effect of Venezuelan migration on crime rates in Colombia, in the context of the recent migrant crisis that made more than 1.2 million Venezuelans cross the border.

Our study focuses on border provinces, where the presence of non-economic migrants is higher and potential assimilation problems could be exacerbated. Building on the fact that Venezuelan migration to Colombia happened due to apparently exogenous reasons and is unrelated to economic outcomes in the latter, we are able to study the causal effect of this large migration wave on crime rates.

Our results show that Venezuelan forced migration had no significant effect on overall crime, but a positive and significant effect on personal theft in Colombian border provinces. Furthermore, migration had a positive and significant effect on personal theft victimization rates of both Venezuelans and Colombians, while only having significant effects on the criminalization rates of Venezuelans. These results are robust to different specifications and controls, and two placebo tests provide strong evidence in favor of our empirical strategy and results. Finally, we link our findings with the overarching criminal context in Colombian border provinces, and develop relevant policy recommendations based on our findings.

Conclusions

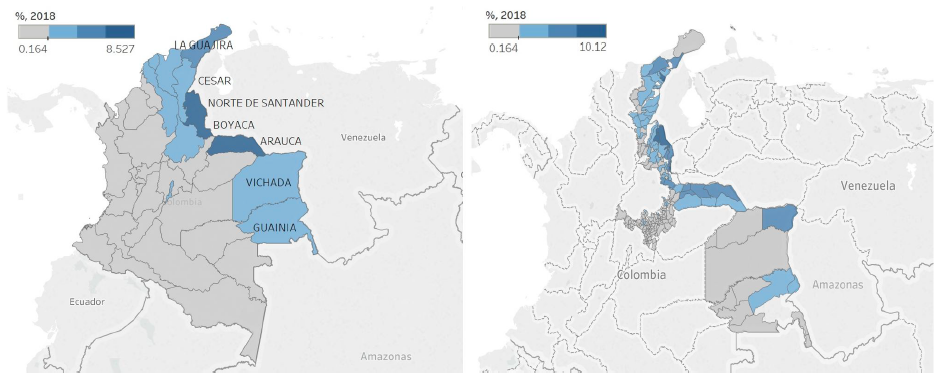

In this paper we analyzed the impact of the Venezuelan migrant crisis, which saw more than 1.2 million Venezuelans cross the border, on crime rates in Colombian border provinces between 2014 and 2018. We focused on the border provinces to study the particular effects of non-economic migration, as we find that migrants in this area did not target areas with specific characteristics but just settled in the closest center to get food, medicine and essential services. This settlement decision strictly based on closeness to border is also illustrated by the figure below: not only is the highest share of foreign-born population in the Colombian regions concentrated in our area of study (the 7 border provinces), but within these border provinces there is also a clear concentration in municipalities on the physical border with Venezuela.

Figure 1. Venezuelan-born population as % of total population by province and municipality, 2018. Source: Own calculations, based on data from DANE.

The main contribution of our study was presenting compelling and robust evidence on no significant effect of Venezuelan forced migration on overall crime, but a positive and significant effect on personal theft in Colombian border provinces. By also analyzing both the direct and indirect mechanisms through which this migration inflow can have an effect on different crime rates, we’re able to establish a causal effect of migration on both personal theft victimization and criminalization rates of Venezuelans, while only having significant effects on the victimization rates of Colombians.

Besides our key findings, other results hint at a more holistic narrative: migration also had a positive and significant effect on both homicide and personal injury victimization rates of Venezuelans. What could be driving these effects? As seen previously, Venezuelan migrants settled in municipalities right across the border from Venezuela – which, coincidentally, are municipalities where criminal organizations have a large presence: criminal organizations are present in 23 of the 42 municipalities on the border, and in 39 of the 81 municipalities where the change in proportion of Venezuelan migrants between 2014-18 was above the average.

In these high migration municipalities, as a consequence of criminal activity, homicide rates tended to be much higher at baseline than in other municipalities. Moreover, we see some evidence of discrimination in homicides – after controlling for all relevant socioeconomic covariates, being Venezuelan seems to have a significant and positive effect on being a victim of homicide.

This additional information could help construct the following holistic narrative and recommendations:

A large wave of migrants arrived in low-income border provinces with little (formal) employment opportunities, and some had to resort to small-scale theft to make a living, which explains the positive effect of migration on Venezuelan personal theft criminalization rates

Driven by both opportunity and attractiveness of targets, this caused an increase in personal theft victimization rates for both Colombians and Venezuelans, although it was much higher for the former than for the latter.

However, these municipalities were controlled largely by criminal organizations, which started threatening Venezuelans and forcefully recruiting them in large numbers. This could help explain the positive and significant effect of migration on both homicide and personal injury victimization rates of Venezuelans.

These findings imply that government policies should focus on reducing the vulnerability of Venezuelans by providing swift access to the formal labor market, either in border provinces or nationwide, so that Venezuelans can avoid resorting to small-scale theft and escape forced recruitment and exploitation from criminal organizations.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Introduction

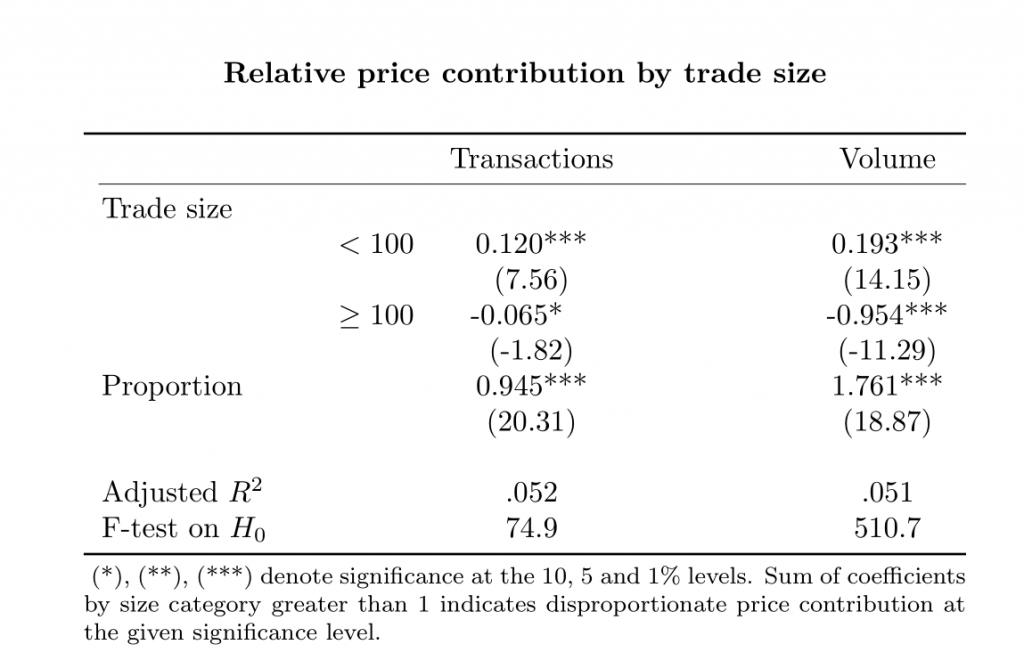

This paper builds on the stealth trading literature to investigate the relationship between several different trade characteristics and price discovery in US equity markets. Our work extends the Weighted Price Contribution (WPC) methodology, which in its simplest form posits that if all trades conveyed the same amount of information, their contribution to market price dynamics over a certain time interval should equate their share in total transactions or total volume traded in the period considered. Traditionally, the approach has been used to provide evidence that trades of smaller sizes convey a disproportionate amount of information in mature equity markets through the estimation of a parsimonious linear specification.

The methodology is flexible enough to accommodate for a first set of key extensions in our work, which focus on studying the relative price contribution from trades initiated by high-frequency traders (HFTs) and on stocks of different market capitalization categories over the daily session. Nonetheless, previous research has found that short-lived frictions make the WPC methodology ill-suited for analyzing price discovery at under-a-minute frequencies, a key timespan when HFTs are in focus. Therefore, to analyze the information content of trades of different attributes at higher frequencies we use a Fixed Effects specification to characterize trades that correctly anticipate price trends over under-a-minute windows of varying length as price informative.

Key results

At the daily level, our results underpin prior research that has found statistical evidence of smaller trades inputting a disproportionate amount of information into market prices. This result holds regardless of the type of initiating trader or market capitalization category of the stock being transacted, suggesting that the type of trader on either side on the transaction does not significantly alter the average information content over the session.

At higher frequencies, trades initiated by HFTs are found to contribute more to price discovery than trades initiated by non-HFTs only when large and mid cap stocks are being traded, consistent with prior empirical findings pointing to HFTs having a strong preference for trading on highly liquid stocks.

Editor’s note: This post is part of a series showcasing BSE master projects. The project is a required component of all Master’s programs at the Barcelona School of Economics.

Around the world, and especially in high-tech economies, the demandand adoptionof industrial robots have increased dramatically. The abandonment of robots (referred to as derobotization or, more broadly, deautomation) has, on the other hand, been less discussed. It would seem that the discussion on industrial robots has rarely been about their abandonment because, presumably, the abandonment of industrial robots would be rare. Our investigation, however, shows that the opposite is true: not only do a substantial number of manufacturing firms deautomate, a fact which has been overlooked by the literature, but the reasons for which they deautomate are highly multi-dimensional, suggesting that they depend critically on the productivity of firms and those firms’ beliefs about robotization.

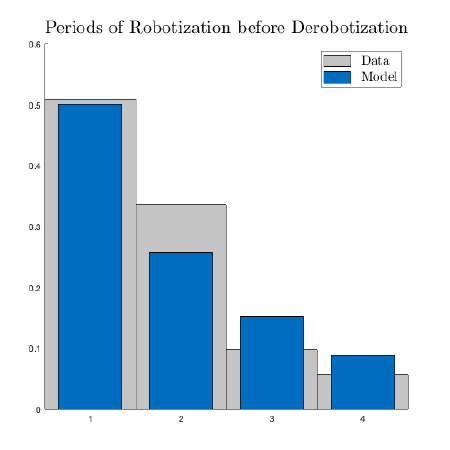

Extending the analysis of Koch et al. (2019), we use data from SEPI Foundation’s Encuesta sobre Estrategias Empresariales (ESEE), which annually surveys over 2000 Spanish manufacturing firms on business strategies, including on whether they adopt robots in their production lines. We document three major facts on derobotization. First, firms that derobotize tend to do so quickly, with over half derobotizing in the first four years after adoption of robots. Second, derobotizing firms tend to be relatively smaller than firms which stay automated for longer periods of time. Third, firms that abandon robots demand less labor and increase their capital-to-labor ratios. The prompt abandonment of robots, we believe, is indicative of a learning process in which firms robotize production with expectations of higher earnings, but later learn information which causes them to derobotize and adjust their production accordingly.

With this in mind, we propose a dynamic model of automation that allows firms to both adopt robots and later derobotize their production. In our setup, firms face a sequence of optimal stopping problems where they consider whether to robotize, then whether to derobotize, then whether to robotize again, and so on. The production technology in our model is micro-founded by the task-based approach from Acemoglu and Autor (2011). In this approach, firms assign tasks to workers of different occupations as well as to robots in order to produce output. For simplicity, we assume two occupations, that of low-skilled and high-skilled workers, where the latter workers are naturally more productive than the former. When firms adopt robots, the firm’s overall productivity (and the relative productivity of high-skilled workers) increases, but the relative productivity of low-skilled workers decreases. At the same time, once firms robotize they learn the total cost of maintaining robots in production, which may exceed their initial expectations. At any point in time, firms can derobotize production with the newfound knowledge of the cost. Likewise, firms can reautomate at a lower cost with the added assumption that firms retain the infrastructure of operating robots in production.

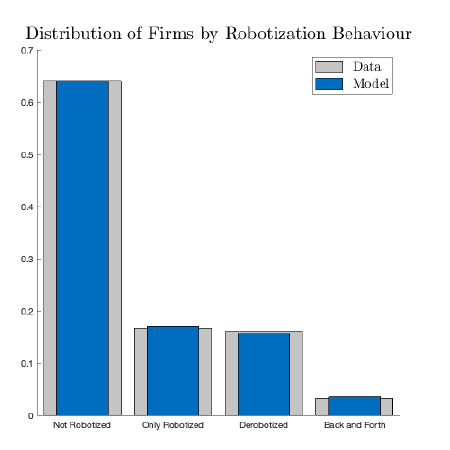

The simulations of our model can accurately explain and reproduce the behavioral distribution of automation across firms in the data (see Figure 1). Indeed, we are able to show that larger and more productive firms are more likely to robotize and, in turn, the firms which derobotize tend to be less productive (referred to as the productivity effect). However, the learning process which reveals the true cost of robotized production (referred to as the revelation effect) also highlights the role of incomplete information as a plausible explanation for prompt abandonment. Most importantly, our simulations suggest that analyses which ignore abandonment can overestimate the effects of automation and, therefore, must be incomplete.

Figure 1: The distribution (left) of firms by robotization behavior, and the distribution (right) of firms’ derobotization behavior (if they derobotize). The data from ESEE is in gray, while the calibrated simulation of our model is in blue.

Our project is the first, to our knowledge, to document the pertinent facts on deautomation as well as the productivity effect and the revelation effect. It is apparent to us, based on our investigation, that any research seeking to model automation would benefit from modeling deautomation. From that starting point, there remains plenty of fertile ground for new questions and, consequently, new insights.

We use our own and third party cookies to carry out analysis and measurement of our website activities, in order to improve our services. Your continuing on this website implies your acceptance of these terms.